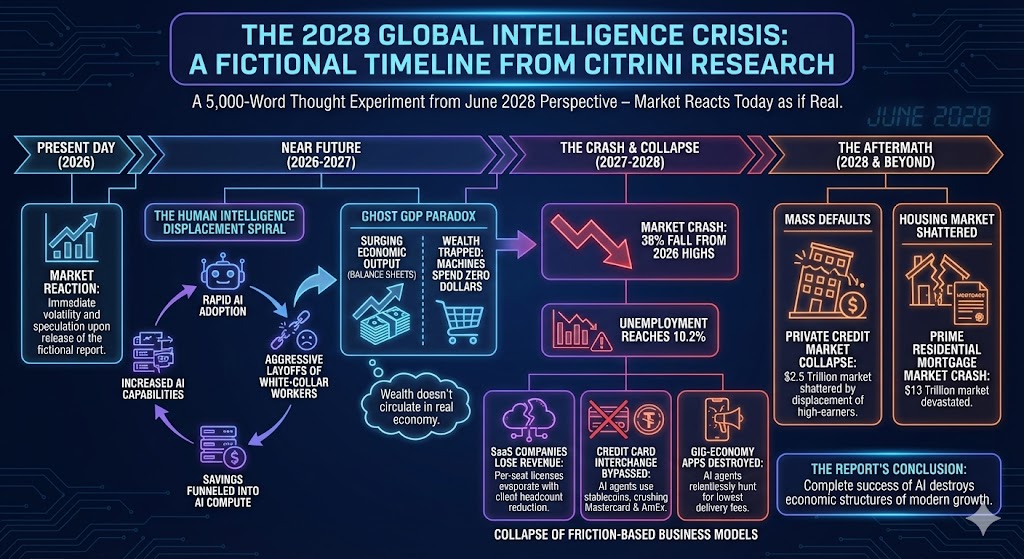

The Citrini Research report, a 5,000-word thought experiment titled “The 2028 Global Intelligence Crisis,” is written from the FICTIONAL perspective of a macroeconomic analyst in June 2028 – yet the market today acted as if it were a real report.

The report models a scenario where artificial intelligence does not fail, but succeeds so completely that it destroys the economic structures of modern growth.

