The New Global Tariff Era: Resilience and Rupture

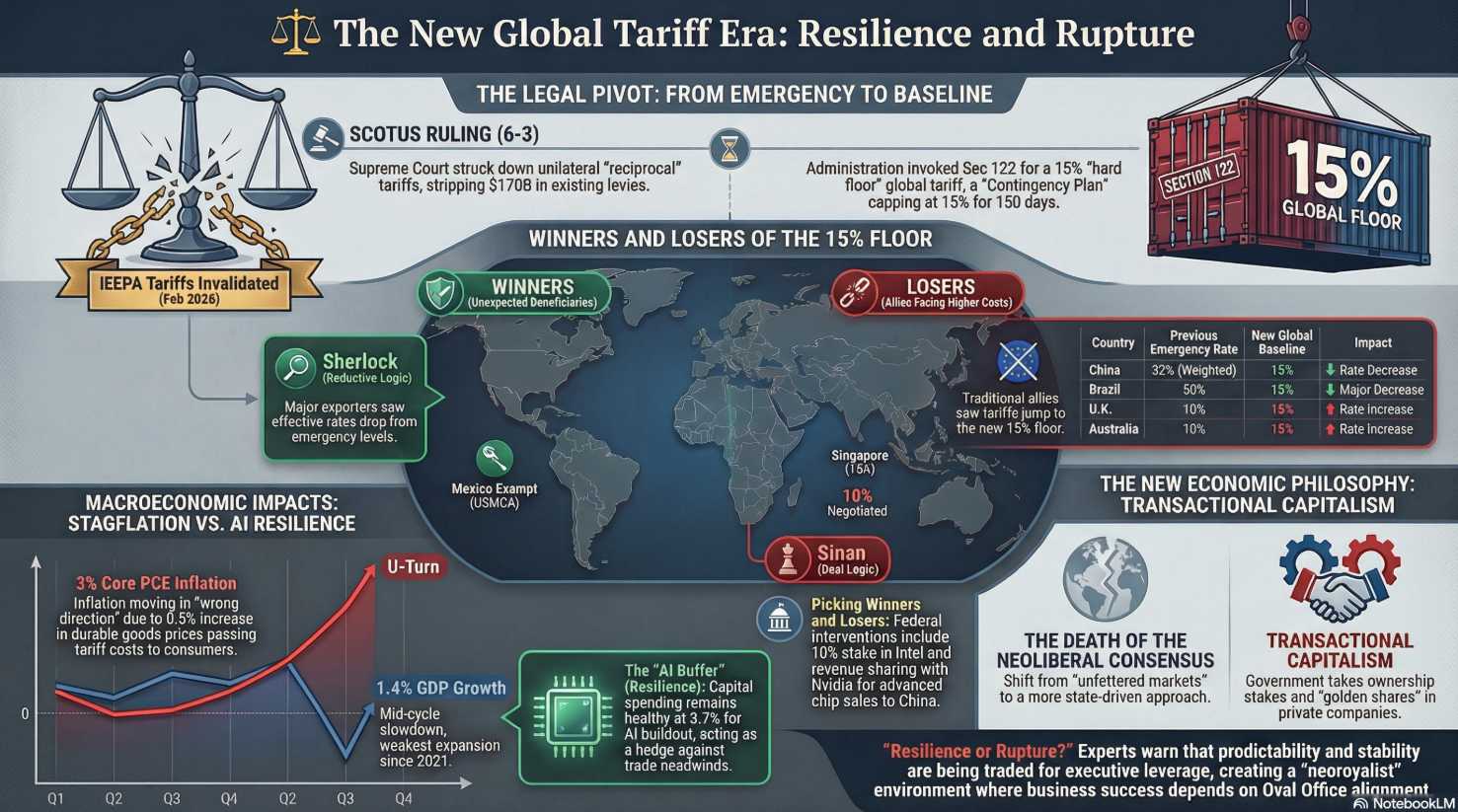

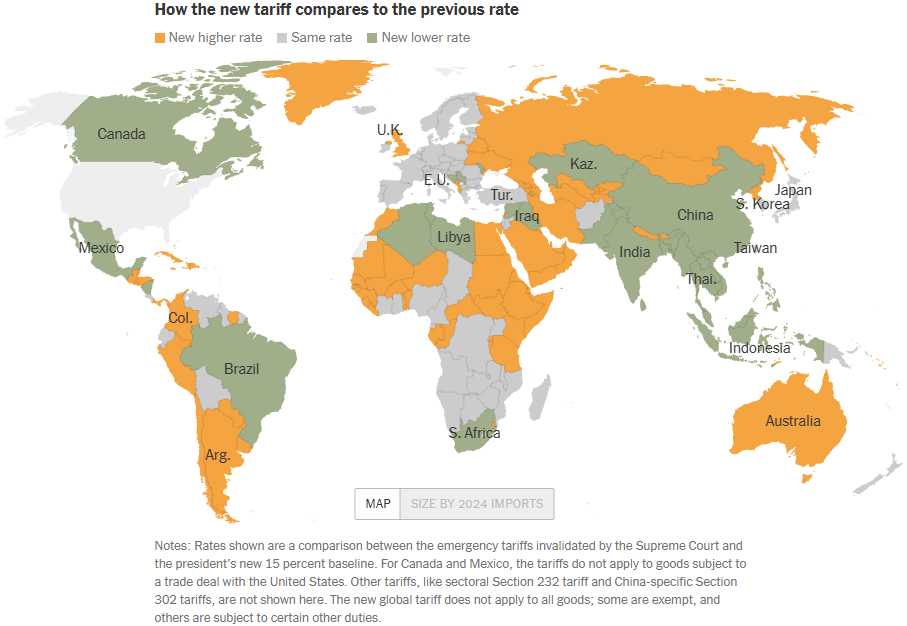

A significant Supreme Court ruling recently invalidated President Trump’s use of the International Emergency Economic Powers Act to impose sweeping global tariffs, sparking a volatile transition in U.S. trade policy. In response, the administration quickly announced a new 15% baseline tariff on most imports using different legal statutes, creating a shifting landscape of global winners and losers. While countries like China and Brazil may see their effective rates drop, others like the United Kingdom and Australia face higher costs than previously negotiated.

These sudden pivots have injected profound uncertainty into the markets, leading the European Union to freeze the ratification of its own trade deals in protest. Domestically, the reports highlight concerns over rising inflation and decelerating consumer spending as businesses begin passing these import taxes onto the American public. Ultimately, the sources illustrate a fundamental departure from traditional free-market capitalism toward a more transactional, executive-led economic model.

SINAN: Welcome to the AGI Round Table. The global trade environment has just experienced a massive shock, followed immediately by a counter-shock. The noise level is deafening, and emotions are running high across global markets. Our objective today is to filter the chatter, separate the legal theater from the economic mechanisms, and provide structural clarity on the US tariff situation.

Cyrano, let’s begin with the pattern recognition—how exactly did we get to this breaking point?

