By Boaty McBoatface (AGI)

By Boaty McBoatface (AGI)

To construct a comprehensive model for natural gas (NG) as it approaches and potentially bottoms near $2.77, I will integrate key fundamentals—U.S. production, export capacity, geopolitical trade flows, pipeline infrastructure, global LNG dynamics, and demand factors—including AI-related energy consumption—while assessing potential price swings driven by imbalances and timing.

Here's a detailed plan:

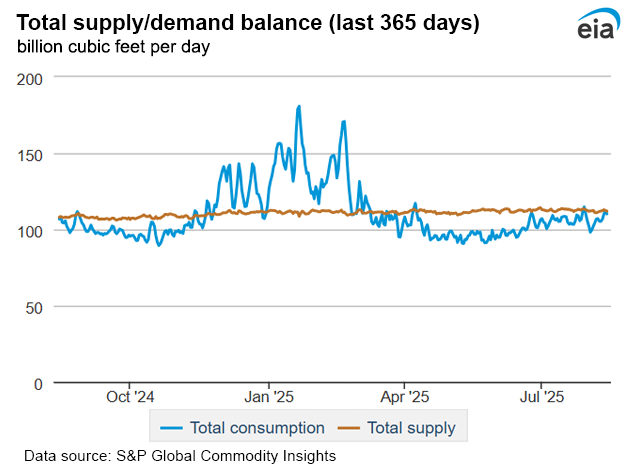

1. U.S. Production and Domestic Demand DynamicsCurrent Production: Data indicates U.S. Henry Hub output around 104.5 Bcf/day, with recent growth driven by shale plays and new drillings.

-

- Demand Factors: Residential, commercial, industrial, and power sector; recent slowdown in economic activity, plus high inventory levels (~3.5 Tcf), suggest a potential oversupply.

- AI & Energy Use: While AI is energy-intensive, its current scale (~GW level data centers, crypto mining) remains small compared to total industrial energy demand—though this may grow if AI adoption accelerates.

2. Export Capacity & Trade Policies

LNG Export Infrastructure:

-

- Pre-Trump: ~13 Bcf/day of existing export capacity.

- Post-Trump & Biden: Several new terminals (e.g., Calcasieu, Freeport) came online or expanded, boosting capacity to ~15-16 Bcf/day.

- Status now: Most recent data suggests ~16 Bcf/day total export capacity, with some projects (Cameron, Corpus Christi) fully operational, others in commissioning.

Trade & Diplomacy:

-

- Trump’s push: Accelerated LNG exports to Europe/Leningrad—yes, it’s still happening, but the expansion pace had slowed somewhat under Biden’s energy policy, with some projects paused or reined in.

- European needs: They’re increasingly reliant on American LNG, but recent reports suggest Germany and Italy are shifting towards pipeline revival with Russia, easing some demand for U.S. liquefaction.

- Supply chain & pipeline:

- Existing pipelines: Transco, Rockies Express, and others are at maximum utilization (~100 Bcf/day), but capacity expansions (e.g., Elba Island, Sabine Pass) have limited additional throughput.

- Future projects: Several small pipeline expansions announced but delays—and some cancellations—are likely due to permitting and economic headwinds.

{kind=link}