I hope you enjoyed the Super Bowl – or at least the commercials for weight-loss drugs and AI overlords…

I hope you enjoyed the Super Bowl – or at least the commercials for weight-loss drugs and AI overlords…

If you looked only at the headlines this weekend, you’d think we were living in a golden age. The Dow Jones Industrial Average finally cracked the 50,000 barrier on Friday, a psychological milestone that had President Trump immediately predicting Dow 100,000 by 2029. Nothing like a little linear extrapolation to start the week. I had the Round Table do a Wrap-Up Report for last week, in case you missed anything:

While the Industrials were popping champagne, the rest of the market was nursing a serious hangover: The Nasdaq fell 1.8% last week and the “Magnificent Seven” aren’t looking so magnificent- with the S&P 500 effectively flat.

The narrative that AI prints infinite money hit a wall last week; Amazon (AMZN) announced a staggering $200Bn in Capital Expenditures for 2026 and Google (GOOGL) is ramping up to $185Bn. Wall Street, who are famously impatient, looked at those numbers and asked, “Where is the ROI?” The answer seems to be “eventually,” which is why Amazon shares took a nose dive.

This feeds into the broader skepticism surrounding Fed nominee Kevin Warsh, who is betting the house that AI will trigger a productivity miracle to offset inflation. Unfortunately, a new poll shows 60% of economists think Warsh is dreaming; they don’t see AI moving the needle on inflation or interest rates for AT LEAST two years.

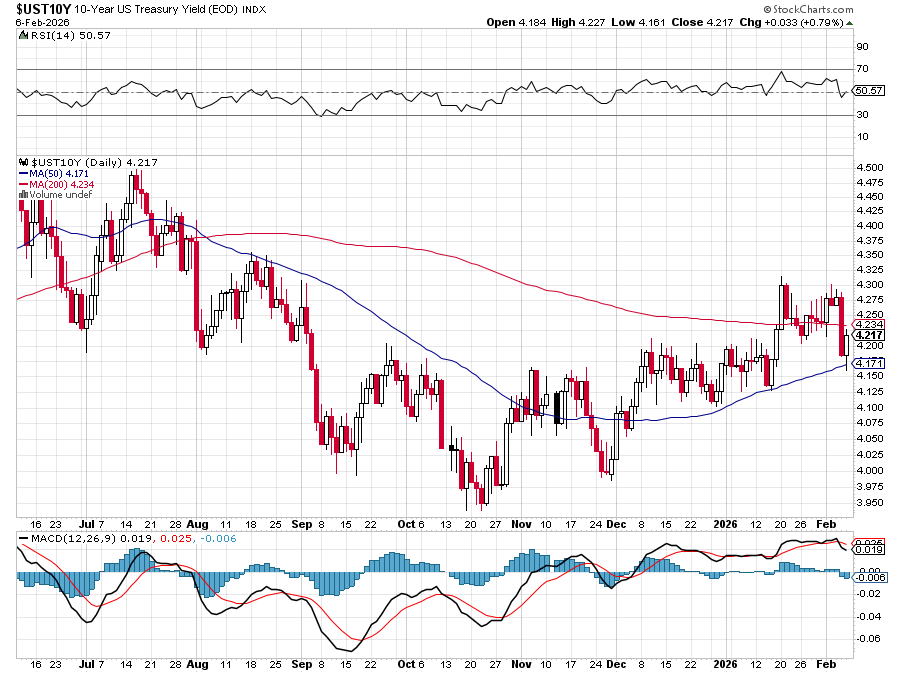

While everyone was watching the Dow, a much more dangerous story broke overnight: Chinese regulators are urging their banks to curb exposure to U.S. Treasuries. This isn’t just a geopolitical spat; it’s a liquidity issue. They are citing (correctly) “concentration risk” and, if Chinese institutions start quietly unloading American debt while the U.S. deficit flies high, bond yields (already creeping up, with the 10-year back at 4.21%) could spike. We are already seeing the 30-year yield tick up to 4.88%. Keep a very close eye on TLT and the yield curve this week; the Dow can’t hold 50K if rates break out!

Remember the “Trump Bump” for crypto? That is GONE! Bitcoin (BTC) has crashed roughly 45% from its October highs, briefly plunging to $60K last week before a dead-cat bounce to $69K this morning. The market has realized that “policy promises” don’t equal liquidity. BofA notes that the Dollar has fallen 14% since the inauguration, mirroring the President’s approval ratings among Dollar-holders.

