By Jacob Wolinsky. Originally published at ValueWalk.

Key Takeaways

- We expect global issuance in sustainable debt to surpass $700 billion in 2021, driven by an acceleration of green-labeled bond issuance and continued growth of other sustainable debt instruments, including social and sustainability bonds.

- Innovation within the sustainable debt market will continue as new types of instruments, including sustainability-linked loans and bonds, expand rapidly and diversify the ways issuers and investors contribute to sustainability objectives.

- Net-zero emissions commitments from the largest economies globally will require significant investment and indicate the dominance of green debt will continue.

- We may also see the continued extension of the use-of-proceeds model to transition bonds for companies operating in more carbon-intensive, transition sectors.

- Improved transparency and reporting practices remain key to fostering credibility in the sustainable debt market.

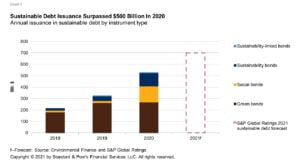

S&P Global Ratings expects issuance of sustainable debt–including green, social, sustainability, and sustainability-linked bonds–will surpass $700 billion in 2021. This would take cumulative issuance past the $2 trillion milestone, from $1.3 trillion as of year-end 2020. Sustainable debt issuance exceeded $530 billion in 2020, according to Environmental Finance, up a staggering 63% from 2019. Social bonds emerged as the fastest growing segment of the market (chart 1), growing about 8x in 2020, catapulted by the COVID-19 pandemic and growing concern about social inequities. As issuer attention shifted toward financing pandemic aid and ensuring recession relief measures, green bond debt slowed in the first half of the 2020. However, it rebounded in the second half, reaching a record annual issuance amount of $270 billion and indicating that issuer and investor appetite for financing climate response and other environmental objectives is strong and accelerating. We believe green-labeled bond issuance could exceed $400 billion in 2021, as global political and regulatory actions grow, serving as a catalyst for increased sovereign and private issuance. We also believe the green use-of-proceeds model will expand to include transition finance, aiding high-carbon-emitting sectors to finance their transition into net-zero emissions business activities.

The COVID-19 pandemic highlighted the need for resilience across societies so they could better withstand high-impact shocks, including those related to health, safety, social fragmentation, and climate change. As this theme becomes more prominent, the connection between social inclusion and the environment will strengthen, and the effect will spill into the capital markets, leading to a rise in instruments targeting broader sustainability objectives. As a result, we believe innovation and diversification within the sustainable debt market will continue in 2021. We expect to see rapid growth of sustainability bonds, which target both social and environmental objectives, as well as greater interest in sustainability-linked instruments. In addition, as the transition to a net-zero economy concept gains traction, we believe new sectors and issuers will enter the market, expanding the pool of investable sustainable financing and allowing investors to diversify their contribution to sustainability objectives.

