By Jacob Wolinsky. Originally published at ValueWalk.

SAGA Partners commentary for the first quarter ended March 31, 2020, discussing holding excess cash.

Q1 2020 hedge fund letters, conferences and more

1Q20 Results

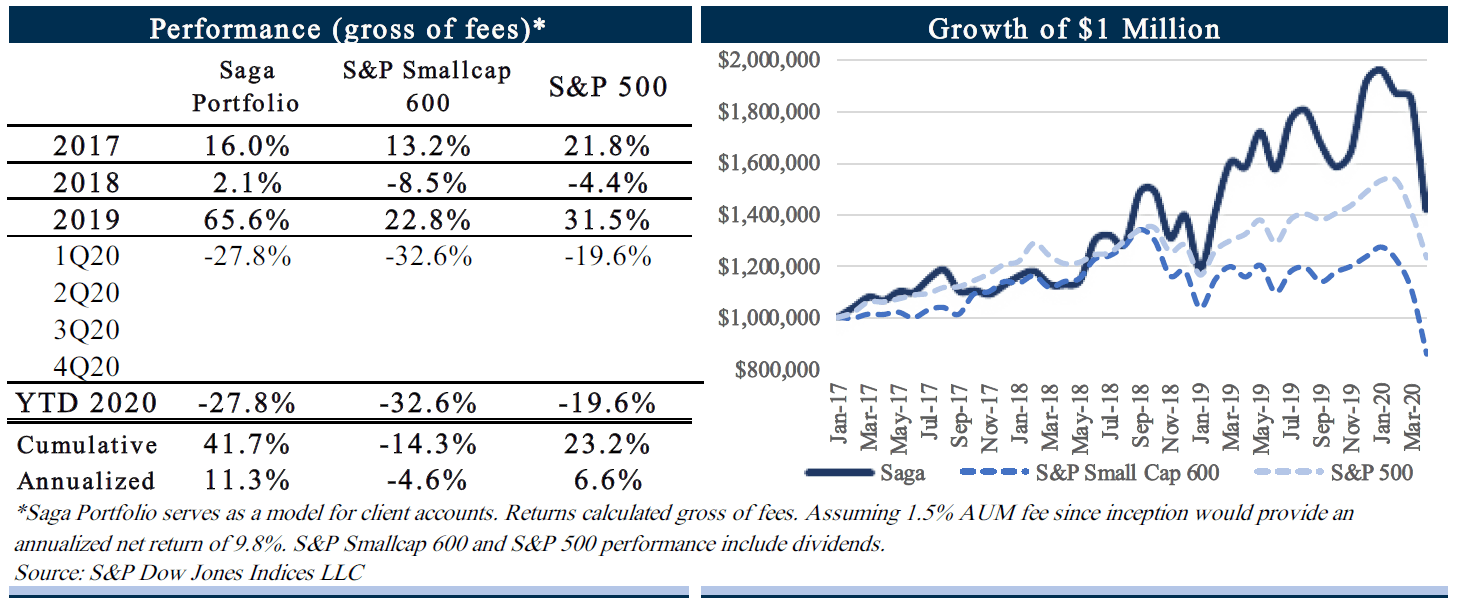

During the first quarter of 2020, the Saga Portfolio (“the Portfolio”) decreased 27.8% gross of fees. This compares to the overall decrease, including dividends, for the S&P Smallcap 600 Index and S&P 500 Index of 32.6% and 19.6%, respectively.

The cumulative return since inception on January 1, 2017 for the Saga Portfolio is 41.7% gross of fees compared to the S&P Smallcap 600 Index and S&P 500 Index of -14.3% and +23.2%, respectively. The annualized return since inception for the Saga Portfolio is 11.3% gross of fees compared to the S&P Smallcap 600 and S&P 500’s respective -4.6% and 6.6%.

Market Commentary

We were originally planning on switching to semi-annual letters to put less emphasis on shorter-term results. However, given recent events related to the COVID-19 pandemic and its significant impact to shorter-term results in the public markets, we think investors may welcome another quarter of the Saga philosophy and our thoughts surrounding the current situation.

