Courtesy of Benzinga.

On February 20, JMP Securities issued a note updating ratings and price targets on the commercial real estate sector, including:

- Blackstone Mortgage Trust Inc (NYSE: BXMT),

- Chesapeake Lodging Trust (NYSE: CHSP),

- Equity Commonwealth (NYSE: EQC),

- Host Hotels & Resorts Inc (NYSE: HST) and

- Sabra Health Care REIT Inc (NASDAQ: SBRA)

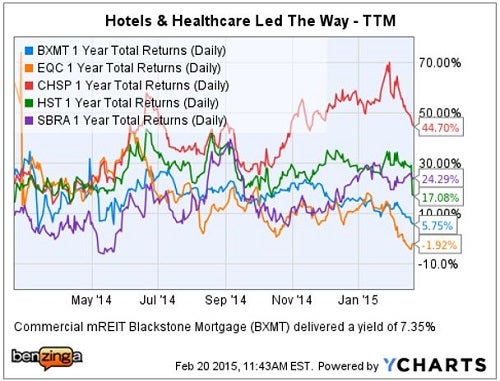

Tale Of The Tape – Past Year

Blackstone Mortgage Trust – Market Outperform

JMP increased its price target to $32 from $31 following the company’s 4Q earnings release and conference call.

- BXMT reported “4Q core EPS of $0.52, which beat consensus by a penny and matched the new $0.52 dividend that was set in December 2014; marking the second consecutive quarter where core earnings fully covered the dividend.”

- Blackstone management believes it can “continue to deliver on the targeted ROI range of LIBOR +12-13%,” (despite increased competition from larger banks).

- JMP trimmed its 2015 core EPS estimate to $2.20 from $2.25, primarily due to a slightly lower net interest spread assumption;

- JMP introduced an initial 2016 core estimate of $2.40; and 1Q16 dividend projection of $0.56.

Host Hotels & Resorts – Market Outperform

JMP maintained its rating but reduced its price target to $25 from $27; based on 14.0x (unchanged) and downward-revised 2016 EBITDA estimate of $1.62 billion (down from $1.70 billion).

- Host reported disappointing 4Q14 results and provided renovation-impaired guidance that was well below what the Street was expecting.

- “Group business weakened in 4Q, and renovations at several key properties impacted performance.”

- “4Q RevPAR grew 3.2% on a 60 bps decline in occupancy and a 3.6% gain in rate.”

- “Portfolio occupancies are at or near historic peaks, making each incremental point of occupancy that much harder to come by.”

Chesapeake Lodging Trust – Market Outperform

JMP did not provide a PT update, but felt the stock was “fully valued” at a price of $36.42, based upon the shares trading at 15.9x and 13.9x JMP revised 2015 and 2016 EBITDA estimates, respectively.

- “CHSP reported a slightly disappointing quarter, with adjusted EBITDA of $33.7M falling short of guidance of $33.8-35.3M on soft RevPAR growth and weaker than expected margin expansion.”

- “In 4Q, the 20-hotel portfolio posted pro forma RevPAR growth of +4.9%, just short of guidance of +5-7%, and adjusted hotel EBITDA margin expansion of +20 bps to 30.5%, which also fell short of margin expansion guidance of 30.8-31.5%.”

- “CHSP has been active in the acquisition market, acquiring the 337-room JW Marriott SF Union Square for $147.2M in 4Q, and announcing on Thursday an agreement to acquire its first hotel in Miami’s South Beach market, the James Royal Palm for $278M, or 13.9x forward EBITDA.”

Sabra Health Care REIT – Market Underperform

JMP maintains its $25.50 PT which is based on a ~5% premium to its FTM NAV estimate, which represents 22% downside potential from current levels, or ~17% after the 5% dividend yield.

- “SBRA reported 4Q AFFO of $32M, in line with the JMP estimate of $31.9M, and reiterated previous 2015 guidance of $2.05- $2.10 without acquisitions.”

- JMP maintained its “2015-2016 AFFO estimates of $2.22 and $2.25, respectively, as capital structure adjustment benefits are expected to be offset by G&A increases.”

- “SBRA currently trades at a 35% premium to [JMP’s] FTM NAV estimate, compared to the overall HC REIT industry at 20%, despite showing higher than average leverage levels…”

Equity Commonwealth – Market Perform

JMP stated that Equity Commonwealth’s fourth quarter earnings result is somewhat immaterial.

- EQC has begun a transition phase, “whereby management is in the midst of instituting a multi-year plan focused on culling an extensive portion of the assets, and significantly de-levering the balance sheet.”

- “Management has been reluctant to shed too much insight into the strategy until recently, as $2-$3B of sales are planned, with proceeds allocated to debt reduction, share buybacks, and special dividends necessary to maintain REIT status.”

- JMP is “incrementally positive” on this strategy; noting “the potential for a turnover of the shareholder base, and reluctance for investors to get involved in a story with an unstable near-term outlook as the portfolio takes shape, may curb share performance in the near term.”

Latest Ratings for BXMT

| Date | Firm | Action | From | To |

|---|---|---|---|---|

| Feb 2015 | Jefferies | Maintains | Market Outperform | |

| Feb 2015 | JP Morgan | Maintains | Overweight | |

| Feb 2015 | Deutsche Bank | Maintains | Buy |

View More Analyst Ratings for BXMT

View the Latest Analyst Ratings

Posted-In: JMP SecuritiesAnalyst Color REIT Upgrades Analyst Ratings General Real Estate Best of Benzinga

{kind=link}