By Sven Carlin. Originally published at ValueWalk.

Peter Lynch is one of the best investors ever. I give examples for each of the mentioned characteristics a stock to buy should have. Lynch is a contrarian, focused on earnings from companies Wall Street doesn’t like or can’t sell to the public. Enjoy the discussion and examples.

Q1 2020 hedge fund letters, conferences and more

- It sounds dull – or even better, ridiculous

- And it does something dull

- It does something disagreeable

- It is a spinoff

- The institutions don’t own it, and the analysts don’t follow it

- The rumors abound – It’s involved with toxic waste and/or the mafia

- There’s something depressing about it

- It is a no-growth industry

- It’s got a niche

- People have to keep buying it

- It’s a user of technology

- The insiders are buyers

- The company is buying back shares

13 characteristics a stock to buy should have by Peter Lynch

Transcript

Good day fellow investors. We continue with our summary of one of the best books for investors out there. Peter Lynch’s One Up On Wall Street. This is part of my free stock market investing course and if you like this video, you might want to check the rest of the course in the link in the description below.

Now, who is Peter Lynch, just to give you a reminder why this is so important. Well, he was the manager at Fidelity Magellan for 13 years. And if you invested 1000, when he started, you would end up in just 13 years with 28,000. So that was a remarkable return above 29% per year. And that’s why this book is totally about practicality from one of the best investors that has ever and is still alive. So really, really a great book and really boiled down to what really matters. And that’s why we’re going to discuss the thirteen characteristics that Lynch says that a stock to buy must have, at least some of them.

Further, just to explain that Lynch wasn’t just a one off kid. He managed his wife’s portfolio that started with about a few thousand dollars and turned it into more than 10 million. So he practically over 45 years turned 1000 into 3.5 million and this book summarises his knowledge.

Now before we start, what do you think Lynch is looking for when he wants to invest in stocks? Is he looking in all the stocks that everybody else loves? That the market loves growth stocks? Or is he looking at something completely different, something nobody loves, and therefore you can find the bargains. You’ll see over the thirteen characteristics that we’ll go through. It’s actually the opposite of what the market does.

So even Lynch, like all value investors, is a contrarian, and therefore, I will try to give as many examples for each characteristic of a stock to keep it entertaining. But as it goes for Lynch, he’s investing is dull, ugly, depressive. Nobody wants to touch it with a 10 foot pole. And that’s where Lynch finds his investments.

Let’s start with the characteristics explained one by one. If you like this video, please click like is good for the YouTube algorithm. Subscribe and click that notification bell to get notified when other videos come out to be it from this series or other stock analysis.

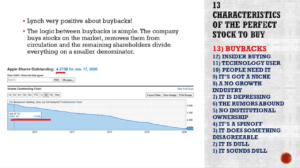

So let’s start with number 13 and then we’ll go down to number one. So Lynch loves buybacks, he’s very positive in the book about buybacks. A buyback is a process when a company buys its own shares on the market then cancels them out and therefore the remaining number of shares is lower. A perfect example is Apple, 5 years ago, the number of outstanding shares was 5.7 billion, and now is 4.37 billion. So the company practically bought 25% of the shares outstanding, which means that the on the same earnings, earnings are much higher dividends per shareholder that you get per share are much higher, and therefore, the positivity of buybacks and the positivity of buybacks, especially in the Lynch era. When he was managing fidelity, the S&P 500 price to earnings ratio was mostly below 10.

So when there is a price earnings ratio below 10, which means that if a company buys back its stock, the return is above 10%. And that was the case with Apple when Warren Buffett stock started buying if we look at the price earnings ratio in 2016, the price earnings ratio was 10. And the stock price was also much lower.

But then thanks to the buybacks, thanks to change in market valuation, now the stock price is much higher and the price earnings ratio is actually doubled. This means that the current buyback is twice as expensive as the buyback that the company did in 2016. So, we have to be very careful when it comes to buybacks, and really check Okay, is the company buying back stocks just for buying back stocks, no matter the price? Or are they allocating capital wisely? That’s the question with buybacks.

