By Jacob Wolinsky. Originally published at ValueWalk.

Symmetry Invest A/S letter for the second half ended December 2020, discussing WANdisco.

Q3 2020 hedge fund letters, conferences and more

Purpose of this Newsletter

Every month, Symmetry sends out a portfolio update to the shareholders. In them, we report the last month’s return, news regarding our investments, and much more. In addition, we send out write-ups and a yearly investor letter analyzing our biggest positions. This newsletter will not replace our copy of the above-mentioned activities, since they are issued exclusively to Symmetry’s shareholders. The free newsletter will therefore to a very limited extent be able to reflect on individual holdings, as this is reserved for our shareholders. Instead, this newsletter will touch upon general trends and developments in the markets and explain how Symmetry navigates them.

The newsletter will from time to time discuss specific stocks in which Symmetry could have a long or short position in, or no position at all, but an interest in.

The newsletter aims to increase awareness of Symmetry for all our stakeholders, including current investors, potential investors, and others who follow the stock market. Symmetry will continuously describe our strategy and make it as easy to understand as possible for readers.

We will, among other things, include quotes from well-known value investors and substantiate claims with graphs and other material that can be used to support our point.

We hope that as many people as possible will find the material useful and easy to read and that it will help sign up new people to the newsletter to follow us.

Nyhedsbrev

When I hopefully look back in 50 years on the dawn of Symmetry, I am convinced that I will explicitly remember 2020.

In the following newsletter, we will go through two main topics. We will express our view of general management interactions, and also review what we call inflection point investing, and provide an example of a stock that might be close to its inflection point.

As always, returns and portfolio updates, etc. are sent out to shareholders monthly on the website.

We will publish our yearly investor letter in March/April in which we will provide an in-depth analysis of the year that has passed and our portfolio holdings.

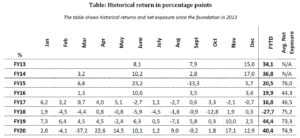

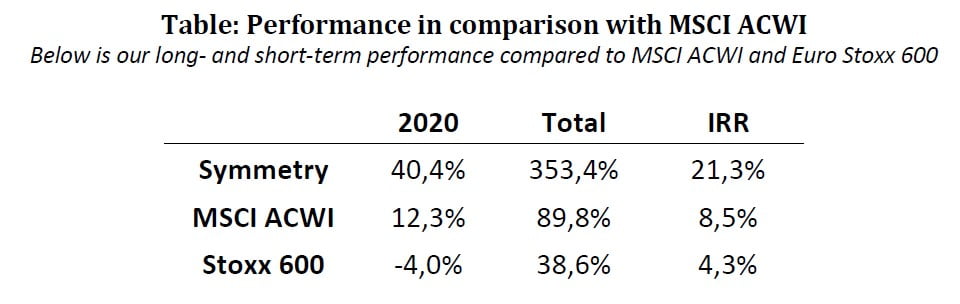

2020 proved to be yet another year when Symmetry comfortably beat the market, and we have now beat the market in 7 out of 8 years since the inception. Our IRR amounts to 21,3 % net (+25% gross), again significantly better than the market. Ending up with such a great year was not expected at the end of March. Even if we recognized that our holdings looked extremely cheap and that we could add to the positions at a low valuation, I still had the feeling that it would take many years before we would recoup the losses incurred. In the end, it took no more than 4 months before we saw new all-time highs for the year.

With that being said I am not overly happy about the year 2020. On the positive side:

- The learning curve has been extremely steep. I feel I have become a much better investor going out of 2020 than coming into the year.

- The idea generation process and risk management process seems to be working much better

- We never panicked doing the March selloff and managed to use the drawdown as an opportunity to add more exposure to our book.

- I have learned even more smart people do know, my network is becoming better each day and I have smoothly hired the first portfolio manager to run Symmetry alongside me.

On the negative side:

- Our initial drawdown in march was too big. We should have done better here and is paid to do better

- Even through we took on more exposure as March went by, we should have been more aggressive. As Warren Buffett famously quoted “when it rains gold, put out the bucket, not the thimble”. In March 2020 I used a thimble instead of a bucket, an error I hope not to repeat next time.