We Expect The Sustainable Debt Market Will Grow Significantly In 2021

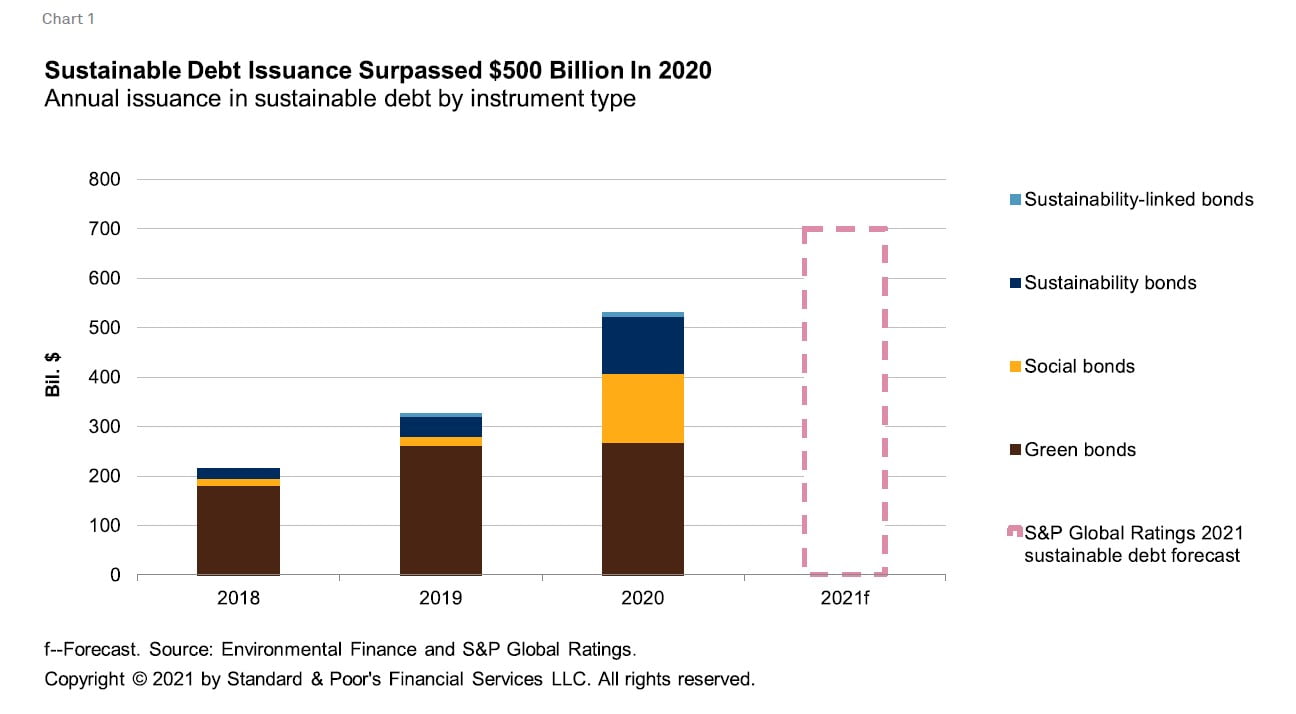

Similar to how the green bond market was spurred by climate policies and the transition to a low-carbon/net-zero economy, we believe greater interest from organizations and investors in social risk factors has had a galvanizing effect on social and sustainability bond issuance. Non-green bond issuance made up almost half of the total sustainable debt market in 2020, up from less than 20% in 2019, according to Environmental Finance. We believe investor appetite for other sustainable debt instruments will complement the continued expansion of the green bond market in 2021. We believe public issuers–including sovereigns, local governments, and government-backed entities–will play a key role in the growth of newer instruments, given their wide social and societal mandate.

Sustainable Debt Instruments Defined

The International Capital Market Assn. defines green bonds as use of proceed bonds that enable capital-raising and investment for projects with environmental benefits including renewable energy, green buildings, and sustainable agriculture. Social bonds raise funds for projects that address or mitigate a specific social issue and/or seek to achieve positive social outcomes, such as improving food security and access to education, health care, and financing, especially but not exclusively for target populations. Sustainability bonds target both environmental and social benefits. Sustainability-linked bonds and loans are a relatively new class of instruments that provide incentives for issuers and borrowers to set and achieve predetermined sustainability performance targets.

We believe green-labeled bond issuance could reach $400 billion in 2021. The COVID-19 pandemic led to a temporary slowdown in green bond issuance in the first half of 2020 as issuers switched their attention to addressing social objectives, namely health and safety, over environmental ones. However, in the third quarter of 2020, green bond issuance rebounded 21% over the second quarter, with $69.4 billion in issuance reported according to the Climate Bonds Initiative (CBI), the highest recorded in any third-quarter period. By year-end 2020, the green bonds market reached a significant milestone, exceeding $1 trillion in issued bonds since the first issuance in 2007. In our view, this growth reflects, in part, a surge in fixed-income issuance globally because of significant liquidity support from central banks and a faster-than-expected rebound in economic activity (see: “Global Financing Conditions: Bond Issuance Is Expected To Finish 2020 Up 16% And Decline In 2021,” published Oct. 26, 2020). It further reflects the continuous acceleration of climate-related policies globally, including as part of countries’ recovery plans. Inaugural sovereign green bond issuances in second-half 2020, including the €6.5 billion bond issued by the German government, the largest ever single green bond to date, as well as Sweden’s $2.3 billion inaugural green bond, were also pivotal for market growth.

