By Aswath Damodaran. Originally published at ValueWalk.

The Fed – Between a Rock and a Hard Place

July 31, 2015

By Steve Blumenthal

“Now look at them yo-yo’s that’s the way you do it

You play the guitar on the M.T.V.

That ain’t workin’ that’s the way you do it

Money for nothin’ and your chicks for free.”

Money For Nothing – Dire Straits

The Fed is sitting between a “rock and a hard place”. A recent Bloomberg survey sees a 50% chance the Fed will lift rates in September. Oh, the consequences. Increasing U.S. interest rates further increases the valuation proposition of Treasurys vs. Bunds, Japanese Bonds and just about every other developed country debt. Further advantage to the U.S. dollar and significant disadvantage to the $9 trillion in U.S. dollars denominating Emerging Market debt. That amount owed goes higher with the dollar and we think Greece and Puerto Rico are issues.

Today I highlight two great letters. One from Lacy Hunt and the other from Bill Gross.

“The excessive debt burden, slow money growth, declining money velocity, the Wicksell effect and the high real rate of interest indicate that the fundamental elements are exerting downward, rather than upward, pressure on inflation.” Lacy Hunt

Fed officials themselves predict that the Fed funds rate will rise to 1.625% by the end of 2016. Hunt concludes interest rates are heading lower thus hold onto your long-term Treasury bond exposure.

Gross argues that the Fed’s low rate policy is a large part of the problem. There is much to gain from both Hunt and Gross’s viewpoints.