- We could have been even more dynamic around opportunities and events. Of course, it’s easier to move around 1 mio. DKK than +100 million DKK. But we have opportunities to trim positions and move into more attractive ones that we missed.

Overall, I would give myself a B- for the year. Fortunately for me Henriks contribution definitely falls into the A category leaving Symmetry somewhere in the middle.

Control of FOMO:

These days it seems on social media that the average return for most investors in 2020 was +100 % with bad investors doing 50 % and the real starts doing 300-500 %. Judging on the results on Fintwit we at Symmetry should feel really shitty about our 40 % net and around 50 % gross for the year. Here one has to remember the huge selection bias there is on social media. For every 1 person disclosing how well things are going there is probably 5-10 not showing anything. Also, the next year its probably other people that have good returns than the ones this year. This way people following fintwit will always end up only seeing the top 10 % portfolios each year. And many people run with many different portfolios always showing the best one each year.

So how do I control the FOMO feeling connected with seeing everyone having much better return that ourself?

In our Q1 2019 newsletter I talked about the difference between running a private portfolio and a fund: Microsoft Word – Q1 2019 Nyhedsbrev (english) (symmetry.dk)

In the newsletter I showed the following table from my personal SAXO bank account prior to opening up Symmetry Invest:

I actually have this 3-year CAGR of 172 % per year printed out in the office. For outsiders this could probably look as a way to boost my own ego. But actually, the opposite is the truth. This works as a way for me to control my own FOMO. It reminds me that I was also having totally outsized returns managing only my own small amount of money. And it reminds me what the goal of Symmetry is. We have a goal of compounding investors capital net of fees and expenses at a CAGR of around 15 % per year. So far, our 21,3 % is ahead but we have also had the wind in our back instead of in our face for most of the time.

Just to be clear, this is in no way to disrespect anyone. I know a huge amount of really smart people in the investment business and my Fintwit friendships has been a huge positive contributor to Symmetrys return in 2020 and hopefully going forward. I would never want to be without that community.

As Charlie Munger puts it:

FOMO have always been one of my biggest weaknesses as an investor. But I can say for sure that it’s something I have been working extremely hard on improving over the years. So far, I would say I have done a great job improving but still have plenty to do in the future.

CEO Interactions:

Prior to an investment, we find it important to interact with, and assess the management, particularly with CEO’s so that we can form a real impression of their personalities and management capabilities. Much of our focus is aimed at understanding how the CEO is thinking about the future and the business model. Do their plans align with ours, do they understand capital allocation and invest long-term, and do they try to build a tangible company culture?

How often should you talk to the CEO, and is it a good idea for the CEO to talk to investors?

Following an investment, the question that arises is: how often should one oversee that investment? Naturally one should monitor the quarterly results, other meaningful KPIs, and the general trends that will affect the company. But how often should one talk to the CEO afterward? Symmetry’s approach is that we conduct regular follow-ups through e-mail and meetings in connection with their roadshows and quarterly or half-year reporting. If there are other significant things to discuss, this will be done through e-mail in between these events.

We have heard about another manager that held 2-3 meetings daily with the CEOs of a limited number of companies. This raises the question of whether the manager really trusts the long-term value creation process of those CEO’s? I one has to validate the investment thesis this regularly its probably not a good thesis at all.

And even more relevant, will the meetings not take up way too much time for the CEO? Would the manager appreciate it if the CEO also talked to 20-30 other fund managers every single month?

But how much is too much? Some companies have followed the mindset of Warren Buffet, where one holds a single annual meeting where there is an opportunity for questions. Beyond this, only written material is sent out, and they do not talk to the analysts etc. Our view is that this doesn’t hold up in the modern world. The companies will need to keep investors and other stakeholders regularly updated on what is happening in the business, among other things to keep the cost of capital down. But concerning the CEO, our opinion is that they should only have to spend a few days in connection to the quarterly and half-year reports with IR work. The rest should be spent on the business.

