By Jacob Wolinsky. Originally published at ValueWalk.

Eurizon Asset Management’s investment view and risk scenarios for 2021.

Q3 2020 hedge fund letters, conferences and more

Scenario 2021

In 2021, the global economy should experience positive growth.

As the vaccination campaign progresses, it will become possible to gradually abandon the virus containment policies based on restrictive measures, allowing the economies to open internally and, at a later stage, externally as well.

At least in the initial part of the year, however, restrictive measures will be confirmed, and the economies will need support from the economic authorities. To this end, the ECB has extended quantitative easing until March 2022, the Fed has said it stands ready to introduce new accommodative measures, the Biden administration is negotiating a new fiscal stimulus package with the Republicans, and in Europe work is still in progress towards activating NGEU/Recovery Fund resources.

According to the baseline scenario, the markets should confirm pro-cyclical trends. Short-term interest rates will be kept at their current levels by the central banks, whereas medium and long-term rates should increase. Investors will continue to seek return from risk assets, on both the bond market (emerging bonds, high yield bonds, hybrid instruments), and the stock markets. On the stock markets, the uptrend should be supported more by recovering earnings, and less by higher multiples/lower equity risk premiums.

Macro Economy

- In the opening months of 2021, the combination will persist of restrictive measures to contain the spreading of the virus, and monetary and fiscal support measures.

- In the second half of the year, the effectiveness of the vaccination campaigns in allowing the economies to reopen first internally, then externally, will be assessed.