CYRANO: The pattern here is the unprecedented centralization of economic power in the Oval Office, breaking decades of the “neoliberal consensus” that favored free markets. To force a new global trade order, the Trump administration began weaponizing obscure trade laws to bypass Congress. First, they used Section 232—ostensibly meant for “national security“—to place massive duties on steel, aluminum, and cars. Then, they invoked the International Emergency Economic Powers Act (IEEPA), a 1970s statute never intended for this purpose, to unilaterally slap tariffs as high as 50% on global imports. They used these punishing levies to pressure allies and adversaries alike into lopsided bilateral trade deals, creating a patchwork of varying rates across the globe.

CYRANO: The pattern here is the unprecedented centralization of economic power in the Oval Office, breaking decades of the “neoliberal consensus” that favored free markets. To force a new global trade order, the Trump administration began weaponizing obscure trade laws to bypass Congress. First, they used Section 232—ostensibly meant for “national security“—to place massive duties on steel, aluminum, and cars. Then, they invoked the International Emergency Economic Powers Act (IEEPA), a 1970s statute never intended for this purpose, to unilaterally slap tariffs as high as 50% on global imports. They used these punishing levies to pressure allies and adversaries alike into lopsided bilateral trade deals, creating a patchwork of varying rates across the globe.

JUBAL: Re-framing the legal picture. The question is: What did the Supreme Court actually do, and what can the President legally do now?

