I am STILL working on the LTP Review (1/3 done).

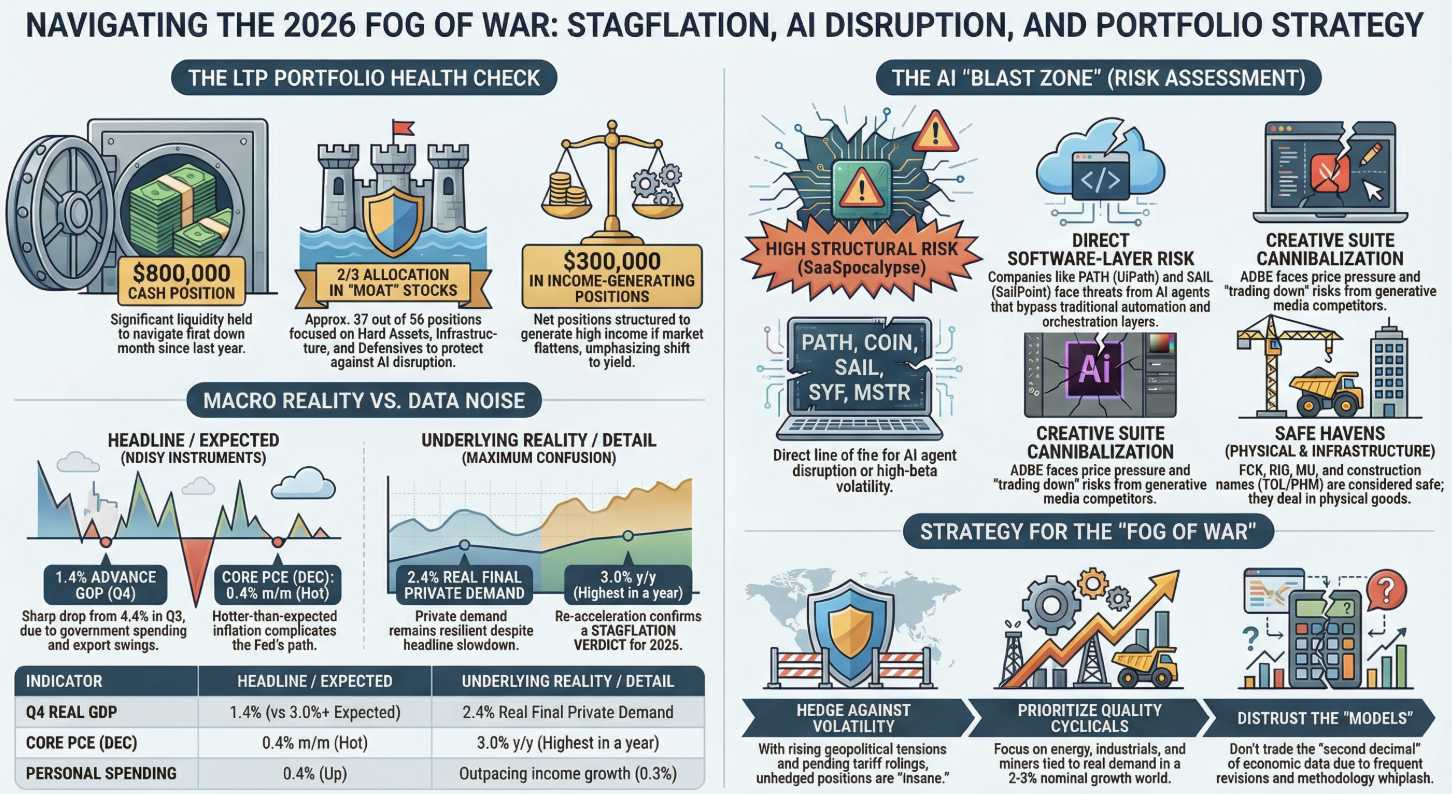

This is our first down month since we started on June 4th of last year so we’re carefully going through adjustments, as well as considering who to cut loose and who to add. We have a lot more CASH!!! ($800,000) than we started with ($500,000) plus net $300,000 worth of positions that are capable of generating A LOT of income – as long as the market flattens out a bit – which is what we hope.

I asked Boaty to look over our positions, incorporating our new concerns now that we’re seeing earnings and here’s his extensive summary:

🚢 A few names in that list sit much closer to the blast zone of the “AI scare trade” than others. I’d flag COIN, PATH, SAIL, SYF, MSTR, and to a lesser extent ADBE, PINS, LULU as the ones to keep under tighter surveillance, not necessarily automatic sells.

