{kind=link}

Whatever the jobs number, G20 lies ahead.

Whatever the jobs number, G20 lies ahead.

As you can see from the chart on the right, the macro data for August has taken a very sharp downturn so it seems unlikely that we'll be matching last month's level of 255,000 jobs created and, in fact, 180,000 is the whisper number and that would be nice, if the US population wasn't growing by 220,000 per month. Adding anything less than 220,000 jobs is falling behind in total employment.

That's why we don't care much about the headline number – which is estimated out of 165M jobs so 50,000 jobs up or down is a 0.03% tracking error which is why it's idiotic to see these figures taken so seriously every month. No one in the MSM ever tells you these things because you tune in or click on the Non-Farm Payroll Report and hundreds of highly-paid pundits make a living discussing the NFP so none of them are going to turn around and tell you what complete and utter BS the number is, are they?

So we're expecting a miss this morning, even from the lower expectations and we only need one chart (above) to make that prediction and I will be on TV Tuesday morning to discuss it and they won't let me decry the whole thing as a farce – not if I want to be invited back!

Our working theory was to hold Gasoline Futures (/RB) longs overnight in expectations of a weak jobs report weakening the Dollar and popping /RB back over the $1.30 line after yesterday's 4.5% sell-off. We're hoping for $1.32 or better as we're coming into the holiday weekend but anything over $1.30 is a keep – so tight stops over the line.

By the way, those USO Sept $11.50 puts we told you about finished the day at $1.49, up 186% for the week and we're done with those, obviously, as we flipped long into the weekend, as planned. Rembmer, we can only tell you what the market is going to do and how to make money trading it – the rest is up to you!

Bearing in mind this is all BS data, how will the beautiful sheeple react to weak jobs numbers? Well, at first they will rally the market because the Fed hangs its hat on employment numbers so low employment numbers push back the tightening (the one that never comes) and we all love FREE MONEY, don't we? As I mentioned, less jobs means less Dollars to pay employees so that weakens the need for Dollars and the Dollar is already down half a point – helping to lift the indexes and commodities.

However, the number we do care about is Hourly Earnings because giving 165M people a 2% raise is like hiring 3.3M people, which dwarves the number of jobs added (or is it "little people"?). Unfortunately for the little people, who are hi-ho'ing off to work, hourly earnings are only up 0.1% in August, just 1/3 of July's encouraging pace and, therefore, discouraging.

Here's another chance for an Econ 101 lesson: Most companies sell products to Consumers. Most consumers get money by working. The amount of money they get from working is the amount of money they are able to spend buying things from those companies (though there is debt, and we'll discuss that later). So, if the Consumers have more money, the economy can grow but, if they have less money – it tends to stagnate.

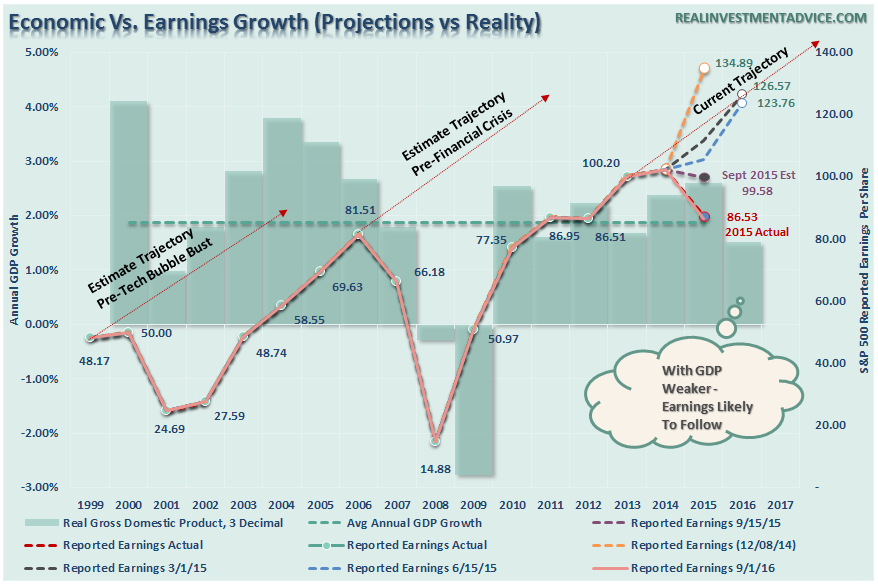

This is not complicated stuff but you'd think so to hear the roundabout discussions they have on TV about something so simple. Unfortunately, the amount of disposable income available to consumers has been falling off a cliff and they have, so far, been piling on debt to cover the shortfall but, as you can see from the chart above, that is what they tend to do right before a crash.