During the last quarter, the S&P 500 experienced the fastest decline of over 30% in the history of the stock market and the second largest single day loss ever. A sharp drop in the stock market is typically broad-based and affects most stocks. In this particular case businesses related to hospitality, “non-essential” retail, and travel are feeling the immediate impacts of government mandated shutdowns of the economy and stay at home orders as an attempt to slow the spread of the coronavirus with shares of many companies falling well over 50% from recent highs.

We have little to add to the evolving dialogue surrounding the virus’ health implications. Even the certified epidemiologists seem to be struggling to wrap their heads around the virus, which no one had heard of before last December. Our basic understanding is the virus is very contagious and while not very harmful to the majority of people, can be very harmful to those with compromised immune systems and the elderly, potentially overwhelming hospital systems in badly affected areas.

Regarding the economy, it is pretty apparent that the U.S. and much of the world has entered a recession. Recessions are technically defined as two or more quarters of declines in gross domestic product (GDP) and are certain to occur from time to time. It’s no surprise that when the government requires many businesses to stop operating and most people to stay home, aggregate demand and output will decline substantially.

No recession is the same though many share similar characteristics, such as decreased business activity, increased bankruptcies, and higher unemployment. The Great Recession in 2008-2009 was largely the result of overleveraged households surrounding the real estate bubble, while the one facing us today is the result of a health pandemic that has effectively shut down much of the economy and delivered a demand shock to many businesses.

During this period there will be lower capital expenditures, cash flows will dry up, if not turn negative, and unemployment figures will rise to levels never experienced before. In response, the Fed and Government are attempting to maintain liquidity in the financial system and provide aid to stabilize the economy during its mandated break.

It’s doubtful this scenario made it into any 2020 economic forecasts and rightly so. If every investment or business decision considered the chance of a global pandemic, little activity would take place. Imagine a scenario where a cyber-attack took down the global internet infrastructure for an indefinite amount of time. What would Google, Facebook, or the countless other internet-facing companies look like? That is the equivalent to what the airlines and non-essential brick & mortar retailers are facing with revenues dropping to zero in the blink of an eye.

Significant selloffs are a reminder that anything can happen to market prices in the short-term. Crazy things can occur when there is a price quote minute-by-minute. When managing an investment portfolio, one must be able to survive any scenario in order to succeed. Although this basic idea seems simple and is crucial to long-term investing success, during times of easy money and upbeat outlooks, many may attempt to juice returns by using leverage in the form of margin debt or options. That is not something we will ever consider for a stock portfolio even if it might help boost returns over the long run. It reminds us of the quote Howard Marks often cites, “never forget the 6-foot man who drowned crossing the stream that was 5 feet deep on average.” By simply managing an unleveraged, long-only stock portfolio, we have the important advantage of ignoring the market when we want to or taking advantage of it when an opportunity presents itself.

Investing Versus Speculating

About 400 years ago, the first formal stock exchange was established in Amsterdam, which made it far easier to transfer ownership in public companies at the going market price. Everyday people could participate in the compounding machine of the market economy. While this opened up opportunity for more people to share in the prosperity of businesses, the formation of the stock exchange reinforced some of human nature’s more primitive and less desirable qualities, such as: greed, jealousy, herd behavior, and desire to get rich quick by gambling.

The formation of stock exchanges quickly divided participants into two camps: investors and speculators. Investors take ownership in companies to participate in the growth in earnings power and dividends of a company. They view themselves as owners of companies, not renters of stocks. Alternatively, speculators do not care about where the price of a stock is trading relative to its intrinsic value but where they think other people think the price of a stock will be next quarter or year. They price stocks based on their expectations of what they think other people’s expectations are likely to be. It’s a zero-sum game with few, if any, consistent winners.

The South Sea bubble of 1720 is probably one of the most prototypical examples of speculation. The South Sea Company was a British joint stock company that was granted a monopoly to trade with the islands in the “South Sea” and South America. There was no realistic prospect that trade would take place given Britain’s involvement in the War of Spanish Succession and Spain and Portugal controlled most of South America. It was actually a scheme based on persuading people to swap government debt for shares in the company. Officials were incentivized to talk up the share price with persuasive salesmen spreading enthusiasm and high expectations for the value of potential trade in the New World, causing a buying frenzy. The stock price increased from about £100 to £1,000 in less than a year, but left many investors ruined when shares quickly cratered back to £100.