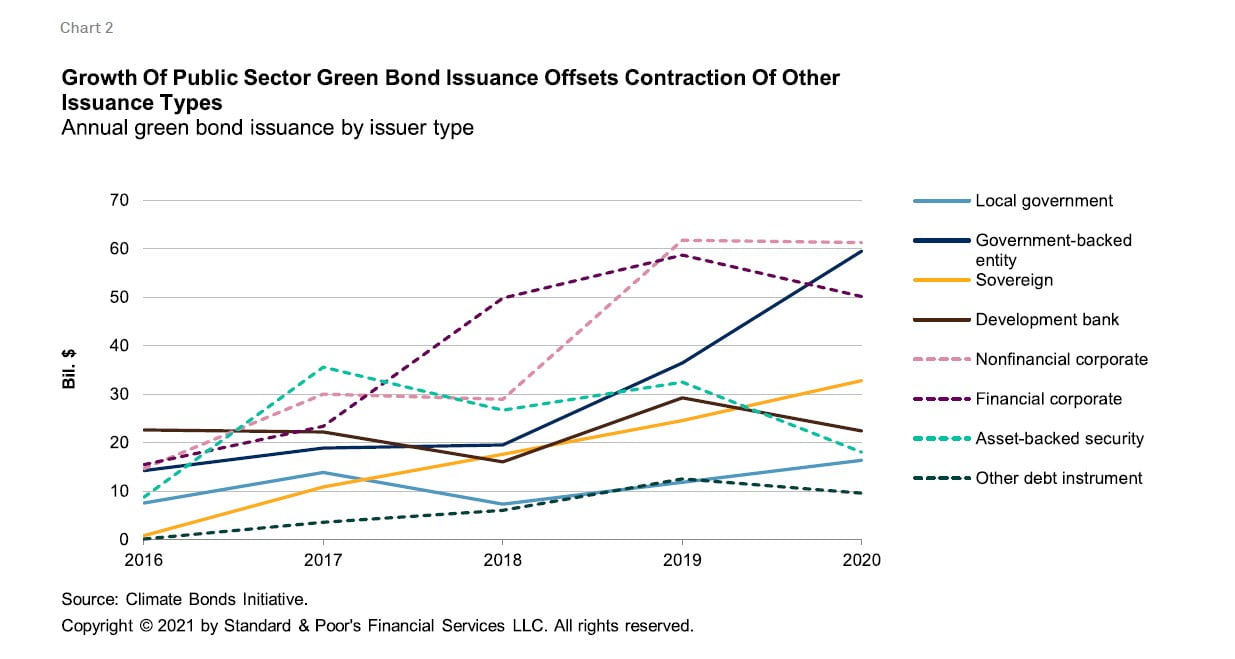

Net-zero emissions pledges will spur green-labeled issuance, particularly in the EU. We expect Europe’s share of the green bond market (54% in 2020 according to CBI) will continue to grow, particularly as green bonds are issued to finance technologies that help meet the EU’s transition to net-zero carbon emissions by 2050. European Council President Charles Michel has proposed using 30% of the €750 billion Next Generation EU COVID-19 recovery plan to target climate-friendly projects, translating to a potential €225 billion of additional green financial instruments (see: “The EU Recovery Plan Could Create Its Own Green Safe Asset,” published July 15, 2020). Italy, Spain, and the U.K. are among European nations planning to sell their first sovereign green bonds in 2021. CBI predicts 14 sovereigns could issue inaugural green bonds during the next two years. We believe changes in environmental legislation and regulation will likely increase pressure for action from the private sector and lead to further follow-on green issuance.