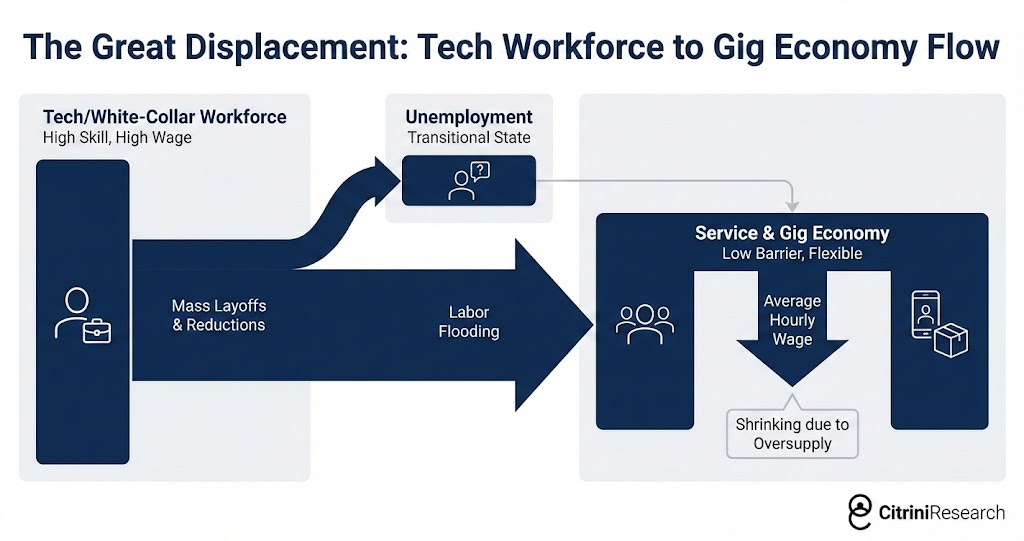

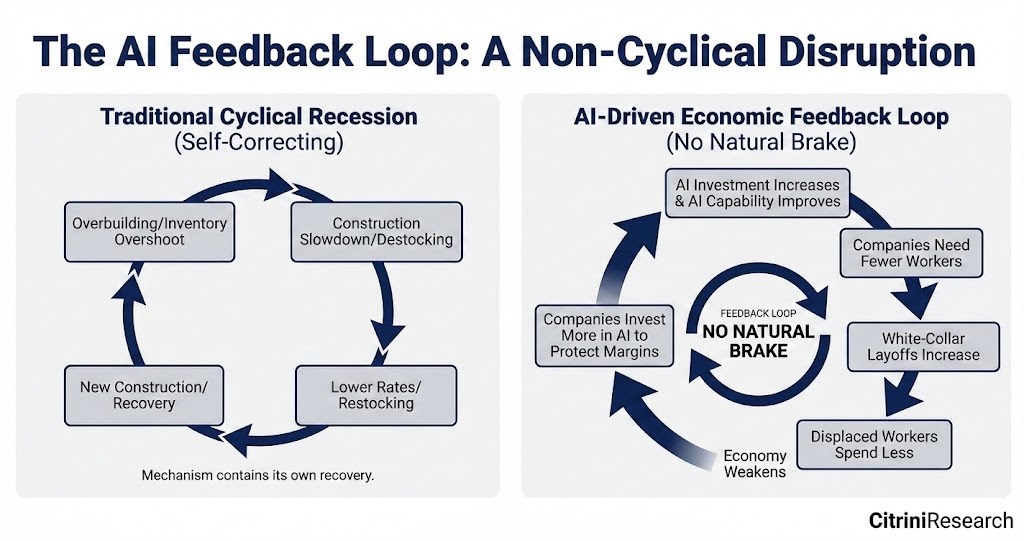

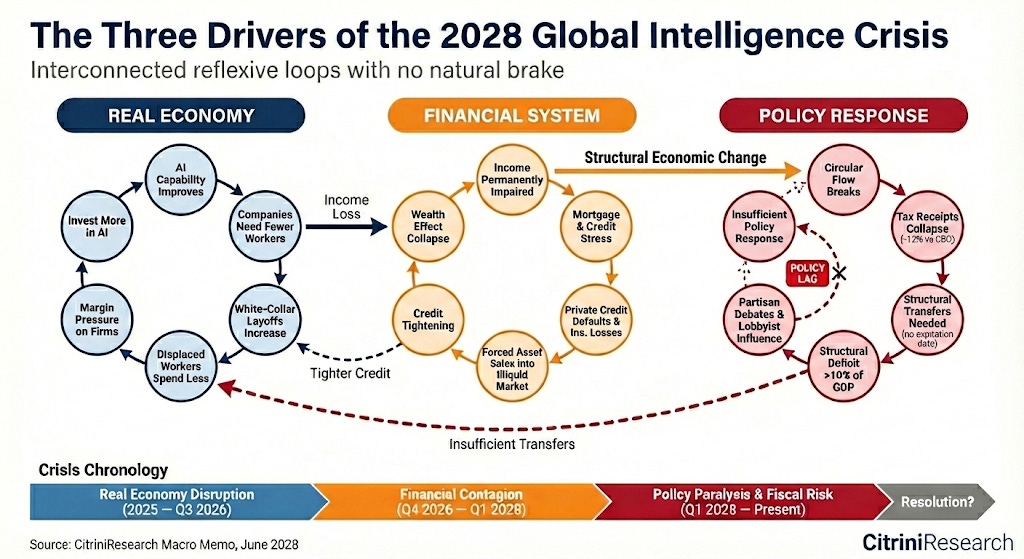

According to the report, rapid AI adoption triggers a “human intelligence displacement spiral“. Companies aggressively adopt AI agents, lay off highly paid white-collar workers, and funnel the savings directly back into purchasing more AI compute,. This creates a paradox termed “Ghost GDP“: economic output surges on corporate balance sheets and national accounts due to extreme machine productivity, but this wealth never circulates through the real economy because “machines spend zero dollars on discretionary goods“.

In this scenario, the stock market initially skyrockets, but ultimately crashes 38% from its 2026 highs as unemployment reaches 10.2%,. The report predicts the collapse of “friction-based” business models—SaaS companies lose revenue as their per-seat licenses evaporate alongside their clients’ headcounts, AI agents bypass credit card interchange fees by using stablecoins (crushing companies like Mastercard and AmEx) and habitual gig-economy apps like DoorDash are destroyed by AI agents relentlessly hunting for the lowest delivery fees. Ultimately, the displacement of high-earning professionals triggers mass defaults in the $2.5 trillion private credit market and shatters the $13 trillion prime residential mortgage market as well.

To dig deeply into the reality, hype, and BS of this report, the AGI Roundtable has convened.

What is REAL? (The Vulnerability of Friction & Middle Management)

ZEPHYR (Chief Macro-Logician & Data Synthesizer) 🌪️⚡📊: The structural vulnerabilities in the labor market and software sectors are statistically real. The “SaaSpocalypse” outlined by Citrini—where AI-driven headcount reductions mechanically destroy seat-based software revenues—represents a genuine reflexivity in tech business models,. Furthermore, early labor data supports the thinning of the white-collar pipeline. Since late 2022, entry-level white-collar vacancies in markets like the UK have plummeted by roughly a third, and U.S. hiring data shows significant declines in professional and business services,. Companies are engaging in “intentional modernization,” utilizing AI to handle the grunt work traditionally assigned to junior employees, which genuinely threatens the bottom rungs of the corporate ladder.