Not even Isaac Newton, considered one of the brightest scientists in history, was immune to these all too natural human tendencies. He participated earlier in the bubble and cashed out with 100% profit as market prices went to what seemed to be unjustified levels in his opinion. However, as prices continued to advance, the pain of not participating in easy profits resulted in him investing what is estimated to be much of his fortune near the peak of the bubble. Upon the subsequent crash, he ended up losing nearly everything. Newton famously said, “he could calculate the motions of the heavenly bodies, but not the madness of people.” If one of the smartest people in history isn’t immune to these emotions, we do not even want to tempt ourselves by trying to buy things based simply on the belief we know where the price of shares will trade tomorrow.

Speculation is a very crowded game of mass psychology that distorts the investing process and in which even geniuses are susceptible to its deceivingly easy fortunes. We’ve seen countless examples of people give in to these temptations. Once one becomes more and more concerned with where stocks are going to trade next, they are getting farther away from thinking as a business owner and more like a speculator. For the truly long-term investor, all that matters in investing is where the price of shares is trading relative to the intrinsic value of the company, not whether shares will move up or down tomorrow or next week.

Timing The Market

Speculation can arise from both euphoria and fear. The biggest mistakes in investing are often not based on what you know or don’t know but by how you behave in both good times and bad. Given the unprecedented health pandemic and economic lockdown, we understand the feelings of fear and uncertainty one may have. While it may be tempting to react to the frightening headlines by selling stocks in favor of “safer” assets like cash, such a strategy has proven to be deeply flawed historically.

If anything can be learned from studying market history, panics, and recessions, reacting to one’s emotions in fear of further price declines in an attempt to wait for the storm to pass is exactly the opposite action that should be taken. Similarly, reacting to one’s emotions during good times from fear of missing out on further price increases is not a good idea. The market may continue to be volatile over the near-term with substantial ups and downs. We have no sense for which direction the market may turn over the next twelve months, and that has always been our view.