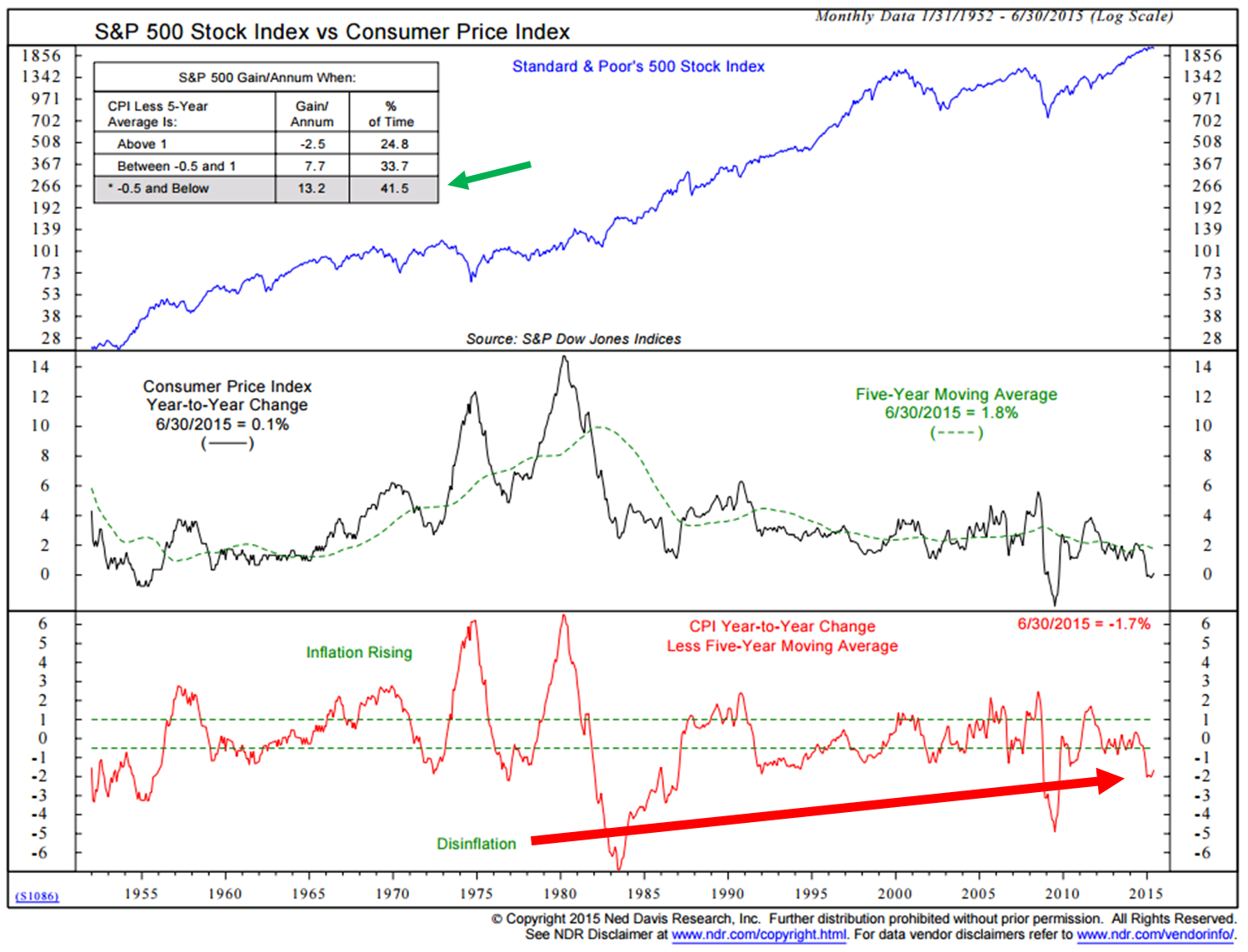

The battle today is one of inflation vs. deflation. The global central bankers are independently and collectively trying to drive inflation higher. So far, as we’ll see in the next chart, they are losing that battle (bottom red arrow).

Put me in the 50/50 camp for a September rate increase. The Fed wants to get off the zero bound peg but the risks are many. Getting to 1.625% in 2016 or even less will come with consequence. More from Hunt:

“The predicament the Fed is in is one that could be anticipated based on the work of the late Robert K. Merton (1910-2003). Considered by many to be the father of modern day sociology, he was awarded the National Medal of Science in 1994 and authored many outstanding books and articles. He is best known for popularizing, if not coining, the term “unanticipated consequences” in a 1936 article. He also developed the “theory of the middle range”, which says undertaking a completely new policy should proceed in small steps in case significant unintended problems arise. As the Fed’s grand scale experimental policies illustrate, anticipating unintended consequences of untested policies is an impossible task. For that reason policy should be limited to conventional methods with known outcomes or by untested operations only when taken in small and easily reversible increments.”

Untested operations only when taken in small and easily reversible increments. Global QE has been extraordinarily massive. Small and easily reversible? No way.

Money Ain’t for Nothin’ Get Your Fed for Free. Between a Rock and a Hard Place – indeed.

I link to these two great pieces below and conclude with a few short thoughts and, most importantly, a wish for you to slow down, detox from work and find a nice place this August to escape to.

Included in this week’s On My Radar:

- Lacy Hunt – Misperceptions Create Significant Bond Market Value

- Bill Gross – Say A Little Prayer

- Trade Signals – Watching Out for Minus 2

Lacy Hunt – Misperceptions Create Significant Bond Market Value

Here are a few highlights:

- Lacy ultimately believes that the yield on the 30-year bond will move much lower.

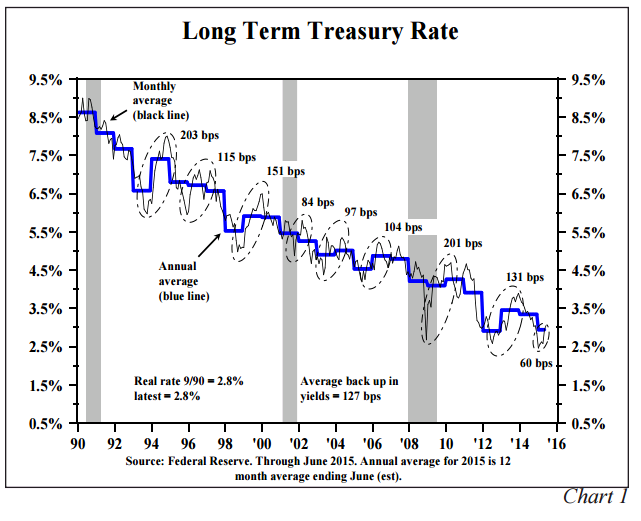

- He notes: From the cyclical monthly high in interest rates in the 1990-91 recession through June of this year, the 30-year Treasury bond yield has dropped from 9% to 3%. This massive decline in long rates was hardly smooth with nine significant backups. In these nine cases, yields rose an average of 127 basis points, with the range from about 200 basis points to 60 basis points (Chart 1).

- The recent move from the monthly low in February has been modest by comparison. Importantly, this powerful 6 percentage point downward move in long-term Treasury rates was nearly identical to the decline in the rate of inflation as measured by the monthly year-over-year change in the Consumer Price Index which moved from just over 6% in 1990 to 0% today. Therefore, it was the backdrop of shifting inflationary circumstances that once again determined the trend in long-term Treasury bond yields.

- In almost all cases, including the most recent Quarterly Review and Outlook Second Quarter 2015 rise, the intermittent change in psychology that drove interest rates higher in the short run, occurred despite weakening inflation. There was, however, always a strong sentiment that the rise marked the end of the bull market and a major trend reversal was taking place. This is also the case today.

- Lacy sites four misperceptions have pushed Treasury bond yields to levels that represent significant value for long-term investors. These are: 1. The recent downturn in economic activity will give way to improving conditions and

Sign up for ValueWalk’s free newsletter here.

{kind=link}