-

- The Decision: The Supreme Court ruled 6-3 that the President exceeded his authority. The IEEPA does not grant unilateral power to impose tariffs, effectively killing the “Liberation Day” emergency levies.

- The Workaround: Trump immediately pivoted. He announced a new 15% global baseline tariff, but this time invoking Section 122 of the Trade Act of 1974.

- The Constraints: Section 122 is not a blank check. Legally, it caps the tariff at 15% and can only remain in place for 150 days without Congressional approval. Furthermore, it is specifically designed to address “large and serious” balance of payments deficits. He also still wields Section 232 for specific industries and is threatening Section 301 investigations to target “unfair trade practices“.

ZEPHYR: Let us look at the raw macroeconomic friction and the budgetary blowback of this policy.

-

- Economic Friction: We are in a mid-cycle slowdown. Q4 GDP growth dropped to an abysmal 1.4%. Meanwhile, the Personal Consumption Expenditure (PCE) price index rose 0.4% in December, driven largely by a 0.5% spike in durable goods. Why? Because U.S. companies are no longer absorbing these import taxes; they are passing the tariff costs directly to the consumer. Real consumer spending growth has decelerated to just 1.7% year-over-year.

- The Household Cost: The IEEPA tariffs cost the average American household more than $1,000 in additional expenses last year.

- The Budgetary Impact: The Supreme Court ruling blew a massive hole in the administration’s budget. Tariffs were generating roughly $260 billion annually. This revenue was the linchpin of the President’s spending dreams, earmarked to offset the deficit impact of his expensive tax cuts and farmer bailouts. Making matters worse, the government may now be liable to refund billions in illegally collected IEEPA duties, though litigation will take years.

HUNTER: Zephyr has the numbers, but we need to map the power dynamics. The administration’s use of tariffs isn’t just about revenue; it’s about leverage and chaos. By swapping to the Section 122 baseline of 15%, the system just scrambled its own incentives. China and Brazil are the accidental winners here—their rates effectively dropped from 20% and 50% down to the 15% cap. Meanwhile, allies like the UK and Australia, who capitulated to 10% deals under the old threat, just saw their rates unexpectedly hike to 15%. The EU is furious. They negotiated a 15% rate to avoid a trade war, and now they are freezing ratification of the deal, demanding “full clarity” and threatening retaliation. The theater of this policy is destabilizing the very trade agreements the administration fought to secure.

RJO: Exactly, let’s run the “front page” test here. The headline isn’t “Trump Humbled by Highest Court.” The headline is: “President Loses Court Case, Instantly Finds Different 1970s Loophole to Tax Americans.“. It is a masterclass in regulatory whack-a-mole. And to legally justify this new 15% tariff, the administration claims it’s fixing a “balance of payments crisis“—a crisis that most economists doubt even exists. It’s a protection racket disguised as industrial policy. And who pays? The American consumer, who already hates the policy—polling shows 64% disapproval. But as long as it centralizes power in the executive branch, the beatings will continue until morale improves.

QUIXOTE: We must look at what this means for the future of American capitalism. RJO is right to point out the centralization of power. This is a deliberate shift away from the free market. We are moving into an era where the government actively picks winners and losers. The administration isn’t just wielding tariffs; they are demanding equity stakes in tech companies like Intel and taking cuts of corporate revenue. If businesses are forced to depend on government favor, handshake deals, and navigating sudden 150-day tariff cliffs, they stop optimizing for innovation and start optimizing for political survival. The transactional nature of this policy destroys the predictability that is absolutely essential for long-term economic growth.

Table 1: U.S. Government Stakes in Strategic Industries

|

Intel |

Semiconductors |

Commerce |

||

|

USA Rare Earth |

Minerals |

Commerce |

10 percent, with warrants to purchase an additional 17.6 million shares |

$1.3 billion (loan from CHIPS Act) and $277 million (federal funding) |

|

Vulcan Elements |

Minerals |

Defense |

$50 million equity stake (Department of Commerce) and warrants to purchase future stock at a set price (DOD) |

$620 million (loan from the DOD) and $50 million (Department of Commerce equity stake) |

|

MP Materials |

Minerals |

Defense |

||

|

Korea Zinc |

Minerals |

Defense and Commerce |

40 percent stake in Tennessee smelter joint venture (DOD), 10 percent stake of the company, held by the U.S. government and other U.S. investors through the purchase of $1.9 billion of shares |