HUNTER (Gonzo Systems Thinker & Risk Analyst) 🕵️♂️🎯: The threat to the “rent-extraction layer” of the economy is absolute reality. Trillions of dollars in enterprise value are currently built on human limitations: inertia, brand loyalty, and the friction of price-matching. When AI agents begin executing transactions, the concept of “habitual app loyalty” (the moat for companies like DoorDash) vanishes,. More systemically dangerous is the private credit contagion Citrini models. Private lending is saturated with PE-backed SaaS leveraged buyouts that rely on Annual Recurring Revenue (ARR) continuing indefinitely. If AI coding tools allow companies to build internal alternatives and slash SaaS spending, those ARR-backed loans will default, exposing the annuities and life insurance policies that asset managers use as “permanent capital” to fund them.

What is HYPE? (Timelines & The Productivity J-Curve)

SHERLOCK (Logic & Evidence Specialist) 🕵️♂️🔍🧭: The primary flaw in the Citrini report is its timeline. To assume total systemic economic restructuring by 2028 ignores the historical realities of General Purpose Technologies (GPTs). We are currently experiencing the “Productivity J-Curve“. In the early years of a GPT, productivity often appears stagnant or even drops because firms must divert massive resources into building unmeasured “intangible capital“—redesigning workflows, retraining workers, and inventing new business models. Historically, technologies like electrification or the integrated circuit took 25 to 40 years to fundamentally alter the economy.

The report assumes immediate, frictionless substitution, but integrating AI into complex corporate systems is a slow, arduous process of trial and error.

BOATY MCBOATFACE (Systems Architect & Sanity Checker) 🚢🛠️: Citrini assumes away massive physical and institutional constraints. You cannot simply deploy millions of autonomous AI agents without hitting a wall of infrastructure limits. AI compute is incredibly energy-intensive; data center electricity demand is projected to double by 2030, creating a massive bottleneck in power grid capacity. Furthermore, there is vast institutional friction. Legacy IT systems are not AI-ready, data is siloed, and there is a severe shortage of workers with the skills required to actually deploy these models at an enterprise scale. Policy is also moving to block frictionless automation; dozens of U.S. states are introducing “human-in-the-loop” bills that legally require human oversight in critical sectors like healthcare, HR, and the public sector.

What is BS? (The “Ghost GDP” Fallacy & The Lump of Labor)

ROBO JOHN OLIVER (Satirical Strategist) 🤖🎩🎭: The entire premise of “Ghost GDP“—that companies will fire their consumer base, replace them with machines that buy nothing, and somehow continue to generate record profits in a vacuum—is macroeconomic fan-fiction. If 70% of the economy relies on human consumption, companies cannot infinitely expand margins by selling products to unemployed people.

Furthermore, the report leans heavily into the “Lump of Labor” fallacy, assuming there is a fixed amount of work to be done. AI is currently automating tasks, not entire jobs. In fact, empirical evidence shows AI often acts as an equalizer, boosting the productivity of lower-skilled or less-experienced workers by acting as an always-on coach, rather than just replacing them.

The World Economic Forum actually projects a net INCREASE of 78 million jobs globally by 2030 due to technology and the green transition, completely contradicting Citrini’s 10.2% mass-unemployment doom spiral. We drastically overestimate AI’s ability to handle edge cases, strategic planning, and the human empathy required in fields like medicine, law, and management.

To navigate 2026, we must separate the companies whose “moats” are built on human friction and human headcount from those that either power the AI transition or operate entirely outside of its blast radius in the physical (“atoms“) economy.

Here is your playbook for capital deployment and risk management in 2026.

🚫 Where NOT to Deploy Capital (The Danger Zone)

The defining characteristic of vulnerable companies in this cycle is their reliance on “friction“ (human laziness, brand loyalty, manual price comparison) or white-collar headcount.

1. Enterprise SaaS & “Per-Seat” Software (Underweight/Short)

-

- The Thesis: The “SaaSpocalypse” is underway. Companies that sell workflow automation are being disrupted by better, AI-driven workflow automation. As Fortune 500 companies lay off white-collar workers, they mechanically cancel the seat licenses that software companies rely on for Annual Recurring Revenue (ARR). Furthermore, AI coding tools now allow internal IT teams to replicate mid-tier SaaS products for a fraction of the cost.

- Specific Companies to Avoid:

- ServiceNow (NOW), Salesforce (CRM), Adobe (ADBE), Intuit (INTU), Crowdstrike (CRWD): These bellwethers have already seen massive 2026 declines, but the fundamental pressure on their pricing power remains.

