By DIVIDEND GROWTH INVESTOR. Originally published at ValueWalk.

Philip Morris International Inc (PM) manufactures and sells cigarettes, other nicotine-containing products, smoke-free products, and related electronic devices and accessories.

In 2008 Altria spun-off its international tobacco operations, and thus creating Philip Morris International Inc (PM).

Q2 2020 hedge fund letters, conferences and more

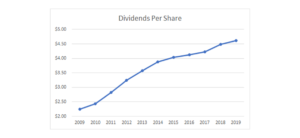

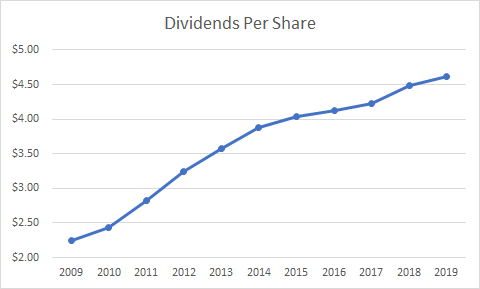

Philip Morris International Inc Increases Dividends

Philip Morris International Inc has managed to increase dividends annually since the spin-off. Annual dividends went from $2.24/share in 2009 to $4.62/share in 2019.

The company raised dividends by 2.60% to $1.20/share just yesterday.

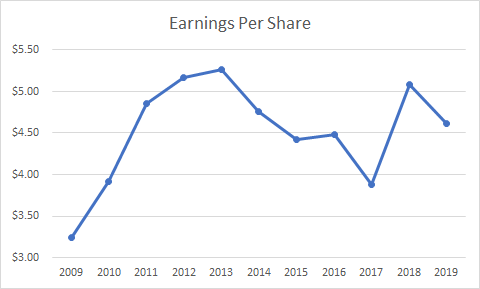

The company managed to increase earnings per share from $3.24/share in 2009 to $4.61/share in 2019.

Philip Morris International Inc is expected to earn $5.08/share in 2020 and $5.61/share in 2021.

The company has been unable to grow earnings per share since 2013. This is unfortunate, because it places a natural limit to how much growth in dividends we can expect. It also puts a natural limit to growth in intrinsic value.

In the future, the company can grow earnings per share through acquisitions, entry into new markets, through price increases that exceed decreases in demand, increase in market shares, through new product offerings (such as e-cigarettes) and through share buybacks. Approximately 40% of the global tobacco market is not accessible easily to PMI. That includes China and India. While PMI decided not to merge or acquire Altria in 2019, this could still happen at some point in the future.

I would be curious to see whether PMI tries to diversify beyond tobacco in the future, into other areas such as packaged food for example or alcoholic beverages. The company is committed to returning 100% of cashflow to shareholders, which it has achieved through dividends and share buybacks.

The tobacco industry is stable, and drowns shareholders in cash. The number of smokers is decreasing in the Developed markets, but staying flat or even slightly increasing in emerging markets. The pace of price increases has historically been enough to compensate for the overall decline in smokers.

While I would not expect high growth for companies like PMI, there are also high barriers to entry. It would be next to impossible to start a new tobacco company in today’s environments.

IQOS Product Success

We also have some competition from alternative sources of nicotine, such as smokeless. PMI is having some success with its IQOS product, which has seen strong growth over the past several years.

There is always the risk of government regulation outright banning the sale of tobacco products or diminishing the brand power of the types of Marlboroughs for example. Given the fact that PMI operates throughout the world, it deals with a lot of governments, which spreads the risk of outright bans. However, it also needs to invest in having the adequate resources to deal with a lot of different governments worldwide as well.

There is also the currency risk, since a lot of developing countries routinely debase their currency against the US dollar. This could be on the headwinds against earnings per share.

PMI generates a third of its revenues from Europe, and a quarter of it comes from Eastern Europe, Middle East and Africa. Asia and Australia account for almost a third of revenues as well, while Canada and Latin America account for about 10% of revenues.

The main positive for PMI is that the company is not dependent on the mercy of a single government and a single market, in terms of unfavorable legislation or bans on tobacco products. For example, the fact that Australia initiated plain packaging laws on cigarettes was not a blow to globally diversified companies like PMI. In addition, even if this plain packaging law spreads to the UK or a few other countries, the diversified nature of PMI’s operations could soften the blow. On the other hand however, it is more cumbersome to deal with 180 governments, which all have different laws and regulations regarding the manufacturing, processing and sale of tobacco products. The fact that a single government entity cannot throw a deadly blow to PMI is a plus. The other positive is that tobacco usage in certain places like emerging markets is actually growing. The downside is that profits per unit are higher in the developed world, and lower in emerging markets. However, consumers in emerging markets may be more likely to trade-up to more premium offerings over the long run, as their income increases over time.

In general, I like PMI because the company has a wide moat. This means that its products have strong brand names, pricing power and loyal customer usage. In addition, PMI usually is number one or number two in most of its major markets in Europe, EMEA, ASIA etc. This strong advantage results in recurring sales and earnings for shareholders for years. This wide moat is the reason why I am willing to sit out any short-term turbulence in Philip Morris International Inc.

Earnings per share growth was aided by share buybacks. Most share buybacks occurred between 2010 and 2014 however, bringing the number of shares outstanding from 1.95 billion to 1.566 billion.

The dividend payout ratio has increased from 69% in 2009 to 100% in 2019. Based on forward earnings estimates, the forward payout ratio is still at a high 94.50%. Most of the dividend growth in the past seven years was accomplished through an increase in the payout ratio. This is unsustainable. A lower payout is definitely a plus, because it provides a margin of safety from short-term turbulence in earnings.

The stock is selling at a forward P/E of 15.82 and yields 5.95%. While the P/E is low and the yield is high, I do not like the lack of earnings growth and the high payout ratio. As a result, I am not interested in adding more to this position.

Relevant Articles:

- Rising Earnings – The Source of Future Dividend Growth

- Are you ignoring investment risks you know about?

- How to get dividend investment ideas

- Philip Morris International versus Altria

The post Philip Morris International Inc (PM) Dividend Stock Analysis appeared first on ValueWalk.

Sign up for ValueWalk’s free newsletter here.

{kind=link}