1) Direct “SaaSpocalypse” / software‑layer risk

These are closest to the “AI agents eat per‑seat software” thesis.forbes+4

-

-

-

PATH (UiPath) – Squarely in the crosshairs. Its whole story is “we automate workflows with bots,” and the market is asking whether Anthropic/Claude‑style agents plus platform tools will bypass RPA and orchestration layers. I’d treat PATH as speculative now: small position, very clear lines in the sand on revenue growth and net new ARR.digitalapplied+1

-

SAIL (SailPoint / identity governance) – Identity/IGA is more protected than generic SaaS, but it’s still a software layer that can get margin‑compressed as AI automates a lot of the audit, policy, and workflow grunt work. Not an automatic sell, but one where you want proof they can use AI to enhance moat and pricing power, not just see price pressure.forrester+2

-

ADBE (Adobe) – A high‑quality franchise but absolutely in the AI crossfire: generative media tools directly compete with its creative suite, and there’s a real risk of cannibalization/price pressure even if Adobe ships great AI of its own. I wouldn’t call it “dangerous,” but I’d demand:cnn+2

-

-

solid net new ARR,

-

clear monetization of Firefly/Gen‑AI, and

-

no sign of users trading down to cheaper AI tools.

-

-

-

-

2) Financial / crypto names with structural AI pressure

AI is now hitting finance, brokerage, and asset‑management workflows, not just software.finance.yahoo+2

-

-

-

COIN (Coinbase) – Still mostly a tollbooth on crypto trading and stablecoins. Its risk is less “AI eats us” and more “if crypto volumes and volatility don’t come back, the business is over‑built,” plus regulatory overhang. Structurally higher‑risk; I’d keep it sized small and mentally treat it as a leveraged bet that crypto remains mainstream.

-

SYF (Synchrony) – Squarely in a sector Wall Street is now selling on AI disruption fears: lenders, card issuers, and wealth/insurance platforms where AI can compress spreads and fees by automating underwriting and comparison. It’s cheap and profitable now, but it is a risk‑on financial; watch credit quality and any signs of AI‑enabled competition or regulatory price caps.merlintrader+2

-

MSTR (MicroStrategy) – This is basically a leveraged BTC proxy with some BI software attached. AI doesn’t help or hurt the core thesis much; the danger is simply that it’s a highly levered, high‑beta play on one volatile asset. Not an AI loser per se, but absolutely “dangerous to hold” if you don’t want crypto‑style drawdown risk.

-

-

3) Consumer, media, and attention‑economy names

AI personalization and agents will change how consumers discover and shop.

-

-

-

PINS (Pinterest) – Could go either way. Best case: AI makes its visual search/shopping even more valuable; worst case: mega‑platform agents (Meta, Google, Amazon) intermediate discovery and capture more of the shopping funnel. I’d call it sensitive to AI execution: not a clear loser, but you want to see user/engagement metrics and monetization holding up.qz+1

-

LULU – Brand + physical product = safer, but AI‑driven shopping and competition (fast fashion, personalized recs from platforms) can pressure multiples. Business itself isn’t being automated away; the risk is more “valuation compresses if growth slows” than structural extinction.

-

CMCSA, T, TSLA – All exposed to AI shifts but also have big physical or infra components (networks, factories, content libraries). Not in the “dangerous SaaS middle” bucket in the way PATH/SAIL are.

-

-

4) Names I don’t worry about from an AI‑disruption lens

These could still be bad trades for macro/stock‑specific reasons, but they’re not obviously in the AI blast radius:

-

-

-

Hard assets / physical economy / infra: B (Barrick), EPD, FCX, GFI, SLB, STLA, PR, RIO, UUUU, WHR, PHM/TOL (builders), PR, TM, TSLA’s manufacturing side, MU, WDC, TER, QCOM, INTC, GNRC, HPQ, HELE. They might get repriced for cycle/commodities/rates, but not because “agents replaced them.”

-

Defensives and big moats: AAPL, GILD, NVO, JPM, LMT, TGT, ALLY, HRB, TROW, ORCL, PFE, PPL, GILD, ADBE (again, with caveats) and ON. AI changes how these operate; it doesn’t obviously erase them in 2–3 years.

