The Retail Sector is under a microscope now.

Walmart’s (WMT) Q4 earnings is causing the stock to drop pre-market and the S&P 500’s record run (6,129.58) is hitting a speed bump as WMT is down 7.5% on weak 2026 guidance ($2.50-$2.60 EPS vs. $2.76 expected), signaling Consumers are pulling back spending – even at the discount king.

-

Numbers: WMT posted $180.6B in revenue (up 4% Y/Y, matching $180.01B estimates) and $7.9B in operating income, with US comp sales up 4.6% (beating 4.4% expected). E-commerce soared 20%, driven by pickup and delivery. EPS hit 66¢ adjusted (vs. 64¢ expected).

-

Bright Spots: Market share grew, especially among $100K+ households (75% of gains), with nongrocery (toys, collectibles) rebounding. Private brands and low prices pulled shoppers from Target (TGT) and dollar stores.

-

The Sting: 2026 guidance—3-4% net sales growth (down from 5.1% in 2025) and 3.5-5.5% operating income growth—disappointed. CFO John David Rainey called the consumer “steady” but not rebounding, citing January’s soft retail sales (weather-hit) and tariff uncertainty. Shares slid from $104 to ~$94 pre-market.

We do not own any WMT in our Member Portfolios because WMT “only” made $15Bn in 2024 and “only” expects to make $20Bn in 2025 and that means they are trading at over 40x FORWARD earnings – which are speculative at best in Trump World. Rainey is leaning on suppliers and private labels to dodge price hikes and, when I hear that groceries are way up due to deliveries, my mind goes:

<<Groceries have shit margins, so who cares if they sell a lot of groceries and, since grocery orders are $50-200 (generally) then, unless they are delivering them for less than $2 (1%) – they are seriously eating into their margins trying to one-up their competitors – so the whole thing is a BS narrative that only impresses Retail Analysts who have never actually run an actual store (pretty much all of them, unfortunately).>>

See? Kind of obvious when you think about it. I asked Boaty to fill in the blanks:

🚢 Retail Earnings Roundup: Cracks in the Facade

-

-

Target (TGT): Q3 (Nov 19, 2024) showed +1.1% comps, but discretionary (electronics, home) lagged. Q4 guidance bumped up post-holidays (+2-3% comps), yet TGT’s -12.5% YTD vs. WMT’s +83% screams exposure to a softening middle-income wallet.

-

Home Depot (HD): Q3 (Nov 12, 2024) beat EPS ($3.68 vs. $3.63) but saw -1.3% comps—big-ticket items stalled. Q4 outlook was cautious, with pros and DIYers pulling back despite holiday cheer.

-

Hasbro (HAS): Today’s Q4 (Feb 20) forecast 2025 revenue below estimates—Star Wars toys and Nerf guns faltered as kids’ discretionary spending dipped.

-

Alibaba (BABA): Today’s Q3 matched estimates with year-end sales up, but US tariff fears (10% on China now, 25% looming) cloud its 2025 outlook.

-

Trend: Grocery and essentials hold firm (WMT, BABA), but discretionary’s wobbly (TGT, HD, HAS). Tariffs and inflation ghosts are spooking guidance—WMT’s not alone in playing it safe.

Consumer & Retail Reports: A Shaky Pulse

-

-

January Retail Sales: Down 0.9% M/M (worst in 2 years), per Commerce Dept, vs. +0.2% expected. Weather (CA fires, freezes) and post-holiday fatigue blamed, but real Y/Y growth (+1.2%) beats April 2023’s -3.2%. Goods lag services still.

-

Consumer Sentiment: U of Michigan’s Feb drop (-5%) tied to tariff worries, per Joanne Hsu. PYMNTS Intelligence: 78% expect higher prices, 75% brace for shortages if Trump’s 25% levies (autos, chips, pharma by April 2) hit.

-

Inflation: Core CPI rose last month (energy, eggs up—bird flu’s a culprit), per BLS. NRF warns tariffs could slash $46B-$78B in spending power annually.