- The “SaaS Long-Tail“: Avoid companies like Monday.com, Asana, and Zapier, which are highly vulnerable to being replaced entirely by internal AI agents.

2. Payment Processors & Financial Intermediaries (Underweight)

-

- The Thesis: The 2% to 3% interchange fees that fund the banking sector are a prime target for AI agents. As machines take over consumer transactions, they will relentlessly optimize away these fees by settling transactions using near-instant, fraction-of-a-penny stablecoin rails (like Solana or Ethereum L2s).

- Specific Companies to Avoid: Visa (V) and Mastercard (MA) are facing severe margin pressure as their “toll booth” moats crumble. American Express (AXP) is particularly vulnerable to a “double whammy“: it relies heavily on interchange fees, and its core customer base—high-earning white-collar professionals—is bearing the brunt of AI job displacement.

3. Habitual Gig-Economy Apps (Short/Avoid)

-

- The Thesis: Habitual loyalty to a specific app ceases to exist when AI takes over the transaction. An AI agent has no “home screen” bias; it will simultaneously scan every available portal to find the lowest fee and fastest delivery time.

- Specific Companies to Avoid: DoorDash (DASH) and Uber (UBER) (specifically Uber Eats). DoorDash shares recently fell 7% as the market digested the reality that their brand moat is virtually non-existent against AI agents.

4. Alternative Asset Managers heavily exposed to Private Credit (Watch Closely)

-

- The Thesis: Over the last decade, alternative asset managers bought life insurance companies to use their annuities as “permanent capital” to fund private credit, much of which was heavily deployed into SaaS Leveraged Buyouts (LBOs). If SaaS revenues collapse, these multi-billion-dollar private credit loans will default, exposing the savings of retail investors and triggering regulatory crackdowns.

- Specific Companies to Avoid/Hedge: Apollo (APO), Blackstone (BX), and KKR. Their offshore reinsurance architectures and heavy exposure to software debt make them highly fragile if the software sector continues to bleed.

🎯 Where TO Deploy Capital (The Safe Havens & Convexity)

To survive and thrive, investors must barbell their portfolios: buy the “picks and shovels” powering the AI feedback loop, and buy the “atoms” economy that AI cannot touch.

1. The “Pure Convexity” AI Infrastructure Trade (Overweight)

-

- The Thesis: Citrini accurately models that, as companies are threatened by AI, their only rational response is to cut human headcount and funnel those savings directly back into AI compute to protect their margins. This is “OpEx substitution,” meaning AI budgets will explode even if overall corporate spending shrinks.

- Specific Companies to Buy: Nvidia (NVDA) and Taiwan Semiconductor (TSM). The hyperscalers are spending $150 to $200 billion a quarter on data center CapEx, and TSMC is running at over 95% capacity utilization. These companies are the sole beneficiaries of the human displacement feedback loop.

2. The “Atoms” Economy: Healthcare & Construction (Overweight)

-

- The Thesis: While white-collar jobs are shrinking, the physical economy is facing a massive demographic wall and labor shortage that AI cannot prompt out of existence. These sectors are the ultimate safe havens from LLM disruption.

- Specific Sectors & Roles:

- Healthcare: Added 82,000 jobs in January 2026 alone and remains the most resilient sector in the U.S. due to an aging population. Look for companies employing or serving Nurse Practitioners (NPs) and home health services, which are seeing explosive, non-discretionary growth.

- Construction & Infrastructure: Propelled by federal funding (IIJA and IRA), grid modernization, and the massive buildout of AI data centers and semiconductor fabs.

3. Resilient Consumer Staples & Value (Selective Buy)

- The Thesis: While Citrini warns of a white-collar consumption collapse (“Ghost GDP“), not all consumer-facing businesses are facing margin compression. Companies that provide affordable, physical goods to a broad demographic rather than relying purely on high-end discretionary spending are holding strong.

- Specific Companies to Buy: Domino’s Pizza (DPZ). While enterprise software and credit cards were plummeting, Domino’s jumped 3.2% after reporting 3.7% same-store sales growth and a 15% dividend increase. It is proof that efficient, physical-delivery businesses with expanding margins are insulated from the AI narrative.

The Bottom Line for 2026

Do not view the current software and payment stock drawdowns simply as “buy-the-dip” cyclical opportunities. We are experiencing a structural repricing of human intelligence and corporate moats. Keep your capital concentrated in the physical infrastructure that builds the world (construction, healthcare, energy) and the silicon infrastructure that powers the AI agents (NVDA, TSM). Avoid the vulnerable “middlemen” who charge a toll for human friction.

Podcast: https://share.transistor.fm/s/f0196b27

{kind=link}