As a result, our opinion is also that a company needs to have a strong IR department:

IR departments role:

Our view is that one of the biggest mistakes many companies make is to not invest enough in hiring a skilled head of IR. In many cases, the head of IR is often a kind of “communication employee”, who is skilled at answering in a politician’s way, answering without really answering anything. Skilled investors will quickly get tired of this behavior and instead turn to the CEO for answers and meetings.

This means that CEOs end up having to spend way too much time talking to investors instead of nurturing the business. In cases where companies manage to hire competent and skilled IR employees, they can often exempt the CEO from many tasks, since the IR person can answer the bulk of investors’ questions.

The best example of this that I can recall was Rachel Gravesen who was the former head of IR at the Danish firm Genmab, a company that Symmetry (and me personally for some years before Symmety’s founding) owned a significant position in. In all that time, I only talked to the CEO Jan Van de Winkel two or three times thanks to Rachel’s knowledge of the business. If I had questions of a more technical nature regarding the products that she couldn’t answer at once, she always came back later with an answer. This freed up time for Jan to attend more “high-end” IR work, like attending big events.

Another example is a smaller Swedish company where we recently had a 2-hour long conversation with the newly appointed head of IR, who was recently recruited after being an analyst covering the particular company for many years. He had a deep knowledge of the industry and the business, and we have not needed a meeting with the CEO yet because of this (we do not own the stock yet).

We believe that the case could be made for smaller companies, in particular, to invest in a better IR department. It would cost a little bit more, but if it frees up time for the CEO, the money will often be well spent. And just to be clear: we know a lot of really good IR people – so we don’t generalize everyone.

Inflection Point Investing:

One of the things we have had a lot of success with is what I call Inflection Point Investing. When we buy a new share and possibly write a report on it, we as investors see the result of our work. But often, a very long period precedes that investment, and it is only a fraction of the stocks that we look at that we end up buying in the end.

Very often, timing is crucial when you want to buy a company. The underlying business must be in a solid position, and the valuation must be attractive at the same time. We often cover many attractive companies that we believe have underlying strong business models and market positions, but where the timing is not right. By following them closely, we are ready to invest when the companies reach their “inflection point”, ie. the time when we think their business models will finally break through and show their worth. It could also be situations where big sellers put pressure on the stock, but we can see that the selling is about to end.

This type of investing is not for everyone. Many investors do not have the time and energy to try and time their investments and simply resort to finding attractive business models and purchase the shares. But in Symmetry our return on investments is very high, and since we almost always have an abundance of good ideas, we will almost always have an alternative place to invest the money. Therefore, we are not interested in entering a position until both the valuation is low, and the business is booming.

A good example of this is GAN:

We have been following GAN for a long time while it was a small AIM-listed stock. The company had gained a strong market position in New Jersey when the state opened up the market for online casinos in 2014, and also exhibited solid growth and a compelling market position in Italy. But at the same time, it was loss-making, had to constantly raise new capital and the growth was not “overwhelming”. We still spent time familiarizing ourselves with the company, as we could see that their market position in the US could become a strength in due time. The first crucial news came in mid-2018 when the PASPA rule was removed, and all states in the US were free to self-regulate sports betting and casino. This presented itself a clear opportunity for GAN, but as they still did not have a sports betting product, we bided our time. When Pennsylvania, in 2019, also allowed sports betting and casino, and we saw how Fanduel/Betfair started to gain a strong market position building on GAN’s platform, we initiated a purchase. At the time the stock was still only increasing slightly, and the financials were still not good (it takes time for leading KPIs to affect the numbers). We continued to buy in light of willingness from more states to open up, and GAN signing on more and more customers. In May 2020, GAN chose to substitute the small AIM exchange for Nasdaq in the US. As reported revenue began to rise +100% YoY and margins followed, the stock reacted strongly. The stock thus ended up rising 1.000% from mid-2018 to mid-2020. Even during 2019, one could still buy the stock for 3-8 USD (the stock was listed in the UK and in pence at the time). Today it is traded for approximately 20 USD.

GAN is therefore a great example of how you can follow a company for a long time, do your analysis, and be ready to buy in when the business model is facing the crucial inflection point.