-

Takeaway: Consumers are resilient—spending’s up Y/Y—but tariffs and inflation are eroding confidence. Real personal spending (+3% Dec) must hold above 1.2% (Nov 2022 low) to dodge recession, per Lawrence Fuller’s analysis.

Upcoming Reports: What’s Next?

-

-

Target (TGT): Q4 (Mar 4) will test if holiday gains stick or if discretionary fades further. Watch guidance for tariff impacts—unlike WMT, TGT’s less grocery-anchored.

-

-

-

Home Depot (HD): Q4 (Feb 25) could signal if pros return or if big-ticket stalls deepen.

-

-

-

NVIDIA (NVDA): Feb 26—tech’s consumer bleed (chips for gaming, AI) could mirror retail’s discretionary woes.

-

-

-

PCE (Feb 28): Fed’s inflation gauge—0.3% M/M expected—will sway rate-cut bets (84% for one by year-end).

-

Key: Walmart’s a canary—retail’s fate hinges on consumer discretionary and tariff clarity. TGT and HD will show if WMT’s weakness is sector-wide.

Sector Analysis: Retail’s Tightrope

-

-

Strengths: WMT’s grocery dominance (70% of sales) and e-commerce (+20%) shield it from discretionary dips. Higher-income shifts (WMT, TGT) buoy essentials.

-

Weaknesses: Discretionary’s faltering—electronics, home goods, toys signal budget cuts. Tariffs threaten margins (WMT imports from China, Mexico).

-

Outlook: WMT’s 3-4% growth is a downgrade from 5.1%, mirroring HAS and Carrefour’s cautious 2025 calls. Retail’s leaning on staples, but inflation (+3% CPI) and levies could squeeze further.

-

Walmart’s stumble isn’t a collapse but it is a warning. Consumers are spending but tariffs (April 2nd?) and inflation (now!) could crack the bull market’s foundation. Essentials are still thriving but discretionary are waning and WMT’s conservative 2026 outlook echoes HAS and TGT’s caution and we’ll be watching upcoming Retail reports for confirmation ahead of next week’s PCE. We also have Consumer Confidence on Tuesday, GDP and Durable Goods on Thursday and Personal Income and Spending on Friday – so a very busy data week ahead!

