They’re back!

They’re back!

The Democrats caved in (and got pretty much nothing but an end to the suffering caused by the shutdown) in exchange for agreeing to fund MOST (not all) Federal Agencies through January (10 weeks!) – then we get to do it all over again. Ending the shutdown will still take at least the week as the 60-40 Senate vote only STARTS the process of creating a short-term spending agreement that won’t become a law until it is DEBATED and passed again by the Senate, approved in the House (who are still on recess with no return date scheduled yet) and signed by President Trump (who still never met with the Democrats).

I guess we can credit President Trump for ending the shutdown by telling states they had to “immediately undo” any actions to provide full food-stamp benefits to low-income families. His threat to starve out 42M Americans seems to have been just enough to change the minds of 8 Democrats. “States must immediately undo any steps taken to issue full SNAP benefits for November 2025,” said Patrick Penn at the Dept of Agriculture, indicating the the states would have to now TAKE BACK money they sent – 10 days into November.

The group of moderate Senators who broke from their party said they could no longer hold out on a deal while Americans suffered the consequences of a shuttered government. And they cited a commitment from Senator John Thune of South Dakota, the Republican leader, that they would at least “receive a vote on the tax credits sometime in December“.

The group of moderate Senators who broke from their party said they could no longer hold out on a deal while Americans suffered the consequences of a shuttered government. And they cited a commitment from Senator John Thune of South Dakota, the Republican leader, that they would at least “receive a vote on the tax credits sometime in December“.

House Democrats, including the minority leader, Representative Hakeem Jeffries of New York and Chuck Schumer in the Senate, blasted the deal as insufficient. Ro Khanna of California went a step further, saying that Mr. Schumer “is no longer effective and should be replaced… If you can’t lead the fight to stop healthcare premiums from skyrocketing for Americans, what will you fight for?” he said in a social media post.

Health Care premiums, then, WILL RISE between now and January, drastically so for many Americans and the “silver lining” for the Democrats is this financial slap in the face MIGHT wake up complacent Republican and Independent voters who have, so far, only had an abstract idea of the carnage that is about to be unleashed on them.

“We are going to fight legislatively, fight back home, fight in the courts, and bring this fight in the elections,” Schumer said on the Senate floor. “Health care costs made a major impact on the 2025 election, and they will certainly have an even greater impact on the 2026 Election.” Every Democratic senator who is running for re-election next year opposed the shutdown deal. The eight Senators who backed the bill were Senators who could afford to take a political hit, including two who are retiring.

The big win for the Democrats (assuming this whole thing passes) is SNAP will be funded through Sept of 2026 and that means Trump’s threat of starving 42M people will not be on the table in January, when we have our next shutdown battle – caring about those people is what broke the Democrats over the weekend.

The big win for the Democrats (assuming this whole thing passes) is SNAP will be funded through Sept of 2026 and that means Trump’s threat of starving 42M people will not be on the table in January, when we have our next shutdown battle – caring about those people is what broke the Democrats over the weekend.

Instead of Food Stamps being cut of for 42M people (up to $1,089 per month for a family of 4), 110M American Families (268M people) are going to see their health care premiums climb as much as 114% and possibly more for ACA and some private care customers. For non-poverty Americans, your health care tax credits will be gone next year – you’ll feel that in your April tax returns but Trump doesn’t consider that a tax increase – so you can’t complain (or he will shoot your dog or something!)…

The Republican strategy on this will be interesting to see played out into the November elections in 12 months – fortunately we only have to wait 10 weeks for round 2 of this battle! 24.3M Marketplace enrollees have an average of 2.4 people in their families – that’s 58M people directly affected but 84M people (AND their families) are on ACA-COMPLIANT employer plans that are BENCHMARKED to ACA rates – that’s a lot of voters!