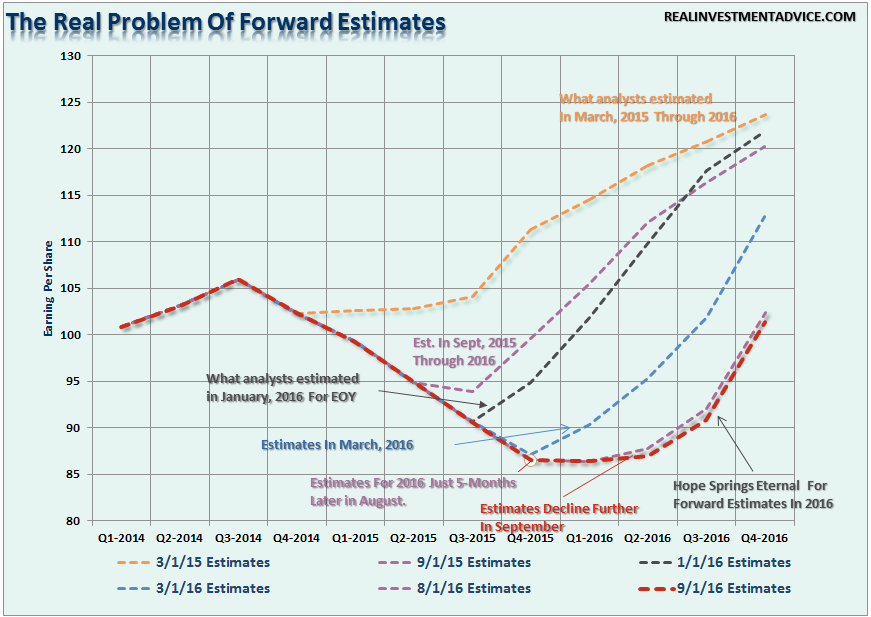

That's why Corporate Earnings are still bottoming and, as we discussed yesterday, only their optimistic projections are signaling a turnaround when, in fact, those optimistic projections haven't hit their marks since the end of 2014:

The willingness of US Corporations to fudge their projections is one of the reasons the Leading Economorons are so far off in their own growth estimates but, of course, it's their own fault for taking CEO's word for it in the first place. A healthy dose of skepticism is the key to being a good value investor!

So bad news is good news – for now. We have the G20 meeting in China this weekend and the bulls expect MORE FREE MONEY in the form of Trillions in stimulus plans and indications of even more monetary easing and we are still expecting them to be disappointed and have hedged ourselves (also outlined in yesterday's busy post) accordingly but we have not cashed out our long-term positions, which we reviewed yesterday in our Live Member Chat Room, because they made $70,655 since July 4th and we'd hate to miss the next $70,000 in case we're wrong and the rally continues.

Intraday, we'll be looking to short at Dow (/YM) 18,450, S&P (/ES) 2,175, Nasdaq (/NQ) 4,800, Russell (/TF) 1,245 and Nikkei (/NKD) 17,000 and, as usual, we wait for 3 of 5 to cross under then short one of the other two, keep very tight stops until the 5th confirms by failing the line and then stop out if ANY go back over and, otherwise, enjoy the ride down with sensible stops.

The Russell has fallen from 1,245 to 1,230 twice this week for $1,500 profits but, of course, a bull would say it's gone up from 1,230 to 1,245 twice as well – that's what makes a market! You just have to play the side of the channel you are more comfortable with and, at the moment, I feel better about being a bear.

The Russell has fallen from 1,245 to 1,230 twice this week for $1,500 profits but, of course, a bull would say it's gone up from 1,230 to 1,245 twice as well – that's what makes a market! You just have to play the side of the channel you are more comfortable with and, at the moment, I feel better about being a bear.

Have a great weekend,

– Phil