By Gabriel Thoumi, CFA, FRM. Originally published at ValueWalk.

As written by Chain Reaction Research, on June 29, the Financial Stability Board Task Force on Climate-Related Financial Disclosures (TCFD) published their final report including key recommendations for the Agriculture, Food and Forest Products sector. The Financial Stability Board (FSB) monitors and makes recommendations about the global financial system with FSB members including all G20 economies, the European Commission and other relevant financial and monetary leaders. Its current chair is Mark Carney, Governor of the Bank of England

Get The Full Seth Klarman Series in PDF

Get the entire 10-part series on Seth Klarman in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

Bruno Bertocci, Managing Director, Head of Sustainable Investors, UBS Asset Management and TCFD member stated:

“TCFD framework enables addressing material deforestation risks in agriculture supply chains and for downstream buyers.” (Interview, July 19, 2017).

Steve Waygood, Chief Responsible Investment Officer, Aviva Investors stated and TCFD member stated:

“The TCFD will be both a mirror and a widow. A mirror as it will help companies study where they can improve their own risk management practices. A window as it helps the market understand where climate risks exist in their portfolios. This is particularly important where those risks are not being managed well.” (Interview, July 19, 2017).

The purpose of the TCFD work is to develop voluntary climate-related financial disclosures that are consistent, comparable, reliable, clear and efficient. They also aim to provide information to lenders, insurers and investors the aids decision making. The TCFD was developed in response to Mark Carney’s Breaking the Tragedy of the Horizon: Climate Change and Financial Stabilityspeech in fall 2015. The FSB chose 32 members to lead the TCFD. These individuals represent financial markets and economic sectors from the G20 and broadly cover both users and preparers of disclosures of financial data. Over an 18-month period, the TCFD developed voluntary guidance on climate-related financial disclosures, seeking input from global stakeholders through an exhaustive set of engagements, and then published their final recommendations.

These TCFD disclosures and their specific Agriculture, Food, and Forests Products sector recommendations are built upon years of experience from implemented disclosure platforms and knowledge generated from recent sustainable banking initiatives. As an industry-led initiative, the TCFD recommendations bring climate-related disclosures to a mainstream audience. The TCFD process is important for investors to be aware because it provides voluntary guidelines for better data as a climate risk mitigation tool in the Agriculture, Food, and Forests Products sector.

The TCFD stated in their findings that they see clear evidence for the need for climate-related financial disclosure in the Agriculture, Food, and Forest Products sector’s financial statements, specifically its:

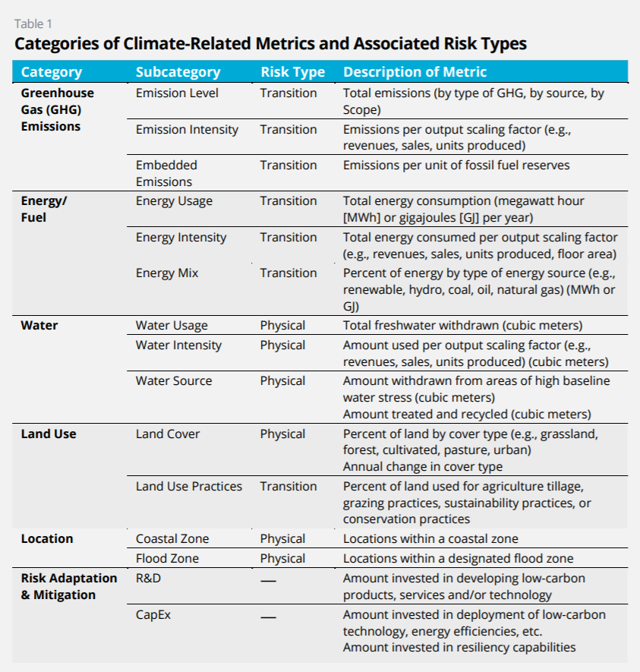

Table 1 shows six broad categories of metrics that may help an organization understand its vulnerability or resilience to various transition and physical risks. For example, organizations with high emissions in their operations and supply chains, high water use, unsustainable land use practices, or facilities in geographically “at-risk” areas, such as coastal zone locations, may be more vulnerable to transition and physical risks. Alternatively, organizations that are energy and water efficient, have low emissions, or use sustainable land practices may be less vulnerable to climate-related risks, depending on the policy, technological, and geographic constraints that they face.