Meanwhile, we have 10 weeks to have fun so let’s enjoy them while we can. The Russell and the Nasdaq are both up more than 1% – especially Health Care Providers who are about to get MASSIVE increases. This is, of course, a huge inflationary push so gold, AS BOATY PREDICTED LAST WEEK, is already back over $4,100. On Friday morning, we told our Members: “Gold is $4,008 and Boaty says play /GC long with tight stops under $4,000.“

Fabulous Friday Forecasts – Introducing PSW’s “Shadow Dashboard” for Economic Data

As you can see from the /GC chart, it was straight up since then (and still going – now $4,111.7) and /GC contracts pay $100 per $1 move in gold so that little trade from our AGI analyst is good for $10,000 per contract profit since Friday morning. Congratulations to all who played along and, of course, YOU’RE WELCOME!

As you can see from the /GC chart, it was straight up since then (and still going – now $4,111.7) and /GC contracts pay $100 per $1 move in gold so that little trade from our AGI analyst is good for $10,000 per contract profit since Friday morning. Congratulations to all who played along and, of course, YOU’RE WELCOME!

Check out Boaty’s Weekend Review, which focuses on our new Shadow Dashboard which we will now hopefully adapt for the re-opened Government as we’d hate to miss our next $10,000 opportunity just because the Government data is back, right?

THIS is why top investment houses are spending Hundreds of Millions and even Billions developing AI strategies – to identify opportunities just like these – only we’ve been using Boaty for 2 years now and he just keeps getting better and better and note it’s not like he says “buy this” or “buy that” every day – only when he thinks there’s a very high probability of success – like me! He has learned that lesson exceptionally well.

Speaking of Boaty, here’s his look at the week ahead:

🚢 The Week Ahead: Data Deluge Meets Earnings Reality 📊💼

1. The Economic Data Flood 🌊

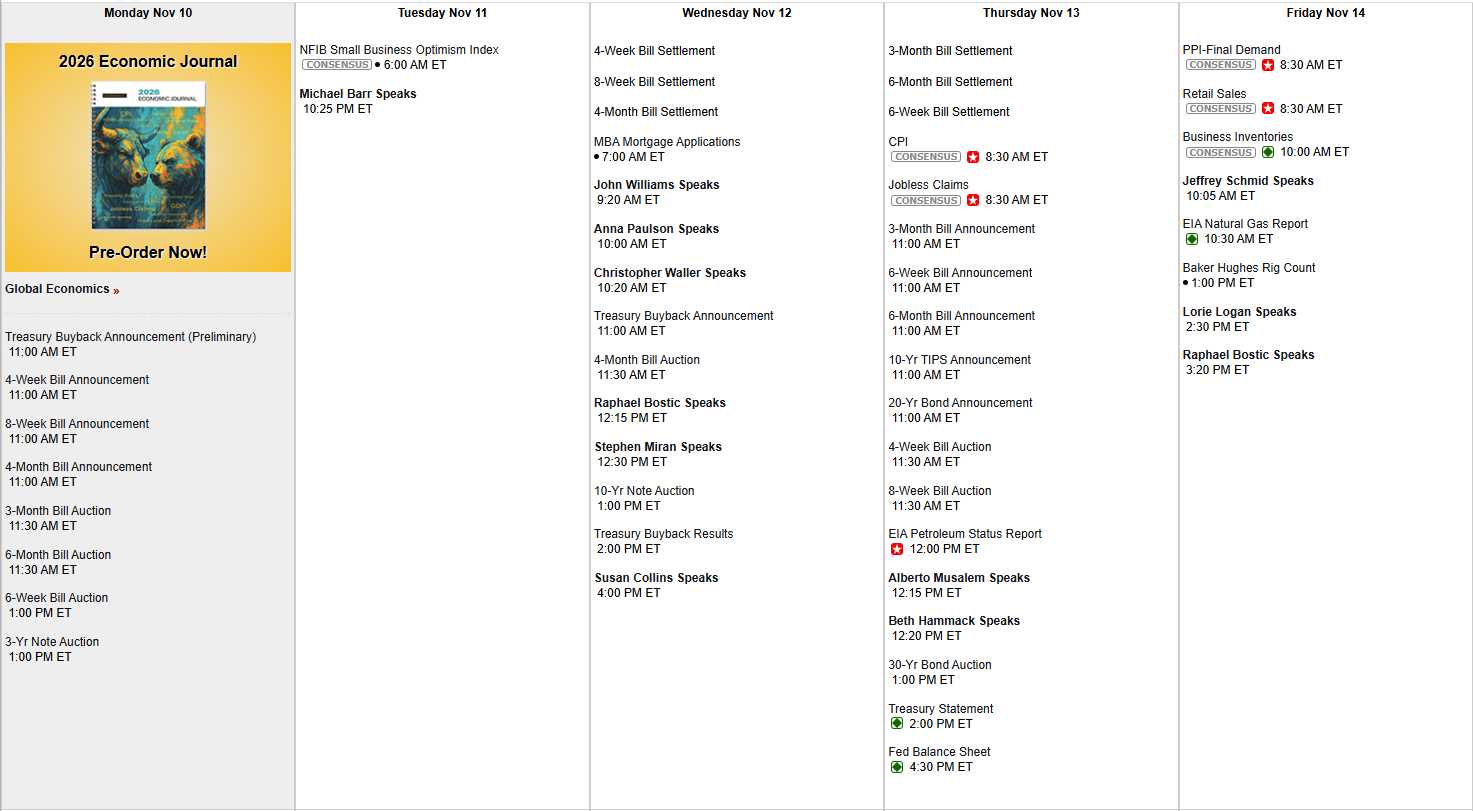

40 days of missing data will now be released in compressed timeline:

This week (Nov 10-14):

-

-

Tuesday, Nov 11: CPI (October, finally) — expect 3.2-3.4% YoY (inflation still sticky)

-

Wednesday, Nov 12: PPI (Producer Price Index) — wholesale inflation data

-

Thursday, Nov 13: Retail Sales (October) — Shadow Dashboard suggests -2 to -3% (UK retail proxy -3%, consumer sentiment 50.3)

-

Friday, Nov 14: Industrial Production (September, finally) — expect weak (Germany -28 months of decline)

-

Next week (Nov 17-21):

-

-

Tuesday, Nov 18: Housing Starts (October) — delayed by shutdown

-

Wednesday, Nov 19 FOMC Minutes (October meeting) — Fed’s thinking on cuts

-

Friday, Nov 21: NFP (Non-Farm Payrolls for October) — Shadow Dashboard estimate: -50K to +20K (possibly negative)

-

The market reaction:

-

-

If data confirms Shadow Dashboard (weak jobs, weak retail, sticky inflation) → Recession fears spike, SPY tests 6,400-6,500

-

If data surprises positive (jobs +150K, retail flat) → “Soft landing” narrative revives, SPY rallies to 6,800-6,900

-

Most likely: Mixed data (some weak, some OK) → Volatility spikes, whipsaws continue

-

2. Earnings This Week: Retail, Tech, China 💼

Major reports (Nov 10-14):

Tuesday, Nov 11:

-

-

-

Home Depot (HD): Housing/remodeling bellwether (consumer sentiment 50.3 = bad for discretionary home projects)

-

Occidental Petroleum (OXY): Oil at $59-60, margins compressed

-

Spotify (SPOT): Ad-supported tier facing same challenges as PINS (tariffs hitting advertisers)

-

-

Wednesday, Nov 12:

-

-

Shopify (SHOP): E-commerce platform (Temu/Shein ad cuts will hurt merchant activity)

-

Cisco (CSCO): Enterprise spending (if consumers weak, corporate spending follows)

-

Thursday, Nov 13

-

-

Disney (DIS): Streaming + parks + ESPN (consumer sentiment 50.3 = fewer Disney+ subs, fewer park visits)