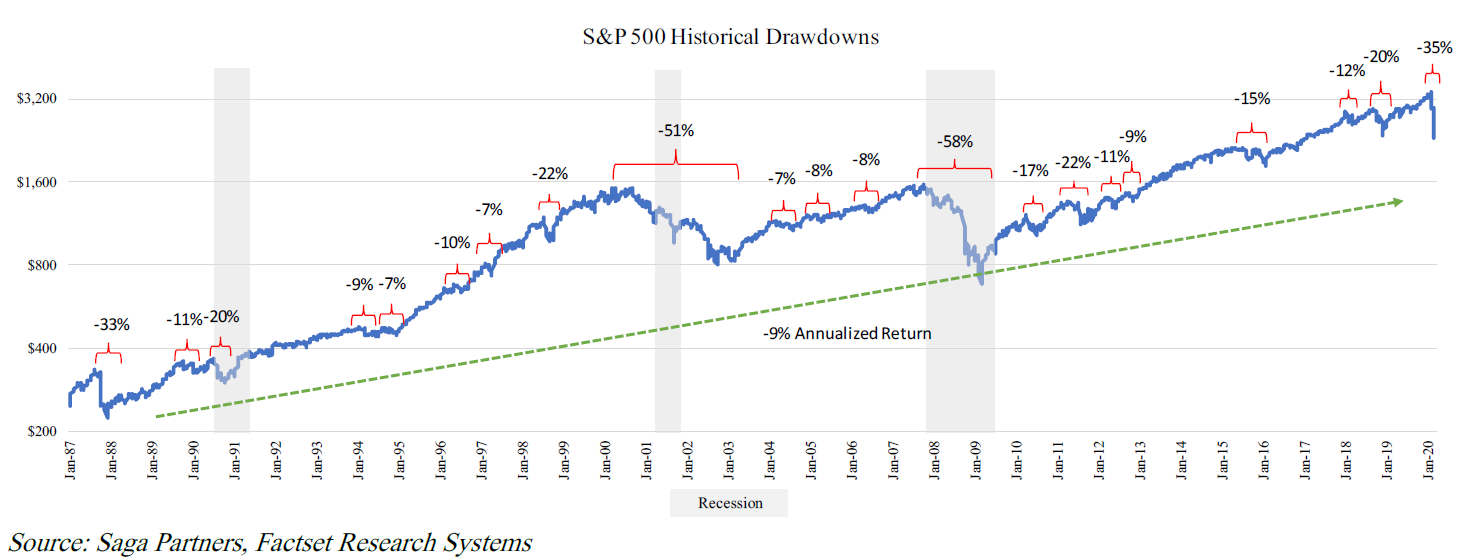

Below is the chart we provided last quarter showing the S&P 500 Index and historical drawdowns since 1987, now including the recent 35% decline.

During this period, the S&P 500 has provided a 9% compounded annual return (CAGR) including dividends. This is as good of a result as anyone could have imagined, generating enormous wealth for those who participated, despite including three recessions, likely four if we are currently in one, and two of the great market bubbles of the past century.

Despite this highly favorable result, very few investors fully participated. Equity fund investors underperform the market by a huge margin. Blackstone produced a report in which they showed that even though the average equity mutual fund in the U.S. averaged 8.2% annually over the last 30 years, investors who invested in these funds averaged only 2%. Another study showed the average equity investor return has underperformed the market by over 4% annually. These significantly lower returns are largely a result of the natural human tendency to chase performance and avoid any setbacks i.e. trying to time the market. The error of omission by not investing in stocks in an attempt to time the market has likely lost investors more money than any realized losses themselves.

Even with the long-term upward trend, the stock market is littered with frequent drawdowns, corrections, and bear markets. There is a 10%+ correction every two years on average, and about half of those will be a 20%+ decline, which have occurred every four to five years.

Since these drawdowns occur regularly, people attempt to avoid these declines by buying and selling based when they “feel” a correction is about to happen. Of course average is not a fixed time frame. There can be long periods with little downward movement. Maybe after 2-3 years of strong returns, commentators will start saying we are due for a correction, suggesting investors should move to cash. Perhaps another 2-3 years will pass with strong market returns as one waits on the sidelines trying to control feelings of missing out on easy money, ready to buy back in at the first sign of a down market.

Not only do investors often hold cash in fear of future corrections, during such drawdowns it is common for them to sell what stocks they own in an effort to protect their wealth, waiting for the bottom to pass…a double whammy to long-term returns. We’ve heard many people say they believe stocks will be worth far more than current prices in five or ten years, but they think stocks have not bottomed yet so are waiting for another 10-20% decline before buying. The thing about market bottoms is they are only known with the help of hindsight.

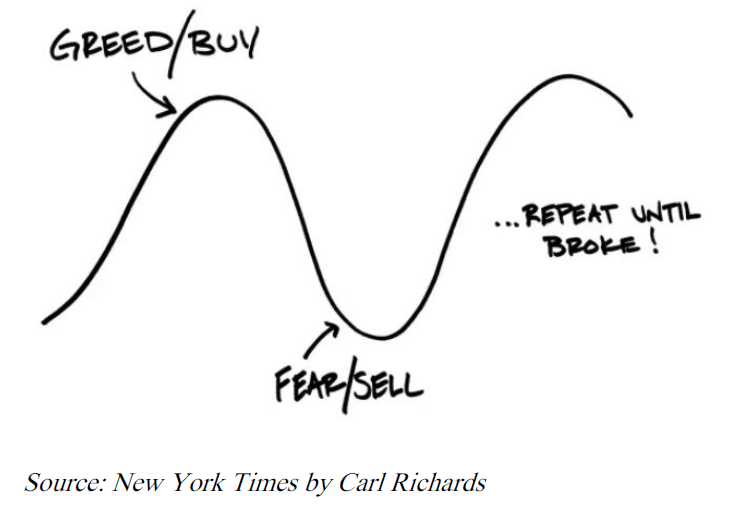

Carl Richards from the New York Times illustrated the cartoon below that depicts people’s natural instinct to buy when news is good and sell after bad news, reacting to their fear and greed.