Naked Wines Plc:

Another good example is Naked Wines, which we have written about earlier. We first learned about Naked Wines at the start of 2017 and chose to spend time analyzing it. From the start, we were intrigued by their online business, but at the time most of the revenue was derived from their physical wine shops in England. With declining revenue and Brexit around the corner, we did not feel fully comfortable with this segment. During 2019, the stock fell to a level where the discount warranted a minor purchase. At the end of 2019, when the company announced the sale of their retail business and was left with Naked Wines and a large pile of cash, we seriously stepped up our due diligence process. Still, we were not completely comfortable with the shareholders of the company. More and more of the revenue came from the US, where the executives were living, but the shareholders were mostly UK based dividend investors. Towards the end of 2019, the inflection point came when 3-4 major US investors, through heavy purchasing cleared out the sellers. We then started to buy aggressively. This also increased the reputation of WINE in the market as a majority of investors now owned the stock because they anticipated promising opportunities for the online business. We followed suit and started to buy the stock, and when COVID hit and the business got another boost we continued to buy over the spring.

The process, therefore, resembles the one applied in GAN very much. We followed WINE for a long time, liked the business model but lacked the crucial “inflection point” at which the purchase should be made.

WANdisco plc:

A stock that could be close to it’s “inflection point” at the moment is the British company WANdisco. We have been following the stock for quite some time, but it wasn’t until the summer of 2020 when we seriously started to get interested. At that time, we thought there were way too many uncertainties and the valuation weren’t attractive enough. At the end of the year, we bought a small position, and at the beginning of 2021, we increased that position given the positive news from the company that still hadn’t materialized in a rising share price. WANdisco has been a controversial stock for many years with super optimistic management that have made promises they’ve been unable to keep. At the same time, the CEO has had a lavish lifestyle and foundations/charities to spend money on. This led to him selling off shares over time, even after raising funds. In many cases they have had to make profit warnings closely afterward, looking very bad on paper.

Based on our conversations with David and the team, we have no concerns regarding their professionalism and competencies as well as their understanding of the business. Our concern has been centered around if whether their ethics/morals are good enough for us to invest in them.

However, several factors speak in favor of an investment:

1) There is a bit of a “fake it until you make it” vibe about their history. Things have taken much longer than they promised the market, with constant postponements. They have also needed constant funding and have had to spin a story to keep it coming, showcasing a more Silicon Valley mindset than the normal European corporate governance way. But the crucial thing for us has been that we haven’t seen examples of the management directly lying or cheating. They have just been too optimistic in many aspects. What is important henceforth is not how much they historically have “faked it” as long as we are convinced that they now can “make it”.

2) Several of their strategic changes have been necessary even though they have been tough. The company has had a good growth journey and been profitable in prior instances but believed that their technology could unlock far greater value by a change of focus towards a bigger market, etc.

3) The majority of the postponements/delays have been beyond their control. Also, it looks like Microsoft have tried to squeeze them a little, to facilitate an acquisition.

4) The management expected around 50 new customers via Azure the first 12 months following the launch but delivered 46 within 2 months. In this instance, they have so far delivered more than promised.

Furthermore, one should also remember that the stock market often views the management in snapshots given the situation they are currently in. Right now, many investors see David as unreliable and one with pipe dreams. One should however remember that if the company reaches its guidance for 2021, people will praise him and explain how excellent it was that he prioritized long-term value creation over short-term revenue – a CEO that dared to make bold decisions. The track record is absolutely an important parameter when you assess the management, but it is also important to remember that the track record often depends on from where and to when you measure.

Everyone knows that I’m not the biggest fan of Elon Musk and Tesla, but one should still have to recognize what Elon Musk has created (which made him the second richest man in the world). Without comparing him with David at all, he also created Tesla by constantly promising things he could not keep and being over-optimistic. He sold a vision as much as a real business. I’m still not 100% sure that Tesla will get there, but at the moment they have been profitable for three quarters in a row and have been able to raise capital at very high valuations. Right now, most people talk of Elon Musk as a visionary that dared to invest in electric cars when no one else did, even though it was unprofitable from the get-go.

So, let’s instead look at WANdisco today based on facts.

What is WANdisco?