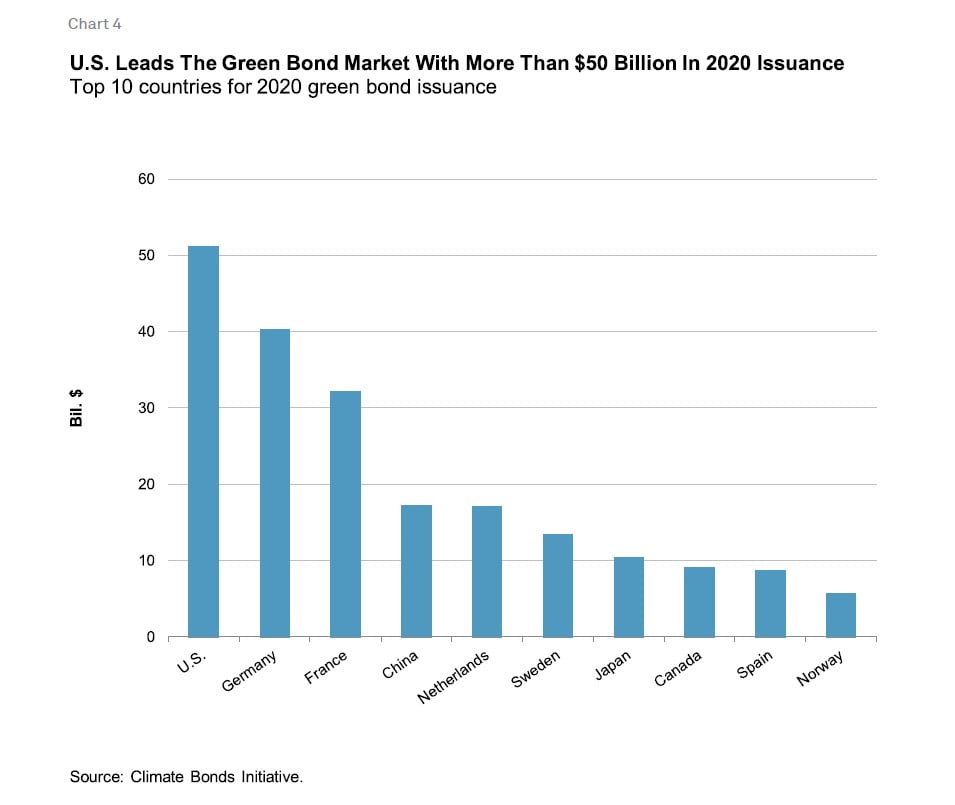

However, growth in the green bond market will not come from the EU alone. U.S.-based issuers have been leaders in the green bond market over the past few years, ahead of any other country, composing more than $51 billion or 19% of total issuance in 2020 (chart 4). We expect the U.S. will maintain its dominant position in the market, given the ambitious set of environmental priorities set out by President Joe Biden’s administration, which include achieving a 100% clean energy economy and reaching carbon neutrality by 2050. In addition, Biden’s climate and environmental justice proposal includes federal investment of $1.7 trillion over the next 10 years, which could attract private markets to crowd into the green bond space. The real estate sector has dominated U.S. green bond issuance, but other sectors–including renewables and transport, which are a focus under Biden’s plan–have also seen large-scale issuance, showing “capacity and appetite to fund a more ambitious environmental drive,” according to CBI. We are also likely to see an uptick in green bond issuance in the Asia-Pacific region as China and Japan aim for carbon neutrality by 2060 and 2050, respectively. These commitments will require significant investment and indicate strong green debt market growth will likely continue in 2021 and beyond.

