"Double, double toil and trouble; Fire burn, and caldron bubble." – Witches in Macbeth

"Cool it with a baboon’s blood – then the charm is firm and good" is the conclusion of that line. Certainly our Government witches have gotten us our double off the S&P’s Satanic drop to 666 back in March of 2009 to a high of 1,322 yesterday – just 10 points away from a 100% run.

Back in March of ’09, I was considered a perma-bull as I was running very contrary to the prevailing opinion on Wall Street. Jim Cramer was warning that the Dow could fall to 5,320 – 20% lower than it was at the time and, on Fast Money on March 6th of 2009 (the day before the bottom):

- Guy Adami said: "But I still don’t think we’re there, yet. It has to feel like the end of the world before the market can bottom."

- "The data that I’d watch to signal a bottom is the rate of decline slowing", adds Karen Finerman. "But I don’t see that, yet."

- "We won’t be at the bottom until the financials participate in the market’s broader moves," adds Pete Najarian.

- "I don’t think we’ll get a bottom until we get policy going forward that doesn’t seem like it’s just attacking Wall Street," adds Jon Najarian.

I’m not bringing this up to pick on those guys but just to remind you that "everybody" can be very, very wrong – both at the top and the bottom of the market. My 13 buy picks on LiveStock that day seem like no-brainers now: Shorting SKF (2 ways), long FAS (2 ways) and longs on RUT, GE, BAC, DIS, XLF, AMZN, TGT, HOV and RKH.

This last week, perhaps ahead of the curve, we shorted oil with USO and XLE, the Russell with TZA and emerging markets with EDZ. We did this in preparation for some buying though because, if we break over our levels (and we did) and hold them (and we are) – then it’s time to get a little more aggressively bullish. It’s a simple enough matter – If you have a virtual portfolio that was 25% invested and 15% bearish and 10% bullish then we deploy 10% of the cash into bullish plays and we are then 35% invested and 20% bullish and 15% bearish. There’s 6 months of virtual portfolio management training in 10 seconds!

Getting more bullish means we’re going to be a lot more selective in our bearish hedges. We’re not going to want too many broad index shorts (although we feel the small caps, obviously, may have trouble due to inflation pressures) and we will focus on high-flyers like CMG, OPEN and NFLX – who are primed for spectacular falls if sanity returns to the markets, rather than just shorting the Dow or the S&P or the Nasdaq – which seem to be more firmly on an upward trajectory.

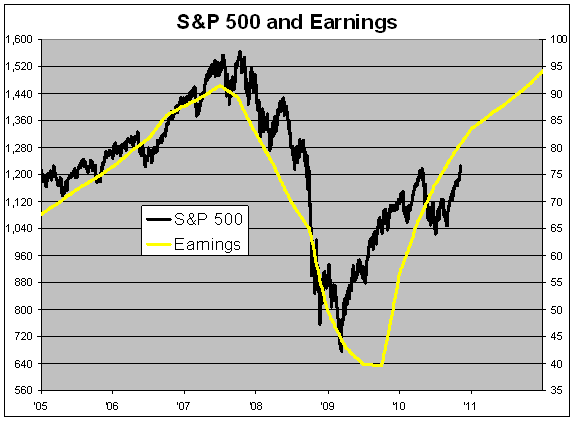

Have Bernanke and company cooled the rally "with baboon’s blood" to make the charm "firm and good" or – is this spell more like an illusion – one that the markets will suddenly wake up from? So far, Q4 earnings are looking good with 71% of the reporting S&P companies reporting better than expected earnings and forecasts for 2011 are looking for an all-time high of $1,017.44 a share. That is very impressive. Last time S&P earnings were near $1,000, the S&P was at 1,550 – no wonder SSO was one of our 500% plays!

Still, let’s keep in mind that that valuation (in 2007) was based not just on current earnings but on the expectations, at the time, that earnings would grow to $1,150 in 2008 and $1,300 in 2009. What actually happened is (and it’s a funny story, really) – it turns out that the earnings that were claimed by many banks and mortgage companies were FICTITIOUS – who would have thought, right?

And, when the bank makes up numbers and the analysts believe them – especially when they believe they can be extrapolated out forever, then valuations can quickly get out of control because, as you can see from this chart, one bad year can wipe out several good ones and it’s the risk of that potential bad year that is currently not priced into some of these runaway valuations.

As we saw in 2007 – the banks claim their loans are good and real estate values are solid and that causes mortgage companies to raise their forecasts (maybe in good faith), which causes builders to raise forecasts and then the land and lumber guys raise forecasts and then Sears raises guidance and they all staff up for a Christmas that never comes – a massive misallocation of resources, all based on one faulty premise whether or not the intent was there to deceive the investing public or just to take huge bonuses before they got caught.

Now, perhaps, we have a different sort of deception as the Federal Reserve pumps money into the system in the vague hope that jobs will magically trickle down as Trillions of dollars handed out to the IBanks HAVE TO create jobs for our 16M unemployed – don’t they?

They’d better – because we bet our future on it! In fact, with $15Tn in official debt by the end of this year and a $1.5Tn annual deficit – we’ve also bet our Children’s futures on it as well as possibly our Granchildren’s futures.

All this gambling, just to get Grandpa a job!

Well, this isn’t all about getting ourselves jobs. If that was a real priority then there are better ways the Fed could have spent $3Tn over 2 years and better things the government could have done with another $700Bn in Tarp money plus all those other bailouts and, of course, the Obama tax cuts – another $4Tn at least all spent to employ what so far? About 1,000,000 net people? That’s about $7M per job created so far – surely there must be more efficient ways to spend the people’s money?

Even if we don’t give a damn about the unemployed American worker as we step over them on our way to the Apple store (made in China), ultimately, we do need people to work, whether here or in China, for all those speculative commodity bets to pay off. Oil, for example, was and is a short for us as supplies in Cushing, Oklahoma (the main delivery point for imports) are at their highest level since 2004 while gasoline inventories are at 21-year highs as well.

Investors should consider selling bullish positions because the market may be set for a “notable correction” as the Egyptian crisis subsides, according to JPMorgan Chase & Co. Thanks for the heads up JP – but we’re good already! “This week will be characterized by a drift down in crude prices on days where either no new tensions arise or where political progress is perceived,” JPMorgan analysts led by New York-based Lawrence Eagles said in a report dated yesterday. “Investors should therefore consider taking profits on all or a portion of their remaining long positions.”

Are commodities the new housing bubble – based on speculative dreams that will never come to pass? Are the investment banks, even now, booking massive profits and causing analysts to push sectors that will lead to the next set of malinvestments that will turn sour, crash the markets and throw another few million people out of work? Money is flowing into commodities as fast as it is flowing out of the Shanghai composite – with the CRB up 17% last year and the Shanghai down 14%.

This, of course, makes little sense since the infinite China growth story is the engine that’s driving the commodity markets but let’s not let a little thing like reality get in the way of a good story, right? “Prices of commodities will have to go up to rationalize the investments to produce commodities as well as consumption,” said Morgan Stanley’s Jeremy Friesen. “Corporates are going to have to deal with how to be profitable and yet still facing higher costs.”

China raised their benchmark rates another quarter point today to keep a lid on rising commodity prices but that only serves to devalue the dollar further and push commodity prices even higher – fueling the speculative frenzy for another day at least. Round and round the madness goes – where it stops – we’ll find out soon enough…

Be careful out there!