In the Lynch era, every buyback was a great buyback because stocks were extremely cheap. Now it’s a little bit different. And you have to be careful not to think of buybacks as good with companies as Boeing that spent what 40 something billion dollars on buybacks over the last years when the stock price was extremely high. When the price to book ratio was not existent because there was no book value, and with buybacks above price earnings ratio of 20, the return is just 5% even lower. And you know what happened to Boeing in the last few months because there was no margin of safety because all the money was spent on buybacks.

Now another characteristic is insider buying and not CEO insider buying. But when the middle management when the upper management is buying more and more shares at market prices, when they do that, they do that only for one reason and then do it because they think the stock price will go up. Usually insiders are net sellers of the stock because they want to chip in on the options they get on the free shares they get, etc. Let’s see. So this is just an example of the stock that I was recently researching Allison Transmission. And you can see that over the last five years the total buys were $530,000 in total sales from insiders $700 million.

This is what is insider selling usual the usual activity. However, you can track that and you can then see okay, what our insider is doing by looking at the SEC form for the statement of changes in beneficial ownership that the company has to report to the SEC and then there is also the website. And you can see another stock that I used to own Fresh Del Monte Producealso total buys 50,000 total sales 91 million and if we look at the common stock purchase or sale over the last period here reported every management manager is selling their stock so managers you have to see okay at high prices, prefer selling rather than anything else. Also, if we look at Tesla common stock purchase or sale, there have been just two purchases from musk Elon and Lawrence Joseph Ellison.

But those two purchases are related to the capital increase that Tesla did just a while ago at the stock price of I think 767. All the other managers, have been selling the stock even Musk’s brother Kimball has been selling the stock over the last period.

Now another characteristic of a great stock is that it is a user of technology, so it benefits from the development in some new technology. Many are attracted by new technology stocks, but that is high competition questionable margins and question about outlook. But the best investment might be the company that uses the technology to lower its costs and increase margins an idea even if that is a difficult sector. Very low margins, but self checkouts lower the cost perhaps for supermarkets. So those are an example of a user of technology.

Another very important characteristic, you can invest into something that people like or something luxurious but don’t need. However, when you invest in something that people really need, then you have a margin of safety, you have a limited downside because you know, you know that whatever happens, people will steep still keep buying that product. So very important characteristic. Just an example. This is Walmart stock versus GoPro. So we need Walmart, we need to go buy things or whatever we need. And Walmart provides that to us. So it’s very unlikely that in 5-10 years, people will stop needing Walmart. However, GoPro, it was hot for a while many bought it and the result is a decline of 94% in the stock price. Compared to Walmart, which is up 48% over the last five years

Another example is Archer Daniel Midlands, food producer, distributor, etc. That you know, okay, you got to eat so a company like this is pretty sure that will make money in any environment will do business in any environment. And what’s the outcome? Well just look at the dividend increases that Archer Daniels Midland has done over the last 20 years from a dividend of below 20 cents per share to above 1.40. Boring company we’ll discuss also later that’s also another characteristic, really not sexy, nothing sexy, just producing, I don’t know oil seeds, etc. But here, this is something that we should consider sexy.

Alright, next one. It’s got a niche. So something specific something where the company can differentiate itself among others, and Warren Buffett likes to call it, it has also a moat, something that can protect the business from incursions of the competition. Do you know what was Warren Buffett’s biggest investing mistake? What was the stock? What was the company? Some say Kraft Heinz. Okay, that was a mistake.

But the biggest mistake, the biggest mistake was a company called Berkshire Hathaway. Yes, it was a textile business in the 1960s. No moat, high capital needs to increase production to keep costs low scalability, but okay, he didn’t make much money from that. But the rest of the investments that he did, by learning the lesson there were extremely well because he started to look for niches and competitive advantages.

One example of a niche is a company we discussed in a recent video 3M. So 3M produces has thousands of patents and produces all these small things needed for the production of various products all across the globe and also proprietary products for free end. So very specific has also a brand and it operates in many many niches and it’s not profitable for any competition to go and develop similar products to enter and compete with 3M. Therefore we can consider freedom to have a niche many niches or how we like to call it a moat.