Transition bonds may emerge as a complement to green-labeled financing. Green financing has been almost solely directed at activities that are considered already green, according to CBI. The largest carbon-emitting industries and companies–including those in the materials, oil and gas, chemicals, and transportation sectors–are still largely absent from the market because they do not have sufficient green assets to issue green bonds. Concerns have grown that there are not enough green assets to absorb the amount of capital needed to meet the Paris Agreement’s climate change goals. Transition bonds provide a potential solution by enabling carbon-intensive companies to raise capital and use the proceeds for activities that help them reduce their carbon footprint. Only a few transition bonds have been issued thus far, because no unifying definition of transition exists in the market. However, we believe these bonds may play a much more important role in the sustainable debt market in 2021, particularly as standards for transition instruments become more comprehensive and robust.

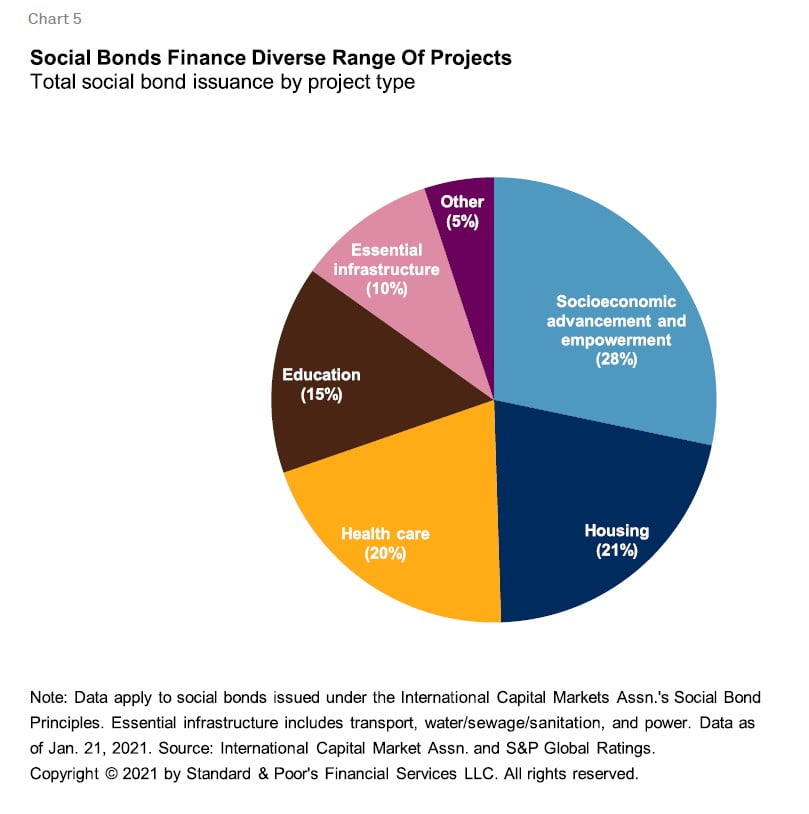

After a breakthrough year in social issuance in response to the COVID-19 pandemic, we expect social bonds will maintain a prominent place in the sustainable bond market. The pandemic has heightened issuers’ and investors’ interests in the vast social inequalities and justice issues–including rising unemployment, income inequality, and strains on housing, health care, and education systems–that exist around the world (see “Sustainable Finance Addresses Social Justice As COVID-19 Raises The Stakes,” published Nov. 10, 2020). Massive social bond issuance by the EU under its Support to Mitigate Unemployment Risks in an Emergency (SURE) program was a major indicator of growth in the market. The EU raised €39.5 billion from SURE social bonds in fourth-quarter 2020 alone. In the Asia-Pacific region, social bonds outpaced issuance of green bonds for the first time as banks and sovereigns turned their attention to financing health care, employment programs, and other social development projects in many of the region’s vulnerable communities.

