By DIVIDEND GROWTH INVESTOR. Originally published at ValueWalk.

Lowe’s Companies Inc (NYSE:LOW), together with its subsidiaries, operates as a home improvement retailer in the United States, Canada, and Mexico. The company offers a line of products for construction, maintenance, repair, remodeling, and decorating.

Q2 2020 hedge fund letters, conferences and more

Lowe’s Companies Hikes Its Quarterly Dividend

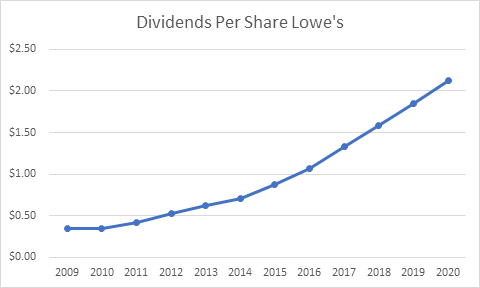

Lowe’s Companies is one of 28 dividend kings in the US. The company last hiked its quarterly dividend by 9.10% to 60 cents/share in August 2020. This marked the 58th consecutive annual dividend increase for the dividend king. Over the past decade, the company has managed to increase distributions at an annualized rate of 19.40%.

The strong growth in dividends per share was aided by growth in earnings per share and the increase in the dividend payout ratio over the past decade.

Between 2010 and 2020, earnings per share rose at an annualized rate of 16.30%/year. Lowe’s Companies grew earnings per share from $1.21 in 2010 to $5.49 in 2020. The company is expected to generate $8.31/share in 2021, but in the current environment, estimates are a challenge.

Lowe’s Companies is in the process of exiting its Mexico operations, closing Orchard Supply Hardware and closing underperforming stores in Canada and the US. Getting out of the ancillary businesses, closing underperforming businesses and concentrating on key operations in home improvement and enhancing the website functionality should help in focusing its efforts on key competencies. The company is working on a transformational initiative to improve stores, do a better job in inventory control, reign in SG&A spending, and improving supply chains. An increase in margins can improve profitability for each dollar of sales. It looks like the company will be relying less on growth through new stores, and more on doing better with the store base it already has.

Ties To North American Housing Market

The company’s fortunes are tied to the housing market in North America. A strong housing market will provide better sales over time. Growth in housing prices over time will provide a wealth effect, which can be transformed into higher spending on homes. As houses age over time, homeowners will spend more funds maintaining their places of living. Living in a house will tell you that the number of house projects never ends, as things break or get into the need for improvements, remodeling and renovations. An uptick in construction can benefit Lowe’s Companies.

While the earnings growth during the past decade has been impressive, we should not forget that Lowe’s Companies is exposed to the cyclical nature of the economy. During the past recession for example, earnings dropped from $1.99/share in 2007 to $1.20/share in 2010.

Lowe’s Companies is second to Home Depot, which has slightly better store locations, higher margins, and a higher share of the professionals market. Better execution at Lowe’s Companies can help in attracting more DIY customers and those from the Pro-segment. Investing in better customer service can pay dividends down the road, as better trained associates can broaden the moat behind the retailer operations. The ability to order online and pick-up in store is helpful in having successful online operations, while fending off threats from Amazon.

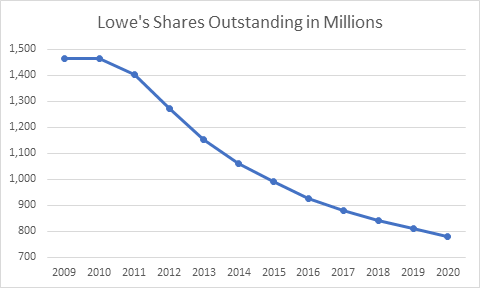

The company has been active on the share repurchase front during the past decade. The number of shares outstanding has gone from 1.465 billion in 2009 to 768 million by 2020. Most of the repurchases occurred between 2013 – 2020, when the share price was going up.

A Fairly Valued Stock

I find Lowe’s Companies to be fairly valued today, mostly because the earnings estimates are up so much due to the increase in sales and earnings around the shut-downs. A lot of smaller competitors were closed during the lockdowns, and many may go out of business. As a result, Lowe’s and Home Depot took business from competitors. This further solidified their competitive positions. Additional time at home also fueled demand for DIY renovation projects. Further growth is stimulated by the growth in construction activity.If the economy goes into a recession, I expect that Lowe’s Companies will halt share buybacks, until the coast is clearer.

Either way, the buybacks have made each remaining share more valuable, thus boosting earnings per share.

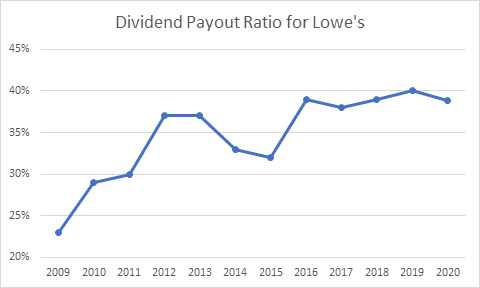

The dividend payout ratio has increased from 23% in 2009 to 39% in 2020. The increase in the payout ratio has definitely helped Lowe’s Companies grow distributions faster than earnings. It looks like between 2012 and 2019 however the payout ratio has not increase by much, which means that dividend growth was closely following earnings growth for a better part of the past decade.

Right now, the stock sells for 19.50 times forward earnings and yields 1.50%. In comparison, Home Depot is trading at 25.30 times forward earnings and yields 2.10%. I find Lowe’s Companies to be fairly valued today, mostly because the earnings estimates are up so much due to the increase in sales and earnings around the shut-downs..

Relevant Articles:

- Home Depot (HD) Dividend Stock Analysis

- How to select winning retail stocks

- 36 Dividend Aristocrats On My Shopping List

- Dividend Kings List

The post Lowe’s Companies (LOW) Dividend Stock Analysis for 2020 appeared first on ValueWalk.

Sign up for ValueWalk’s free newsletter here.

{kind=link}