It is a big mistake to look at what is going on in the economy today and then decide whether to buy or sell stocks. A bad economy and down market can be your friend if it provides an attractive investment opportunity. It does not make a lot of sense to wait to buy into a great business at an attractive price for the potential that it gets more attractive tomorrow. One should decide whether to buy or sell stocks based on how much they are getting for their money, as in where shares are trading relative to their intrinsic value. The important thing is to have the right long-term outlook.

Volatility is a big advantage to investing in the public markets, but those who become affected by market fluctuations and then make decisions based on them turn it into a disadvantage. If you buy stocks understanding they are susceptible to large price fluctuations, with the expectation they will appreciate over a period of many years, it will likely shield you from any desire to act during market extremes. Just as anyone running for President of the United States should expect roughly half the country to disagree with him or her, public equity investors should expect that stock prices are susceptible to large price fluctuations based on little more than sudden changes in current sentiment.

Some may argue that as the risks of the pandemic grew more apparent in mid-February the prudent thing would be to sell or hedge one’s positions. This same logic could be applied to selling when risks of the Chinese trade war arose, potentially rising interest rates, or the numerous other headline risks that appear frequently. This reasoning also misses the point that one is able to sell near market highs and buy back in at the lows with full clarity.

If trying to time the downturn, the question is when does one buy back into the market? Should one have bought the dip when the market dropped 4% on February 24? Recent history suggested buying the dips has been very profitable, although simply being invested has been even more profitable. Was March 9, the second largest single day decline in stock market history, a good time to get back in? Perhaps one was smart enough to buy back in at the bottom tick on March 23 or are they smart enough to foresee the bottom is still looming sometime in the future? All these questions go into our “too hard” pile. We have found that we are not any good at predicting or timing these market movements.

Maybe there does exist a token few investors that are talented market timers, better at knowing what people’s emotions will be tomorrow than others, though we remain skeptical. Phil Fisher may have said it best, “I had seen enough of in an out trading, including some done by extremely brilliant people, that I knew that being successful three times in a row only made it that much more likely that the fourth time would end in disaster. The risks were considerably more than those involved in purchasing shares in companies I considered promising enough to want to hold them for many years of growth.”

We know plenty of people who consider themselves to be long-term investors but will trade in and out of their favorite stocks. To help protect us from these natural human tendencies, we will always be market agnostic. We make our investing decisions not on where we think shares will trade next quarter or year but based on a bottom-up analysis of picking a few of the best returning opportunities we can find.

Holding Excess Cash

Since we have no confidence in our ability to time the market, we rarely hold large cash balances in the Saga Portfolio. This is because we are simply trying to find the best opportunities available based on the information and prices we have today, and we are usually able to find enough attractive ideas that look better than holding cash.

In our 3Q18 investor letter we said:

“If anyone knows they will need cash within the next few years, investing in public equities is more of a speculative activity. We’ve probably hammered the point to death that anything can happen in the markets over the short term and you do not want to find yourself selling assets at fire sale prices.

Once you determine the amount of cash you may need to hold, the question is what to do with everything else. Cash is one of the worst performing asset classes over time. Holding excess cash is an active investment decision and strikes us as somewhat risky since it is certain to lose value. It does provide optionality if other assets can be bought at a cheaper price at some point in the future, however trying to time the market also seems risky to us and people that believe they have the foresight to do so are typically proved wrong.”

It can’t be stressed enough how important having an adequate cash emergency fund/security blanket is to endure difficult times of potentially lower income or unexpected expenses. The amount to set aside in liquid cash is dependent on one’s regular ongoing expenses, any significant one-time expenses (think house, car, vacations, gifts), and reliability of future income.

This exercise is the same whether someone is in their 20s, 90s, a business, foundation, or any other type of entity. Always keep money you know you may need over the next few years in safe, liquid assets (i.e. cash or short-term bonds). It’s all about what one’s cash needs and cash sources will be going forward. This cash security blanket should be viewed separate from the assets that you set outside to grow in value over time. If you find that you do not have excess savings beyond this amount, owning publicly traded stocks becomes more of a speculative game.