The pandemic’s legacy and implications, particularly as they relate to social justice, will persist. As a result, we believe that even in a post-pandemic world, the calls for equitable, sustainable growth will continue to be heard in the capital markets, leading to further growth in social bond issuance. We have already seen rapid diversification in the types of projects financed by social bonds, and we believe this will continue in the longer term as new financed categories emerge, targeting areas such as economic recovery, diversity and inclusion, and improvement of basic essential services including vaccine manufacturing and distribution.

Sustainability-linked instruments are gaining traction as the sustainable debt market diversifies. Sustainability-linked bonds (SLBs) have historically composed a very small part of the sustainable-debt market; only a few issues are outstanding. However, several factors indicate this category of instruments may experience significant growth in 2021. Unlike green, social, and sustainability bonds, which rely on proceeds being allocated to specific green or social projects, SLBs give companies incentives to advance their sustainability agendas more broadly by directly linking their cost of funding to the achievements of specific sustainability performance targets (SPTs). In June 2020, the International Capital Markets Assn. (ICMA) published the Sustainability-Linked Bond Principles (SLBPs), outlining the five core components of an SLB: key performance indicators (KPIs), SPTs, bond characteristics, reporting, and verification. By providing guidance on best practices for issuance, we believe the SLBPs will promote a sense of legitimacy in the market. Large corporations, including French fashion house Chanel and Brazilian paper and pulp firm Suzano, are some of the recent sustainability-linked bond issuers, and we expect more companies to follow suit as market integrity and transparency efforts grow. In addition, the European Central Bank announced that starting in January 2021, it will accept sustainability-linked bonds as eligible collateral and also start buying them under its asset purchase programs, which should further stimulate growth of the market and help establish best practices for the instrument.

Transparency And Reporting Remain Key

Regulations and principles have played a key role in advancing the best practices for use of proceeds and impact reporting. ICMA’s Green Bond Principles, Social Bond Principles, and Sustainability Bond Guidelines (collectively the Principles), promote the standardization and integrity of the use-of-proceeds market by ensuring that bond proceeds are used exclusively to finance or refinance green and/or social projects and recommending best practices related to transparency, disclosure, and reporting. Furthermore, the EU Taxonomy–a classification system that establishes a list of environmentally sustainable economic activities and requires issuers to report on the environmental objectives of their green bonds–is expected to create a greater sense of credibility in the green bond market. We expect the EU Taxonomy and other similar frameworks will promote the growth of the sustainable debt market as they provide financial market participants with additional resources for assessing the sustainability merits of an investment. While significant progress surrounding transparency and reporting has been made, there is room for improvement, particularly with the newer categories of bonds (i.e., social and transition), for which impact assessment is less standardized. In our opinion, robust disclosure practices, ongoing standardization, and the use of qualified third-party reviews could mitigate some of these risks.

Looking ahead

The sustainable finance landscape is growing and evolving as new financing instruments, including transition and sustainability-linked financing complement green, social, and sustainability bonds. We believe growth in these instruments will be global, accelerated by ambitious environmental commitments and the call for a greater focus on mitigating social risks. In our opinion, improved transparency and reporting practices are key to fostering credibility and propelling future issuance.

Related Research

- Stakeholder Capitalism: Aligning Value Creation With Protection Of Values, Jan. 19, 2021

- Sustainable Finance Addresses Social Justice As COVID-19 Raises The Stakes, Nov. 10, 2020

- A Pandemic-Driven Surge In Social Bond Issuance Shows The Sustainable Debt Market Is Evolving, June 22, 2020

- People Power: COVID-19 Will Redefine Workforce Dynamics In The Post-Pandemic Era, June 4, 2020

- The ESG Lens On COVID-19, Part 2: How Companies Deal With Disruption, April 28, 2020

- The ESG Lens On COVID-19, Part 1, April 20, 2020

The post Sustainable Debt Markets Surge As Social And Transition Financing Take Root appeared first on ValueWalk.

Sign up for ValueWalk’s free newsletter here.

{kind=link}