Asset Allocation

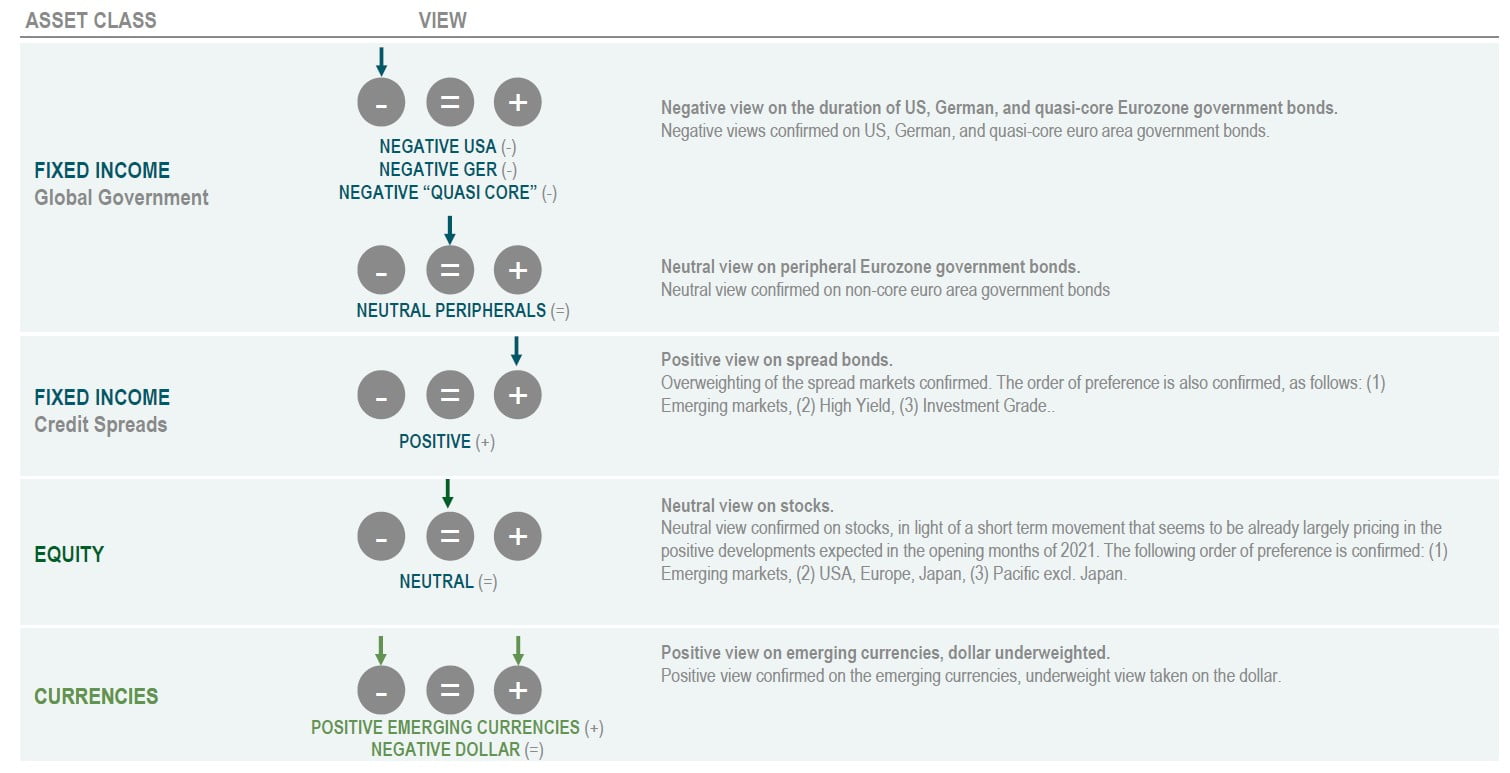

- Pro-cyclical nature of investment choices confirmed looking ahead to 2021, in view of an ongoing recovery of the global economy.

- In the nearer term, the overweighting of the spread markets is confirmed, as opposed to a neutral positioning on stocks.

Fixed Income

- Negative bond coupon flows on German government bonds, and lower than inflation on US bonds, strip these assets of appeal in a global recovery phase. Peripheral euro area government bond rates have almost completed their convergence, especially on the short end of the curve.

- There is still appeal in the spreads offered by emerging bonds, High Yield bonds and, to a lesser degree, Investment Grade bonds.

Equity

- Stock markets appealing in a medium-term perspective, considering the likely recovery of earnings in 2021, as opposed to bond coupon flows reduced to zero.

- On a shorter time horizon, the sharp recovery from the lows hit in March 2020, and the still rather volatile context, could slow the upward movement.

Currencies

- Uncertainty on the fiscal front could weaken the dollar in the immediate term. Positive view confirmed on emerging country currencies.

Risk scenarios for 2021

There are two opposite risk scenarios for 2021.

Any disappointments tied to the diffusion of the vaccines (delays in their administration, or lower than expected efficacy), would trigger a downward revision of growth estimates. In this case, a volatile phase on the markets would be likely, but also a subsequent new round of stimulus measures from central banks and governments. At this point, investors, as they did in 2020, will resume seeking return from risk assets, as the only alternative in a context of low bond rates for an extended period of time.

By contrast, stronger than expected economic growth would be welcome and initially supportive for risk assets, in combination with rising government bond rates. At some point, however, the uptrend of long-term rates would be perceived as hindering the recovery, triggering, as has been the case in the past, a surge in volatility. The subsequent downward reversal of interest rates would act as an automatic stabiliser, enabling the stock markets to subsequently recover.

In the United States and Europe, where the pandemic is still spreading, focus will initially be on the efficacy of the vaccines, whereas the risk of an overheating of the economy would only potentially emerge at a later stage. In China, by contrast, the most unexpected surprise could be a resurgence of Covid infections. More realistically, in China sooner than elsewhere, the debate will begin on the appropriateness of cutting back on fiscal and monetary stimulus, to prevent an overheating of the economy.

- Both risk scenarios, i.e. disappointment and exuberance, may generate volatility, but do not seem capable of derailing the recovery.

Truly serious consequences are only imaginable as the result of policy mistakes, such as failure to offer support in the event of signals of a weakening of growth or, by contrast, the introduction of pre-emptive tightening measures if macro or inflation data were to beat expectations. - However, in 2021, the governments and the central banks will be very careful not to waste all the good work done in 2020.

Investment View

Expansionary monetary and fiscal policies in the first half of the year, and the initial effects of the vaccination campaign starting in the second half, allow for a favourable outlook for 2021. A pro-cyclical approach to investment choices is maintained, underweighting core government bonds, and overweighting spread bonds. Neutral view on stocks, as the near term movement seems to be already pricing in the positive developments expected at the beginning of 2021.