Figure 1: Categories of Climate-Related Metrics and Associated Risk Types. Source: TCFD.

The TCFD recommends that after companies assess the risks described in Table 1 (above), they should address both strategic and financial planning decisions related to these risks and opportunities, such as:

Develop enterprise risk management (ERM) tools for mitigating, transferring, accepting and controlling risks.

Pursue relevant capital expenditure opportunities that enable appropriate ERM responses.

Finance R&D actions that are support ERM responses.

Describe the impact of climate-related risks and opportunities on the organization’s businesses, strategy, and financial planning.

Describe the resilience of the organization’s strategy, taking into consideration different climate related scenarios, including a 2°Celsius or lower scenario.

Disclose the metrics used by the organization to assess climate related risks and opportunities in line with its strategy and risk management process.

The TCFD summarizes the climate-related opportunities for the Agriculture, Food and Forest Products as increasing efficiency, reducing inputs, and developing new products. Therefore, the TCFD asks that each company’s disclosures focus on both quantitative and qualitative inputs that reduce GHG emissions, water use, and waste while increase carbon sequestration and growth and yield per hectare.

The metrics that the TCFD recommends that the Agriculture, Food, and Forest Products use are in Figure 2 (below).

Financial Category

Climate-Related Category

Metric

Revenues

Risk Adaptation and Mitigation

Revenues/savings in local currency from investments in low-carbon alternatives (e.g., R&D, equipment, products or services)

Expenditures

Risk Adaptation and Mitigation

Operating expenditures in local currency for low carbon/ water alternatives (e.g., R&D, equipment, products, or services)

Expenditures

Water

Total water withdrawn and total water consumed in cubic meters

Expenditures

Water

Percent of water withdrawn and consumed in regions with high or extremely high baseline water stress

Assets

Water

Amount of assets committed in regions with high or extremely high baseline water stress described using number of assets, value, and percentage of assets

Assets

GHG Emissions

Non-mechanical (Scope 1): Emissions from biological processes measured using metric tons of CO2 equivalent

Assets

GHG Emissions / Land Use

Land use change (Scope 1): Changes of carbon stocks as a result of land use and land use changes (e.g., from the conversion of native habitats into farmlands) measured using metric tons of CO2 equivalent

Expenditures

GHG Emissions

Mechanical (Scope 1): Emissions from equipment or machinery operated on farms/plants measured using metric tons of CO2 equivalent

Expenditures

GHG Emissions

Purchased energy (Scope 2): Emissions from purchased heat, steam, and electricity consumed on the farm /plant measured using metric tons of CO2 equivalent

Assets

Risk Adaptation and Mitigation

Investment (CAPEX) in low currency in low carbon/water alternatives (e.g., capital equipment or assets)

Even though climate-related risks in the Agriculture, Food, and Forest Products sector generally arise from changing land-use patterns and their resulting GHG emissions and water and waste management issues, Figure 2 above demonstrates that systemic metrics are available.

NGO leaders such as SPOTT now assess companies systematically for 125 indicators in the palm oil and timber, pulp and paper sectors using many of these exact same metrics, making it easy for investors to consider their investments in large global companies through the metrics applied by the TCFD. Using the SPOTT tool, an investor can assess the large agriculture trader Bunge across a broad set of metrics that overlap between SPOTT’s criteria and the metrics suggested by the TCFD.

Bunge states the company’s 10-year plan includes a target to reduce water use by 10 percent overall and 25 percent in high water stress regions,

{kind=link}