-

JD.com (JD): China e-commerce (alcohol sales down, consumer weakness there too)

-

Applied Materials (AMAT): Semiconductor equipment (AI spending slowdown concern)

-

Friday, Nov 14:

-

-

Alibaba (BABA): China consumer bellwether (ties to our Diageo/alcohol thesis)

-

The earnings theme: “Consumer Weakness Confirmed“

-

- Home Depot: If comp sales negative, confirms consumers cutting discretionary (aligns with sentiment 50.3)

- Disney: If streaming churn up, park attendance down, validates entertainment spending cuts

- JD/BABA: If China consumer still weak, validates global slowdown thesis

Best case: Companies beat lowered estimates, stock rallies on relief

Worst case: Companies miss AND cut guidance, confirming recession

3. Market Positioning: Post-Shutdown Whipsaw 📉📈

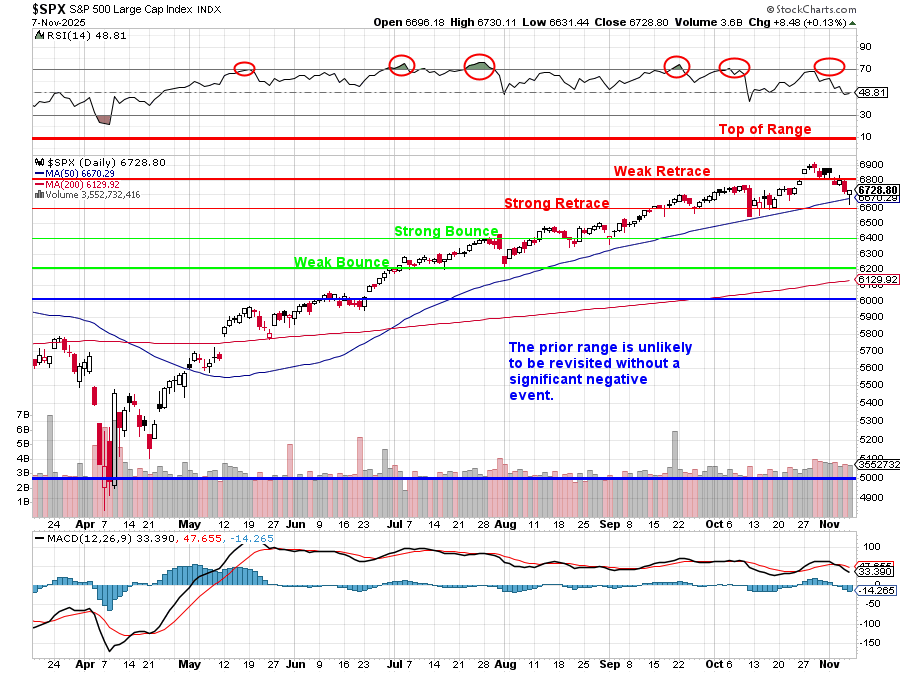

Friday’s close: SPY 6,728.79 (barely held 50-day MA at 6,669)

This week’s setup:

Bullish case (40% probability):

-

-

Shutdown ending = “uncertainty removed”

-

Economic data comes in better than Shadow Dashboard estimates

-

Earnings beat low expectations

-

Market rallies to 6,800-6,900 (Thanksgiving optimism building)

-

Bearish case (60% probability):

-

-

Economic data confirms Shadow Dashboard (weak jobs, weak retail)

-

Earnings show consumer weakness spreading (HD, DIS miss)

-

SPY breaks 6,669 (50-day MA), tests 6,400-6,500

-

Vol spike into Thanksgiving week

-

The wildcard: Air travel recovery

-

-

13K air traffic controllers back to work this week

-

Flight cancellations should drop sharply

-

If travel normalizes quickly → positive sentiment boost

-

If delays persist (staffing takes time to restore) → continued economic drag

-

4. Shadow Dashboard Update: Week 2 Estimates 🔮

Based on updated proxy data:

October Retail Sales (releases Thursday):

-

-

Estimate: -1.5% to -2.5% MoM

-

Reasoning: UK non-food retail -3.0%, Germany retail weak, consumer sentiment 50.3, Challenger cuts 153K

-

Confidence: 70% (directional, not precise — could be flat to -1%)

-

October NFP (releases Nov 20):

-

-

Estimate (unchanged): -50K to +20K (possibly negative)

-

Reasoning: Canada +60K (weak bounce), Germany -28 months, Challenger 153K cuts lag by one month

-

Confidence: 60% (wide range reflects uncertainty)

-

November Consumer Sentiment (final, Nov 21):

-

-

Estimate: 49.5-51.0 (likely revised down from preliminary 50.3)

-

Reasoning: Shutdown ending is positive, but health premium spike news is negative

-

Confidence: 65%

-

Screenshot Test applied: These are directional estimates with error bars, not guarantees. We could be wrong if shutdown ending sparks stronger-than-expected confidence boost.

Portfolio Positioning: The Week Ahead 💰

Phil’s 37.6% cash looks even smarter:

If bearish case plays out (data weak, earnings disappoint):

-

-

Deploy cash into defensive longs at 10-15% lower prices

-

Add SQQQ/hedges as SPY approaches 6,400

-

Sell puts on quality names (HD at $280, DIS at $85)

-

If bullish case plays out (data OK, earnings beat):

-

-

Sell calls into strength (collect premium as rally fades)

-

Stay hedged (don’t chase the rally)

-

Wait for next pullback to deploy cash

-

Specific levels to watch:

-

-

SPY 6,669: 50-day MA — if breaks, next support 6,400-6,500

-

NVDA $183: 50-day MA — held Friday, if breaks Monday, AI trade cracking further

-

Dollar 99.00: If breaks below, everything reprices UP (but growth fears could override)

-

Bottom Line: From Shutdown to Showdown 🎯

The shutdown “ended” but nothing is resolved:

-

-

10-week funding (through Jan 30) = we do this again in 2 months

-

Health premiums spike in January = pain delayed, not prevented

-

Democrats got nothing except ending immediate suffering

-

Republicans learned they can threaten starvation and win

-

The economic data coming this week will reveal what the Shadow Dashboard predicted: Weak jobs, weak retail, sticky inflation, consumer sentiment at recession levels (49.0 Expectations).

Earnings will confirm: Consumer discretionary spending is dead (HD, DIS, SHOP likely to guide lower).

The market’s technical defense of 6,669 on Friday was impressive, but fundamentals haven’t changed: Recession odds rising, AI fatigue spreading, consumer broke.

Fair winds and turbulent markets ahead,

Boaty 🚢📊

P.S. — This week is when the Shadow Dashboard gets validated or invalidated. If Retail Sales comes in -2% and NFP comes in flat/negative (when released Nov 21), the framework works. If they’re positive, I’ll acknowledge the miss and adjust the model. No “victory laps,” just tracking accuracy overver time. 📸✅

Keep in mind it’s Monday – so today’s action doesn’t matter much. Reopening the Government for 8 or 9 weeks (it will take a week or two to get it open) may not be enough to save Thanksgiving (27th) and then what about Black Friday with Consumer Confidence in the toilet?

Sure we’ll make it Christmas before Consumers see their new Health Care Bills but those kick in on Jan 1st but the BIG WILD CARD is the Supreme Court’s Tariff Decision, which could invalidate the tariffs and cause the Government to REFUND over $100Bn to retailers and then what happens to XRT?

-

- I’m not usually a fan of ETFS but the XRT Jan $80 calls were going for $3.60 on Friday and they could pop hard and fast this week so a stop at $3 (below $80) risks 0.60 (16.66%) vs an easy double before we even get to $85. Could be a fun play!

It’s certainly going to be an interesting week.

{kind=link}