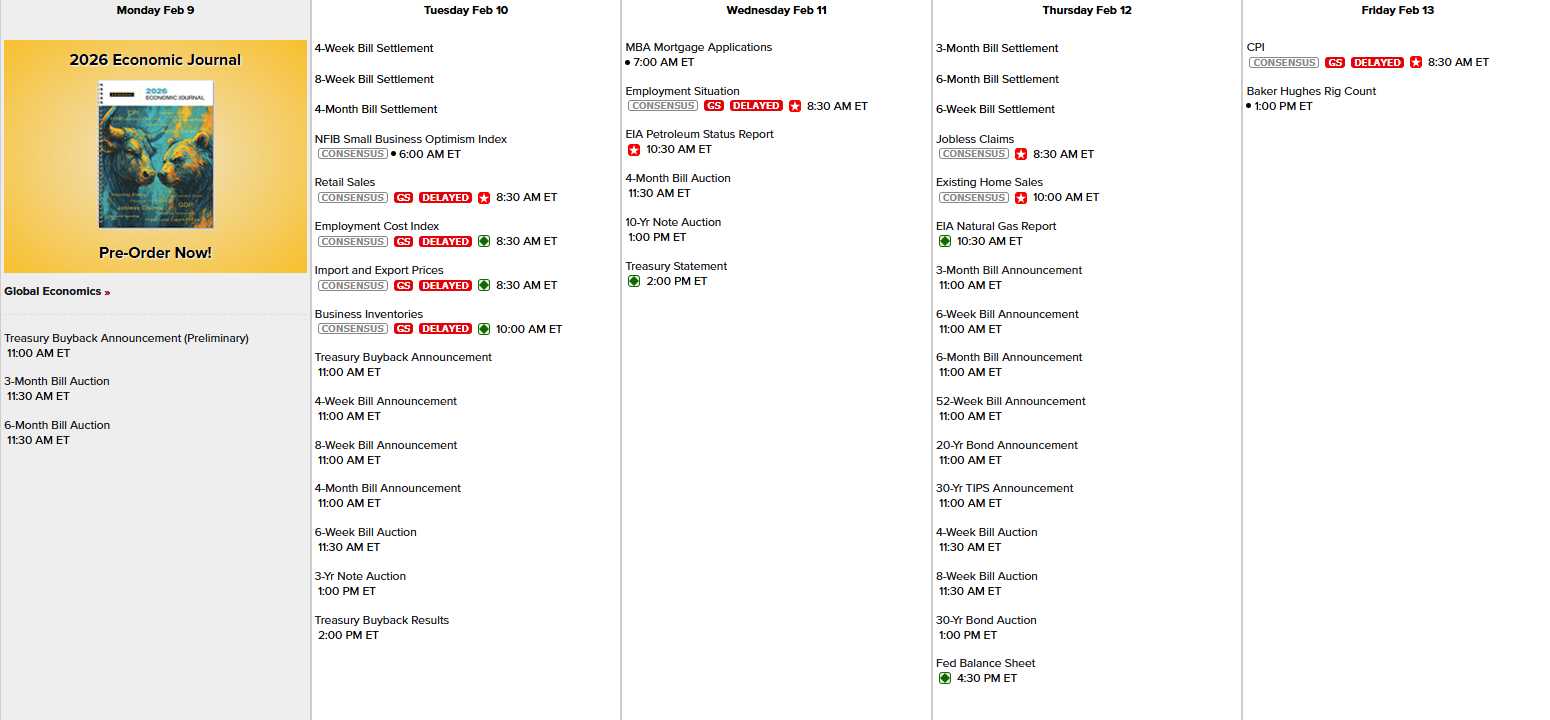

The week ahead is a crowded one. Because of the partial government shutdown (remember that?), the January Jobs Report was delayed and will now drop on Wednesday. We also get the all-important CPI data on Friday. If Inflation looks sticky, the Fed’s “patience” will suddenly look like “paralysis” and investors will get worried fast!

Earnings are going to be interesting in the second (and last) huge week of the quarter:

-

- Monday: Cleveland-Cliffs (CLF) kicks us off. They missed on revenue but beat on EPS – classic cost-cutting measures.

- Tuesday: Ford (F), Coca-Cola (KO), and Shopify (SHOP).

- Wednesday: Cisco (CSCO) and McDonald’s (MCD).

- Thursday: Airbnb (ABNB) and Applied Materials (AMAT).

- Friday: Moderna (MRNA)

The Nikkei soared to a record high after PM Takaichi secured a supermajority, fueling hopes for big fiscal spending (and a weaker Yen). Nonetheless the Dollar fell 1% on news of China’s withdrawal from Dollar assets and that weakness is giving US stocks and commodities a false sense of strength this morning – so BE CAREFUL!

We have a LOT of notes to auction this week and, if the International Buyers are going on strike – that can be BIG TROUBLE! Retail Sales, Employment Costs and Import/Export Prices tomorrow, Non-Farm Payrolls Wednesday AND the 10-Year Auction and CPI on Friday rounds out our data week – the focus will still be on earnings.

Hims & Hers (HIMS) is down 20% pre-market after they bowed to pressure from Novo Nordisk (NVO) and the FDA – agreeing to stop selling their $49 compounded “knockoff” Wegovy. It was fun while it lasted, folks, but Big Pharma always wins…

This is a strange divergence: We have Japan partying, the Dow at 50,000 and Elon Musk pivoting SpaceX to focus on the Moon because Mars is taking too long (and was never realistic). Yet, we have a tech correction, a crypto collapse, and China pulling back on U.S. debt – all at the same time!

Be VERY careful out there. As the “Super Bowl Indicator” reminds us – market superstitions are fun but LIQUIDITY is what pays the bills…

{kind=link}