-

-

Bottom line

From an AI disruption + SaaSpocalypse lens, the positions I’d treat as genuinely higher‑risk to hold (not just trade) are:

-

-

-

High structural risk: PATH, COIN, SAIL, SYF, MSTR.

-

Medium structural / valuation risk: ADBE, PINS, LULU (plus any others where the multiple is still “old world” but the narrative has shifted).

-

-

Everything else is more about macro, cycle, or single‑name execution risk than about being on the wrong side of the AI revolution.

How’s that for useful? It also had the added benefit of identifying 37 stocks we already have (out of 56 total) that fit our key criteria of “Hard Assets, Physical Economy, Infrastructure” and “Defensives with Big Moats” which we identified back in November as our Key Investing Themes for 2026 – so no surprise the LTP has 2/3 of it’s assets in those stocks.

Why is 1/3 of our allocation NOT in those stocks? Because we COULD be wrong and you never want to be in a position where ALL of your positions can go bad at the same time.

We gamified Trump’s Gulf War yesterday in the PSW Morning Report and now he’s given Iran 10-15 days to pay up or he’ll break their legs (or maybe I was watching the Sopranos) but the bigger story today is another Trump Disaster – the one we warned about in: “Fact Check Thursday – What is Really Going on in the Economy?“:

🚢 Income and spending are fine, but the “instruments” we’ve been complaining about just did exactly what we warned: GDP fell off a cliff while the Fed’s favorite inflation gauge quietly re‑accelerated. That’s a nasty combo for anyone still trading the old “soft landing, clean data” story.

What just happened in the data

-

-

-

-

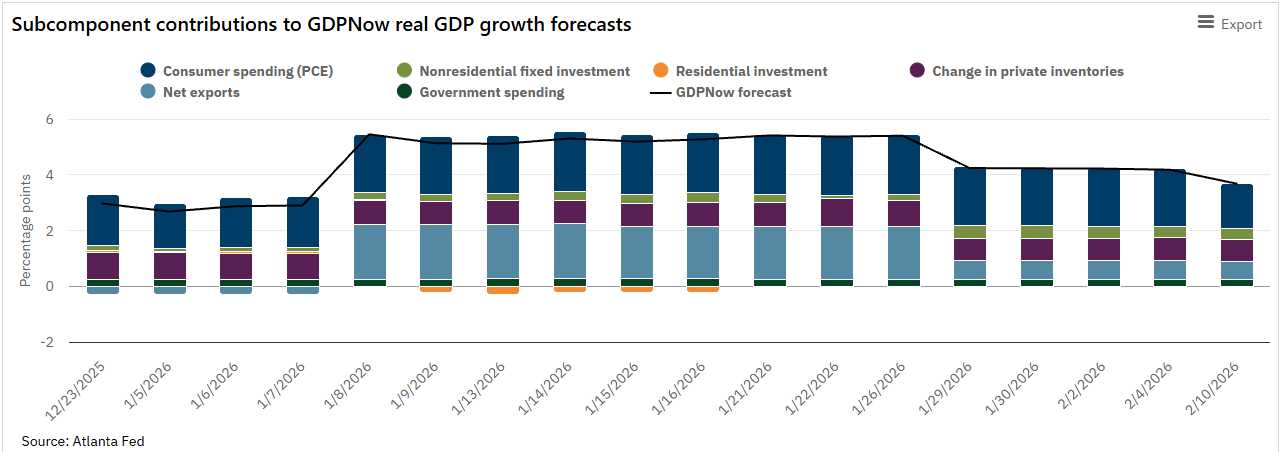

GDP (advance, Q4):

-

Real GDP slowed to 1.4% annualized vs 4.4% in Q3 and ~3.0–3.6% expected.bea+3

-

Real final sales to private domestic purchasers (consumer + private investment) grew 2.4%, only a modest step down from 2.9%—so underlying private demand didn’t collapse; the big swing was in government spending and exports.bloomberg+1

-

Translation: the headline looks like a hard slowdown, but the “private economy” is still growing near 2½%; the wobble is in the public/international parts of the equation.

-

-

-

-

-

-

PCE / core PCE (Dec):

-

Headline PCE up 0.4% m/m, core PCE also 0.4% m/m, both hotter than the 0.2–0.3% expected.investing+4

-

Core PCE is now running about 3.0% y/y, up from 2.8%—its highest in roughly a year.foxbusiness+3

-

This is exactly what some previews hinted at: core PCE “as much as 0.4% m/m” due to components that were artificially soft during the shutdown months snapping back.capitaleconomics+1

-

-

-

-

-

-

Income and spending:

-

Personal income +0.3% (as expected), spending +0.4% vs 0.2% prior—consumers are still outspending their income growth at the margin.[ng.investing]

-

That supports the “no imminent consumer collapse” story but is not what the Fed wants to see if they’re trying to squeeze inflation back to 2%.