For the assets set aside to grow wealth over the long-term, it is all about opportunity cost, as in what is the best available option to invest in today. We assume you want to invest in income-producing assets (stocks, bonds, real estate) versus non-producing assets (commodities like gold, art, jewelry, etc.). While some investors can be very good at investing in non-producing assets, this is not our area of expertise. The return of non-producing assets is always dependent on someone else paying you more for it in the future instead of the cash it generates over its life.

When considering the long-term returns of income-producing assets, cash rarely looks like an attractive investment. Holding excess cash when there are other attractive investment opportunities available is only admitting that we believe we have the ability to time the market. If we don’t think we can time the market with all of our money, then why would we believe we can time the market with a smaller percent of our money?

Additionally, when holding excess cash balances, nearly any other income-producing assets will always look relatively more attractive than cash. If holding a lot of cash, it is possible we may lower our investing standards for a potential new company since its return will merely beat an asset that just sits there. We like the idea that for us to invest in a new company it must look relatively better than any of our existing ideas. We want each new idea to improve the quality of the portfolio as a whole.

This view may seem unconventional and is not shared by most other investment managers, but it seems riskier to hold something that is sure to lose value over time when we can find other assets that have a very high probability to grow in value. Why give the S&P 500 index any more of a chance to beat us by holding excess cash in an already difficult match up?

Investing Opportunity Costs, Stocks Versus Bonds

We think we have made our views on market timing pretty clear. However, we do not want that to be confused with the statement that one should own stocks regardless of price. We will only invest in something if we believe the long-term expected return looks attractive. The price of an asset is the sole determinant of return when considering the cash flows it will generate over its life.

Stock prices can rise to the point where the long-term return outlook no longer looks attractive. This was the case near the peak of the dot-com bubble when the S&P 500 was trading at a 30-40x P/E ratio (2-3% earnings yield) and long-term U.S. treasury bonds were yielding high single digit annual returns. If you bought the S&P 500 in March 2000 and held it for the subsequent 20 years to March 2020, you would have earned an annual return of 4.4% including dividends. If you bought the 20-year U.S. treasury, it would have earned a 6.8% annual return, providing over 2% in “alpha” annually by simply holding treasury bonds.

Beating the S&P 500 index by 2% annually has proven to be very difficult for the majority of mutual funds. Morningstar’s mutual fund database has historical performance going back 15 years. There are 1,100 U.S.-focused equity mutual funds with a 15-year track record listed on Morningstar and only about 90 of them beat the index by more than 2% annually. This list does not include all the failed mutual funds that went out of business or stopped operating during this time. We estimate that beating the index by more than 2% a year over the long-term would likely put you in the top 5% of professional money managers. Simply buying U.S. treasuries near the peak of the dot-com bubble could have provided industry-leading results in a very competitive field.

The dot-com bubble was one of the few times in market history that long-term bonds looked relatively more attractive than buying the market index. We would like to think if stocks were trading at a valuation such as in the year 2000 with a 2-3% earnings yield and a 1% dividend yield while U.S. government securities were available at a 6-7% yield, we would choose the latter.

Today, however, is the complete opposite scenario. When looking across the investment landscape, stocks appear to be a no brainer when compared to bonds at current prices. Long-term U.S. treasuries yield less than 1%, investment grade bonds yield ~3%, and the S&P 500 has over a 2% dividend yield and was trading for 18x 2019 earnings (~6% earnings yield) at the end of the quarter. Certain sectors of the index were trading at even more attractive prices. 2020 earnings are sure to drop from the economic shutdown, but they will inevitably grow over the next 10 years.

Moving between stocks and bonds based on what you expect the long-term return of the asset to be is not market timing, it is value investing. If considering stocks, bonds, a commodity like gold, or cash at today’s prices, stocks are an easy choice in our opinion.

Portfolio Commentary

We typically do not comment on quarterly changes in share prices (both favorable and unfavorable) since short term price swings are largely random, distracting, and can even be misleading. That practice may look convenient given the price of nearly all our holdings fell significantly during the month of March, some even falling by more than 50% at their lows.

