By Jacob Wolinsky. Originally published at ValueWalk.

Prescience Point is long Groupon Inc (NASDAQ:GRPN).

Q3 2021 hedge fund letters, conferences and more

Most people think Groupon is dead (we did). However it has a valuable secret asset, revamped core business poised for accelerated growth, & surprisingly loyal user base, making it worth 2.7x to 4.3x the current share price.

Groupon, Inc. (GRPN) is a misunderstood Company that has been wrongly left for dead due to an antiquated bear thesis and apathetic sell-side. Market participants have completely overlooked the sizable and growing value of Groupon’s investment in SumUp, and are significantly undervaluing the Company’s core business, which has recently stabilized and is poised for significant growth. We believe shares are worth at least $63.18 today and could exceed $98.00 in a conservative upside scenario.

Prescience Point Research Opinions:

- The market has completely overlooked Groupon’s sizable ownership stake in SumUp, which we estimate has grown to at least $268m or close to 40% of the Groupon’s current enterprise value: In 2013, Groupon made a small initial investment in SumUp, a fast-growing fintech with a +50% revenue CAGR. Today, the investment is worth at least $268 million yet it’s been largely overlooked by market participants. Even after a recent ~$90 million book value mark-up of the investment, sell-side analysts covering Groupon have continued to overlook its existence.

- Factoring in the SumUp investment, the market is valuing Groupon’s core business at just 2.9x consensus FY 22E EBITDA; at this extremely cheap valuation, very little has to go right in order for Groupon shares to increase substantially from current price levels: After deducting the value of the SumUp investment, which we estimate to be worth at least $268m, from the current enterprise value, we calculate that the market is valuing Groupon’s core business at just 2.9x consensus FY 22E EBITDA. This valuation represents a massive 66% discount to the Company’s historical average multiple of 8.7x forward year EBITDA.

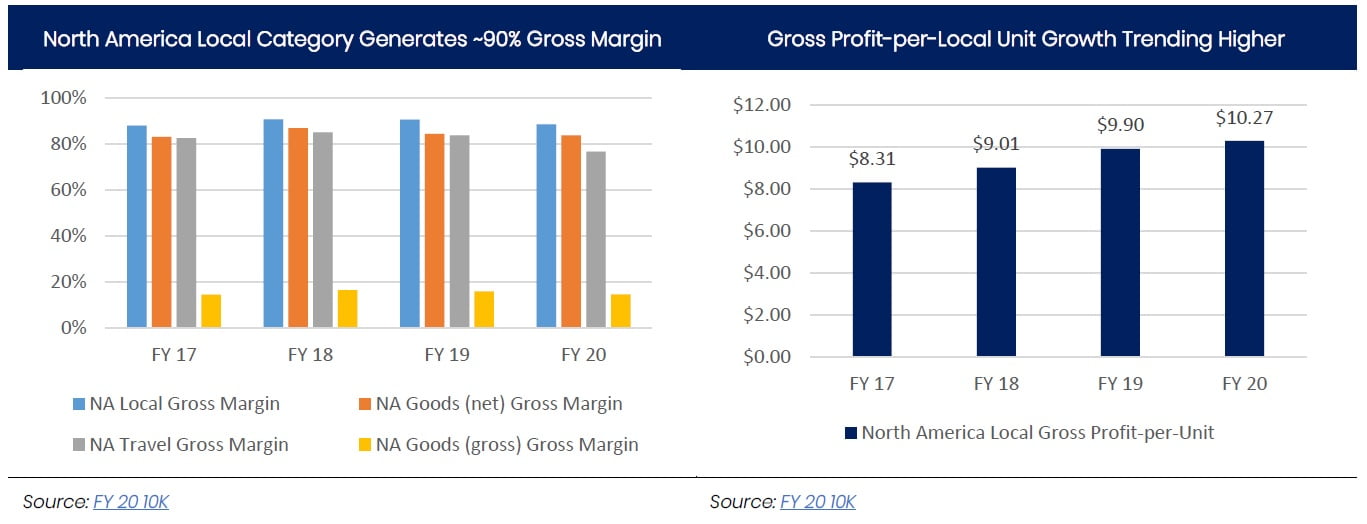

- Despite the severe headwinds created by the global pandemic, Groupon’s business has stabilized: Bears have continued to posit that Groupon is a melting ice cube, while completely ignoring recent evidence that proves otherwise. The pandemic hit Groupon with a vicious one-two punch of behavior modification and labor shortages which gutted demand and supply in key verticals. However, the worst is over for customer attrition as the North America customer base has bottomed and International customers approach trough levels. Despite widespread lockdowns and restrictions and persisting public health & safety concerns, there are ~24M customers that continue to use Groupon. ~15M of these have been customers for >3 years and are among the most active and profitable users. In addition, the largest and most profitable sub-category, Local, is already seeing sequential growth in users and accelerating purchase frequency.

- Recent, large decline in revenue is largely attributable to a change in revenue recognition accounting: Historically, the Company’s Goods business accounted for ~50% of total revenue. In early 2020, Groupon began to transition its Goods business to a third-party model. Accordingly, Goods revenue began to be recognized on a net basis (previously gross). The North America first party Goods business transition was largely completed in Q4 20, while International will be completed by the end of FY 21. At first glance it appears revenue has fallen off a cliff and will never recover. However, this is largely attributable to this revenue recognition change. Consequently, Groupon likely falls through the cracks of many financial statement screens as prospective investors inaccurately conclude that Groupon’s business is in steep decline.