Now it’s a no growth industry everybody’s focused on growth stocks, cannabis, Aurora Cannabis, I remember it a few years ago, so when you’re crazy, you should invest it will change the world. Yes, of course. And the same in Lynch’s book that was written in 1989. His list goes as following 1950s it was carpets. Yes, carpets were the hot stuff of the 1950s because of the huge real estate building, 1960s electronics, 1980s it was computers, 1990s the end of it was the internet mania, now we have seen cannabis, lithium and all others pretty much debacle for now. But if you invest in a no growth story, slow growth story, like for example food, and Archer Daniel Midlands that we discussed then you are looking at something boring, but that doesn’t have the risk of Aurora Cannabis.

Then something depressing. Okay, nobody wants to depressing stock or a depressing business. Nobody likes to talk about it. Service Corporation international is a burial service. And you can see how okay, sometimes it becomes a hot stock but often and in the last 40 years, three times nobody wanted to come close to it. And Peter Lynch mentions it in his book. So if you can find the depressing business that cannot go out of business because the demand for their services is pretty stable, then you might be looking at something interesting.

Next, the rumors abound Waste Management, in the 1980s, when Lynch was managing Fidelity, waste businesses were all related to the mafia to all things that could be ugly and bad and dirty. But then in the beginning of 1990s we had the first boom, then again, nobody wanted to touch waste management stocks for 20 years, and now we had another boom. So bad rumours, dirty businesses, that’s where you find great, great investments or how Peter Lynch likes to call them 10 baggers.

Okay, next step. As we mentioned already, you can own what everybody else owns or the hot names like Google, Netflix, Amazon, etc. Or you can go and search where nobody looks. And it means you have to put a lot of effort, do a lot of research, or simply as Lynch says, and we have mentioned in the previous lectures, that looking there where you have a circle of competence. You might be a medical doctor and say, okay, this product is getting used more and more, let’s see, how is the stock doing?

And then you see, okay, your wife buys something, let’s see how that stock is doing. And then every three months, you get an opportunity to investigate something, you understand the business, and every year or two, you get a great buy. Also, Lynch says, Look at stocks that have no institutional ownership that are not followed by analysts, because there are the best investments can be found. If I asked you, what do you want to know more about Google, Amazon, Netflix, Facebook, what do you want me to make videos about? Those will be the stocks.

However, if I told you that great investments might be [unintelligible] Tourist Hotels, La Doria? Oh, I don’t want to do deal with that because that’s something I don’t know. And if we look at the book from Daniel Kahneman, Thinking Fast and Thinking Slow, we as humans don’t like something that is unknown. We don’t like the mental effort that we have to put in to learn the unknown. And therefore that’s an investing advantage that also Peter Lynch discusses in his book.

I think one idea for the future, when I’ll have time is making a book called Thinking Fast and Slow for investors. That’s what we need, we need the right mindset and that’s what we are doing with these videos.

How to know when to buy a stock: Conclusion

Now. Next characteristic, it’s a spin off. Spin off our companies that are separated from the parent company because of different business model or better prospects by working independently. Shareholders of the parent company keep their share in the parent company, but also get the new share in the new company. Livent Corp, is a lithium miner that was spun off by the parent FMC Corporation. So they said, as a lithium miner, you’ll do better by yourself.

And then you have these shareholders that had company like FMC, they hold it, let’s say, for the dividend, and they get the shares that keep going down because of the selling pressure, because people don’t know what to do about it. And therefore, if you look into spin offs, you might be rewarded very well.

Next one, it does something disagreeable. If you’re watching this video, you’re using something some device that has plenty of metals that have been mined somewhere. So nobody likes my mining, but it is something we need, and therefore I think it fits the characteristics of okay. It’s something we need and we will need in the future, but it also does something disagreeable.

Next on Lynch, it is something dull and we have seen Archer Daniel Midlands. Waste Management. What is more boring than managing waste? And Lynch starts his characteristics by discussing the name of the company, Pep Boys, Manny, Moe & Jack. So it’s a boring name, what kind of name is the Pep Boys? But it has been one of the best investments for Lynch.

If you like this video please subscribe if you have any questions, please leave them in the comments below. I always love reading your questions. Thank you for watching. Don’t forget to check my free stock market course in the links below and I’ll see you in the next video.

The post 13 characteristics a stock to buy should have by Peter Lynch appeared first on ValueWalk.

Sign up for ValueWalk’s free newsletter here.

{kind=link}