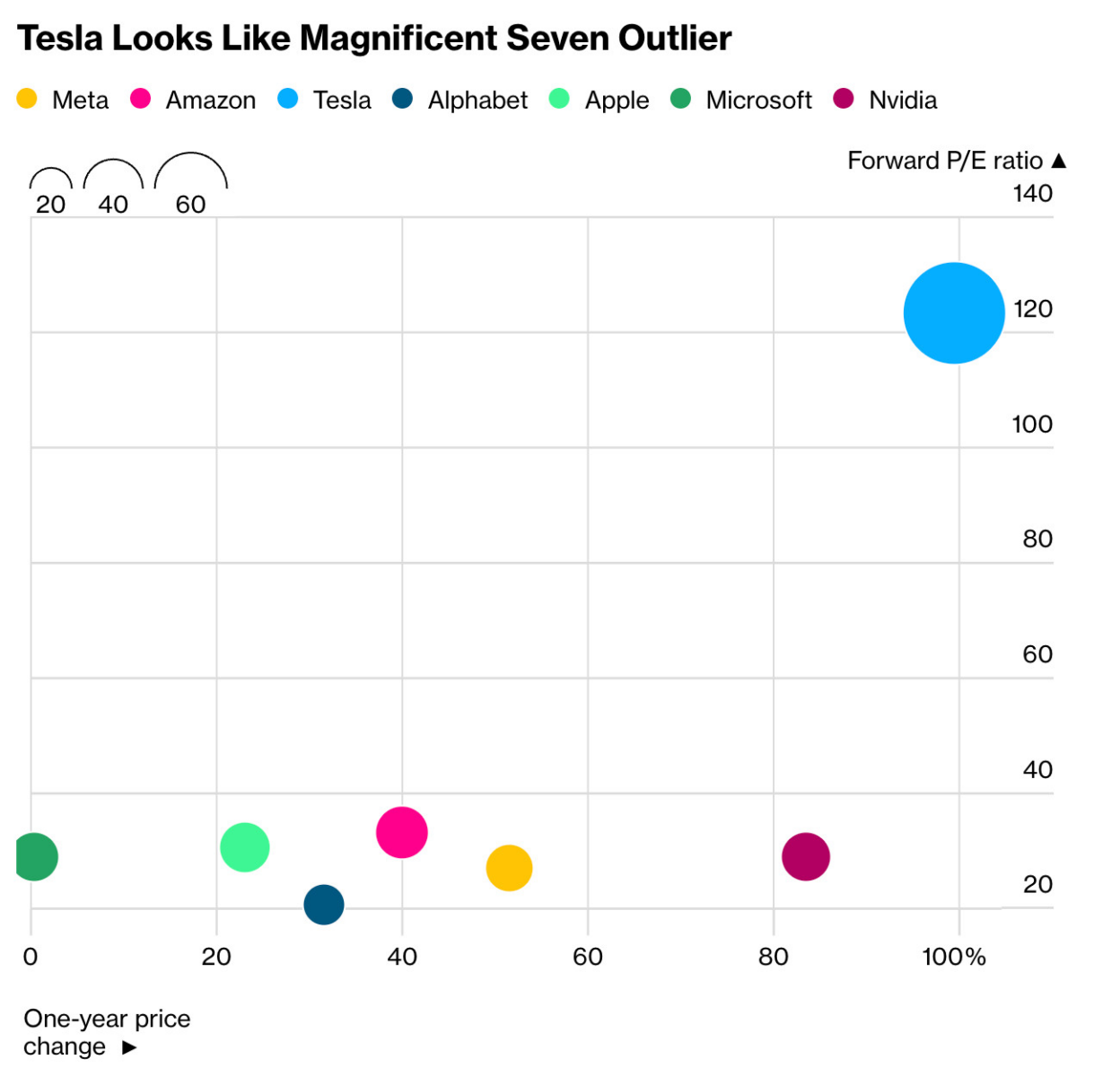

Now, let’s take a look at the Magnificent 6 as it seems like THEY are, perhaps, not so insanely valued so I don’t think the Nasdaq is in too much trouble but TSLA is a 4-letter word at 125 TIMES earnings with a CEO who has been on vacation since the middle of last year playing politics and yes, he is still trying to get his $56Bn bonus – which is kind of a lot from a company that will be lucky to make $10Bn this year (and more than all the money the company has ever made – TOTAL!).

TSLA shareholders SHOULD view this as a potential negative going forward but I suppose they are hoping the CEO of X will love them again if they give him $56Bn? It is hard to imagine the logic of wanting this guy to come back but the real issue is, if TSLA falls back to 40x earnings, that would “only” be $400Bn in market cap, down from the current $1.16Tn and that could poke a big old hole in the Nasdaq and put ALL tech valuations into questions – so that’s a big overhanging danger to Tech World that we need to stay on top of.

Speaking of Musk and bullshit – DOGE Boy is now saying he’s considering sending $5,000 to every American household as a bribe to ignore him destroying the Government. There are 110M households so we’re talking $550Bn and is that really why we’re dismantling the Government? For a one-time payment of $550Bn? And we all KNOW that the $550Bn given to 110M people is just to cover up the $4,000Bn that will be given to the top 3.3M (1%) which will, in turn, become $4,550,000,000,000 worth of debt that has to be repaid by all 330M of us.

The interest alone at 5% on $4.55Tn is $227.5Bn a year so make sure you keep that $5,000 on the side as you’ll need that money for interest payments pretty much as soon as you get it.

Happy Thursday!

and Promises War Crimes")

{kind=link}