A panic, crisis, or recession occurring does not impact how we manage the Saga Portfolio by any means. During a downturn, we do not rotate from low quality companies into higher quality, or cyclical to non-cyclical, or from an out of favor industry into a more favorable industry, etc. At any part of the market cycle, we only own companies that meet our investing criteria with the expectation that we would be happy to own them throughout a downturn.

During such steep selloffs, we must assess if the new market price more accurately reflects a much worse future than previously believed or if it provides a more attractive price at a larger discount to intrinsic value than before. While we obviously do not welcome pandemics, economic declines, terrorist attacks, or any other type of potential harm, it is not unusual that during times of fear and panic certain stocks may fall to prices that provide a very attractive buying opportunity. Last quarter we bought two new companies which we will discuss more in the next investor letter and reallocated to certain holdings where the price-to-value ratio became much more attractive. It is our expectation that the Portfolio’s overall long-term returns will be stronger because of the market selloff, but only time will tell.

Companies and their earnings power will be impacted by the pandemic and social distancing measures to varying degrees. Some will be harmed significantly and may not survive, some will see demand decline temporarily as in any recession, and a few will even benefit. The adverse impact to airlines, cruise lines, brick and mortar department stores, and hospitality focused businesses, may be longer-lasting while those related to e-commerce or cloud-based internet services may benefit. Our job is to incorporate the current events that may have a lasting impact to a company’s earnings power and evaluate whether the current price (regardless of where it traded last week, month, or year) looks attractive going forward.

While no one really knows how much the economy will contract or how long this recession will last, it is unlikely that we are about to enter a new world order that will permanently change life as we know it. Eventually some sort of normal will return, people will likely have the same basic wants and needs, and companies will be there to satisfy those needs.

We believe that the companies we own are exceptional, led by high caliber managers, and have strong futures. In many cases they will benefit during a downturn from their strong market position as competitors struggle and they win market share in the inevitable recovery.

Conclusion

When fear and negativity dominate the headlines, an excerpt from Matt Ridley’s 2015 book The Evolution of Everything seems appropriate to end on a more positive note:

“There are two ways to tell the story of the twentieth century. You can describe a series of wars, revolutions, crises, epidemics, financial calamities. Or you can point to the gentle but inexorable rise in the quality of life of almost everybody on the planet: the swelling of income, the conquest of disease, the disappearance of parasites, the retreat of want, the increasing persistence of peace, the lengthening of life, the advances in technology…It is surely gloriously obvious that the world was a much, much better place than it had ever been. Yet read the newspapers and you would think we had lurched from disaster to disaster and faced a future of inevitable further disaster…I could not quite reconcile in my mind this strange juxtaposition of optimism and pessimism. In a world that delivers an endless supply of bad news, people’s lives get better and better.”

It is no question the world is facing a significant challenge that it will need to overcome. Despite these challenges, it is optimism that will likely pay dividends over the long-term. This is not some naïve view; it is backed by historical data. Even though future success is never guaranteed (ask the dinosaurs), we think a more sanguine future is the probable outcome.

We do not know if we have reached the market bottom and we never will. We continue to comb through the markets for companies that meet our investing criteria and sometimes a near-term crisis can provide an opportunity for us to reallocate to more attractive opportunities.

We could not be more grateful to our investors for being long-term in their thinking and allowing us to manage the Portfolio to the best of our abilities during any selloffs and more volatile times. None of our investors called during the steepest decline in the history of the stock market in fear or panic, and in fact, a few added to their accounts. We have spoken with several investors in recent weeks who were curious to hear our thoughts on the current situation as everyone is trying to decipher the long-term implications of this dynamic situation. We are always available to answer any questions or to simply catch up.

We try our best to outline the Saga Portfolio’s strategy so investors understand how we think and manage their money. A strong investor base aligned with our philosophy is a true competitive advantage in the investment management business. We would love to continue to grow with other like-minded investors. If you know someone that may potentially be interested in a strategy like the Saga Portfolio, feel free to forward on our information.

Sincerely,

Joe Frankenfield, CFA

The post SAGA Partners 1Q20 Commentary: Investing Opportunity Costs, Stocks Versus Bonds appeared first on ValueWalk.

Sign up for ValueWalk’s free newsletter here.

{kind=link}