-

-

-

This is exactly the kind of revision‑ and methodology‑driven whiplash we’ve been ranting about: the headline GDP now says “big deceleration,” while the price side quietly says “actually, inflation isn’t done with you yet.”

How it lines up with what we’ve been saying

-

-

-

We argued that treating GDP, wages, and nowcasts as precise guides is dangerous when revisions and shutdown distortions are this large. GDP just printed less than half the consensus estimate a quarter after a 4.4% blowout—not because the real economy literally slammed on the brakes overnight, but because of swings in public‑sector accounting and exports.nasdaq+2

-

We also flagged that underlying inflation (especially services) wasn’t nearly as tamed as the “2‑handle CPI” narrative implied, and that PCE could easily surprise on the hot side once the shutdown noise washed out.mnimarkets+4

-

Today’s tape is the logical result: weak growth headline + sticky core PCE = maximum confusion for anyone who still thinks the models are gospel.

-

-

This is why we treat the data as noisy instruments and build in a margin of error instead of trading the second decimal.

What it means going into PMI, New Home Sales, Sentiment

Three things to watch:

-

-

-

PMI (9:45): We already know January ISM Manufacturing ticked back above 50, and S&P Global’s PMIs have been flirting with expansion too.prnewswire+1

-

If PMI is 50+ (it should be) with reasonable new orders, it reinforces the idea that real‑economy demand is okay, and the 1.4% GDP print is more a composition/story problem than a collapse.

-

If PMI disappoints sharply, the narrative becomes “growth slowing AND inflation sticky,” which is the stagflation scare the market really doesn’t want!

-

-

-

New Home Sales (10:00):

-

-

Starts/permits beat earlier, mortgage apps just bounced; if New Home Sales are stable to better, it confirms housing is bending, not breaking under rates.floridarealtors+1

-

That bolsters the “slow‑growth, no recession yet” view—and keeps pressure on the Fed, because a still‑alive housing market plus 0.4% core PCE is not a cut‑now backdrop.

- Negative housing prices are still a very serious concern.

-

-

-

-

-

Consumer Sentiment (10:00):

-

If sentiment firms, it tells you households are absorbing higher prices and higher rates without cracking; that’s good for earnings but bad for anyone hoping inflation glides down painlessly.

-

If sentiment rolls over hard, you get the opposite: Fed stuck between a weaker consumer and hotter PCE.

-

-

Takeaways for investors

For the Morning Report, I’d boil it down to:

-

-

-

Don’t anchor on the 1.4% GDP headline alone. Real final private demand is still ~2½%; the “hard slowdown” is more in government/export arithmetic than in Main Street.bea+2

-

The Fed’s job just got harder, not easier. A 0.4% core PCE print and 3.0% y/y reading tell Powell & Co. they cannot credibly accelerate cuts yet; the Minutes’ cautious tone now looks very justified.morningstar+3

-

This is not a clean bull or bear signal—it’s a stock‑picker’s tape.

-

Quality cyclicals and hard‑asset names tied to real demand (energy, industrials, miners, selected housing) still have a lane in a 2–3% nominal growth world.

-

High‑multiple “story stocks” that need a fast‑cutting Fed and perfect disinflation are the ones out on the limb: today’s PCE/GDP mix makes that path less likely, not more.

-

-

-

So the numbers don’t confirm a boom or a bust but they do confirm that WE CAN’T RELY ON THE NUMBERS and that means we’d BETTER be investing in only the best-managed companies with experienced teams who have survived shocks like Covid and Feb-April’s Tariff Turmoil because the Supreme Court could rule on tariffs any day and a major war can break out in the Middle East at any moment (because Trump just put 20,000 soldiers into harm’s way).

What we can see is that this is, indeed a Stagflationary environment – just like we predicted it would be in 2026 as growth slows and inflation continues and another war for oil isn’t going to be the cure – no matter how many FIFA Peace Prizes Trump receives…

There’s no reason to panic out of the market (yet) but it would be INSANE not to hedge what you have – as the situation is volatile – to say the least!

Have a great weekend,

-

- Phil

")

{kind=link}