{kind=link}

Courtesy of Chris Kimble.

Today I was honored and humbled to do an audio interview with the great people at Benzinga this morning. The short interview can he heard HERE

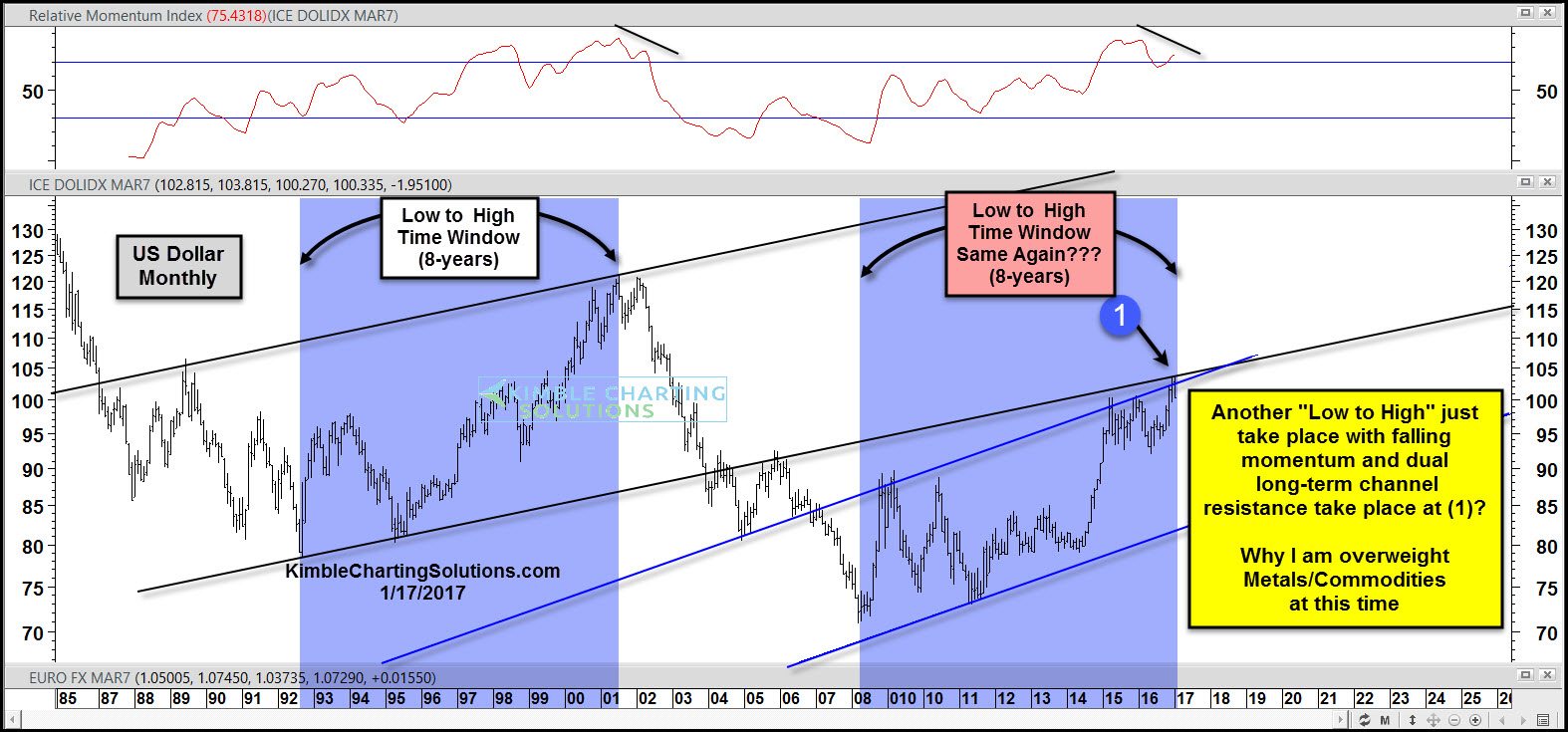

I discussed the the three charts below during our discussing. Our Full Interview can be heard HERE My interview starts at the 34:45 mark and runs for about 10 minutes.

CLICK ON CHART TO ENLARGE

CLICK ON CHART TO ENLARGE

![]()

CLICK ON CHART TO ENLARGE

Thanks again to Benzinga for having me on the show. Our interview can be found HERE

To become a member of Kimble Charting Solutions, click here.