- With minimal leverage and the leanest cost structure in its history, Groupon is well-positioned to take advantage of accelerating fundamentals: Groupon focused on liquidity at the expense of growth throughout the pandemic, stripping out >$200 million of fixed costs while simultaneously strengthening its balance sheet. The time for conservatism is over and we fully expect the Company to deploy significant capital over the coming quarters in the pursuit of long-term sustainable growth. • Minimal sell-side coverage and high short interest shows just how misunderstood and overlooked Groupon is: Three years ago, nine analysts joined the earnings calls, today there are two. Even with the stock near all-time lows, short interest is still relatively high in the mid-teens as bears have failed to re-evaluate their antiquated short thesis given price confirmation and negligible bullish sentiment.

- Shares are worth at least $63.18 with upside to +$98: In our sum-of-the-parts Base Case of $63.18/share, we value Groupon’s base business at 6.0x (above current levels, but well below the historical average) our FY 23 adj. EBITDA of $286.6m, or $55.35/share + the SumUp stake at $268.6 million, or $7.84/share. A more bullish case, assuming FY 23 adj. EBITDA of $340.9 million and an 8.0x multiple (in-line with historical levels) + a SumUp stake worth $483.7 million, results in a target price of $98.86.

Executive Summary

Prescience Point is long Groupon Inc (NASDAQ:GRPN). Groupon is a misunderstood Company that has been wrongly left for dead due to an antiquated bear thesis and apathetic sell-side. Market participants have completely overlooked the sizable value of Groupon’s investment in SumUp, and are significantly undervaluing the Company’s core business, whose recent turnaround has been overshadowed by pandemic related shutdowns and a quirky change in revenue recognition accounting. We believe shares will increase >3x from current price levels.

Groupon quietly owns a sizable stake in SumUp, one of the largest and fastest growing mobile payments companies in the world. In 2013, Groupon made a $13 million investment in SumUp in exchange for a 10.3% ownership interest in the company. Since making this investment, based on disclosures provided by the company, we estimate that SumUp’s revenue has grown at a CAGR of 50%+ and that FY 22 revenue will exceed $550m.

SumUp’s largest competitor in the mobile payments space – iZettle – was acquired in 2018 by PayPal for $2.2Bn or ~13x forward year revenue of $165m. Given that SumUp has more revenue, merchants and a larger addressable market than iZettle, we believe SumUp should, at the very least, be valued at a similar valuation multiple. Conservatively assuming a forward year revenue multiple of 11x, we value Groupon’s stake in SumUp at an estimated $268.6m or $7.84 per share – close to 40% of Groupon’s current enterprise value! Puzzlingly, despite the considerable size of this investment, sell-side analysts who cover Groupon have completely excluded SumUp in their valuation models, even after a recent ~$90 million book value mark-up.

In addition to ignoring Groupon’s sizable investment in SumUp, market participants are also significantly undervaluing the Company’s core business. Bears have continued to posit that Groupon is a melting ice cube, while completely ignoring recent evidence that shows otherwise. Despite operating in the most challenging environment in its history, brought on by the pandemic, Groupon’s customer base has started to stabilize and is now concentrated with its most loyal and profitable users. Notably, the largest and most profitable sub-category, Local, is already seeing sequential growth in users and accelerating purchase frequency. Additionally, Groupon focused on liquidity at the expense of growth throughout the pandemic, stripping out >$200 million of fixed costs while simultaneously strengthening its balance sheet. As a result, the Company is well-positioned to deploy capital over the coming quarters and take advantage of accelerating fundamentals.

Lastly, a recent overhang on the equity had been the lack of a permanent CEO. Groupon’s President of North America, Mr. Aaron Cooper, took the reins in March 2020 and had the interim CEO title for over a year-and-a-half until Groupon announced a permanent replacement, Mr. Kedar Deshpande, earlier this month. Despite now having a permanent CEO in place, there appears to be some reticence that Mr. Deshpande may change-up Groupon’s strategy and revert back to the Goods business given his tenure at Zappos, an online shoe and clothing retailer. At the current juncture, we think these concerns are unfounded as Groupon’s Board of Directors has been explicitly clear that its goal in the CEO search process was to bring a leader to accelerate the Company’s progress in its Local category. Nevertheless, we will be paying acute attention to any strategy shifts as we think it’s in the best interest of shareholders that Groupon continue its plan to focus on Local and transition its Goods business to a third-party model. We look forward to seeing Mr. Deshpande push forward Groupon’s Local strategy.

After stripping out the value of the SumUp investment, we calculate that the market is valuing the core business at just 2.9x consensus FY 22E EBITDA, which represents a massive 66% discount to the Company’s historical average valuation multiple of 8.7x forward year EBITDA. At this extremely cheap valuation, very little has to go right in order for Groupon shares to increase substantially from current price levels, and given the recent turnaround in the business, we believe the core business should trade at a multiple that is at least in-line with its historical averages. Assuming a conservative multiple of 6.0x FY 23 EBITDA, which still represents a significant discount to the Company’s historical average of 8.7x, we estimate that the core business is worth $55.35 per share.

Putting it all together, we believe Groupon shares are worth $63.18 in our Base Case and $98.86 in our Bull Case.

Read the full report here by Prescience Point

Updated on

Sign up for ValueWalk’s free newsletter here.

{kind=link}