WANdisco is the leading player in data migration of Hadoop data to the cloud. When companies with large on-premise servers with data want to move to the cloud, they can use WANdisco to migrate that data.

There are several different solutions to migrate static data (i.e., backups that never changes). There are also some solutions that can migrate smaller amounts of data that is actively changing. WANdisco is the only solution that can migrate large amounts of data that is constantly changing.

Unless you’re dealing with pure archive data, most data lakes in companies are constantly changing. This is because almost all companies’ applications, websites, emails, etc. go through their databases.

To get the most out of this data, many companies chose to move from on-prem to the cloud. They will come to Wandisco for help with this shift.

Based on our research, and the conversations we’ve had with people in the industry, we have verified that other solutions will work, but none that can handle the type of complex situations that WANdisco can.

For example, Google Cloud uses a solution called Dual Ingest. The disadvantage of Dual Ingest is that data is copied to two locations where the data always must be identical. I.e., if there is a delay or problem with one of the units it will take massive amounts of manual work to get it up and running and maintained, during the migration.

Amazon (AWS) used (“used” because they’ve adopted WANdisco now) a technology called Snowball which bluntly can be described as a big USB-stick (huge trucks) that upload the data and then drives it to an AWS server. The problem here, of course, is that it takes time, is expensive, and will be useless if data changes along the way.

In October, WANdisco launched their two products LiveData Plane and LiveData Migrator as an integrated migration solution directly in Microsoft Azure as a simple white label solution. At the same time, Amazon AWS also uses WANdisco as their recommended solution for data migration. We will review later why we believe it is a gamechanger that WANdisco now has the two largest cloud players in the world to recommend WANdisco’s solution.

As displayed in the figure above, the migration follows a connection by the customer’s on-prem server to the Azure cloud (online). From there, the customer can connect the data migrations from Hadoop to ADSL GEN2. The first 25 TB of data is free, after which they pay by usage depending on the amount of data. When the data is migrated, customers can utilize Livedata Plane for a constant synchronization between cloud and on-prem. WANdisco continuously earns recurring revenue from the amount of data that is kept synchronized as well as from the number of changes that occur that need to be duplicated.

Why would the customer choose this solution? There are several reasons; the need to get their data in the cloud is great, to be able to take advantage of the speed and analytical solutions found there. But at the same time, many companies find it valuable to have a local backup through their on-premise. Many sectors (financial services, medical, etc.) are even required to keep a local backup.

The actual data migration can be done in a few days or weeks via WANdisco, but most applications that a customer has built on his on-premise will need to be rebuilt in the cloud. I.e., the programs and modules (website, etc.) that send data to on-premise often have to be rebuilt in the cloud to work there. It’s, therefore, crucial for the company to have a solution that can ensure that the data will be available in both places as long as they have some applications in both places. Depending on the size and complexity of the company, it can take several years to run a complete migration, during which the customer will be dependent on having LiveData Plane connected.

History:

Data is the new gold. It is gradually becoming a common belief that most companies’ way of winning customers and creating unique business models is by understanding, acquiring, storing, and using data to their advantage. But this was not always the case.

Before Hadoop, servers were often very poor at storing so-called unstructured data. Most of the data we receive today is unstructured (social media, e-mail, website traffic, etc.). This changed with the invention of Hadoop which is open-source software. Many companies invested heavily in Hadoop databases throughout the ’90s to be able to structure their data better. There were also companies (especially Cloudera & Hortonworks) that made a business of advising/selling Hadoop systems.

This has changed primarily after Amazon launched AWS (and Microsoft and Google etc. followed). From there on cloud solutions took over as the preferred solution from Hadoop.

As one can see in the graphs above, the interest in Hadoop began declining in tandem with the increase of interest in Azure. The same picture emerges if you compare Hortonworks and Databricks (analysis of Hadoop and Cloud data, respectively).

WANdisco initially made good money by selling licenses to Hadoop focused businesses, but as management realized that the future was in the Cloud, they were forced to change the strategic direction of WANdisco.

Read the full letter here.

The post Symmetry Invest A/S 2H20 Letter: WANdisco appeared first on ValueWalk.

Sign up for ValueWalk’s free newsletter here.

{kind=link}