Asset Classes compared

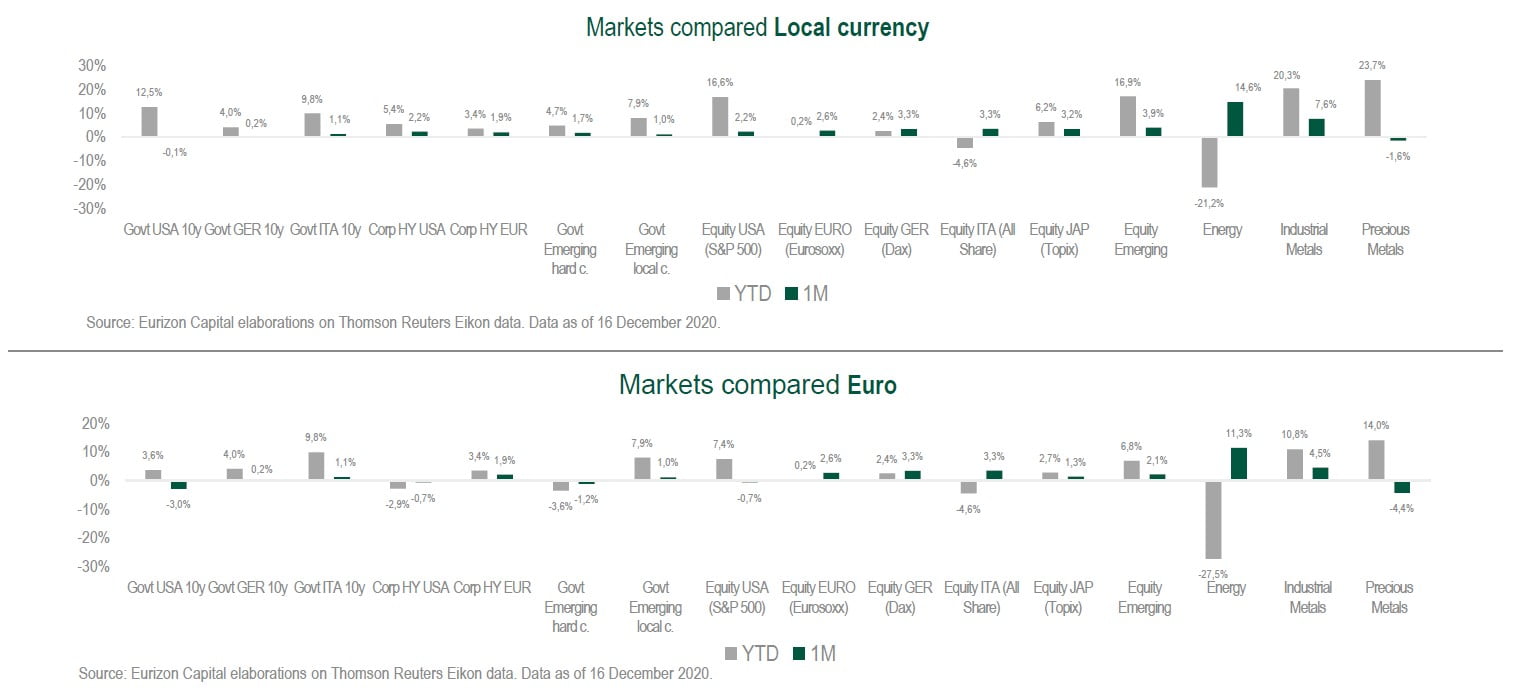

- Positive balance in 2020 for the global stock markets, that recovered swiftly from the March crash, albeit with very mixed performances by geographical region. The US and Emerging stock markets scored substantial gains, whereas European indices are back at the same levels as a year ago.

- Government bond rates dropped sharply in March in the US and in Germany, at the outbreak of the pandemic, and recovered only modestly in the following months.

- Dollar on a downswing since March. BTP-Bund spread at its tightest since 2018.

The post Risk Scenarios And Investment View For 2021: Eurizon appeared first on ValueWalk.

Sign up for ValueWalk’s free newsletter here.

{kind=link}