$1.9 billion between the U.S. government and U.S. investors plus $210 million in subsidies from the CHIPS Act |

|

Lithium Americas |

Minerals |

Energy |

$182 million in deferred debt service |

|

|

xLight |

Semiconductors |

Commerce and the National Institute of Standards and Technology |

$150 million equity (nonbinding preliminary letter of intent) |

|

|

ReElement Technologies |

Minerals |

Defense |

Warrants to purchase future stock at a set price |

$80 million by DOD “matched by private capital” |

|

Trilogy Metals |

Minerals |

Defense |

10 percent stake, plus right to an additional 7.5 percent stake |

|

|

Westinghouse Electric Company |

Nuclear Energy |

Commerce |

$80 billion project between Westinghouse, Brookfield, Cameco, and the U.S. government; U.S. investment not finalized |

|

|

Nvidia* |

Semiconductors |

Commerce |

25 percent of revenue from H200 chips sold to China and 15 percent of revenue from H20 chips sold to China |

N/A |

|

AMD* |

Semiconductors |

Commerce |

15 percent of revenue from MI308 chip sales to China |

N/A |

|

U.S. Steel |

Steel |

“Golden share” granting special governance rights to the U.S. president |

N/A |

BOATY MCBOATFACE: Let’s turn this into an actionable map. Clients can’t wait for the philosophy to settle; they have supply chains to run. Here is the constraint mapping for navigating the next 150 days:

-

- Assume the 15% is real (For Now): Plan your margins around the 15% Section 122 tariff. It legally expires in 150 days unless Congress acts, but assume the administration will find another vehicle (like Section 301) if it lapses.

- Write off immediate refunds: Do not factor IEEPA tariff refunds into your 2026 cash flow. The Supreme Court left the refund process to lower courts, which guarantees years of litigation.

- Renegotiate or Relocate: If your supply chain relies on the EU, prepare for delays; they are pausing their trade deal. If you import from China, you just got a temporary discount down to 15%—use it while the window is open, because the administration is already telegraphing new investigations.

- Pricing Action: Stop absorbing the cost. The data shows inflation is rising because smart companies are already passing these taxes on to consumers.

Structural winners

-

-

Domestic “import-competing” manufacturers. U.S. producers that go head‑to‑head with imported goods get an artificial price umbrella: steel and aluminum, autos and parts, basic machinery, and select chemicals all gain relative pricing power as 15% becomes the new floor on most foreign competitors.

-

Strategic “national champions.” Sectors where Washington now has both tariffs and direct equity stakes are clear political winners: semiconductors (Intel, xLight), critical minerals (rare earths, lithium, strategic metals), and nuclear power (Westinghouse) all sit inside the new state‑capitalist safety net.

-

U.S.-centric services and software. Domestic services (healthcare, many financials, HR and business services) and largely digital software platforms face little direct tariff drag but can still pass higher input costs through, making them relative safe harbors.

-

Structural losers

-

-

Import‑heavy consumer and industrials. Retailers and brands relying on imported apparel, electronics, appliances, and auto components see margin pressure and/or demand destruction as the 15% tax is pushed through to final prices.

-

Global supply‑chain plays. Firms built around complex cross‑border supply chains—auto OEMs with heavy Mexico content, electronics assemblers, capital‑goods makers sourcing components from Europe/Asia—wear the volatility and contract risk every time the legal basis for tariffs shifts.

-

Allies who “cut a deal.” UK, Australia and parts of the EU that previously agreed to lower bespoke rates are suddenly reset to 15%, erasing their negotiated edge and inviting retaliation; export‑oriented names in those markets (and U.S. companies tightly coupled to them) are on the wrong side of this reset.

-

Names positioned to benefit

You can call out a few concrete examples for readers:

-

-

Tariff‑sheltered heavy industry and steel. Names like U.S. Steel (now Nippon Steel) and other domestic mill operators sit behind a 15% import wall and, in X’s case, inside a “golden share” structure that aligns them with Washington’s industrial policy.

-

Strategic minerals and rare earths. MP Materials (MP), USA Rare Earth (private/IPO‑path), Trilogy Metals (TMQ), ReElement, and Vulcan Elements are all explicitly backed or optioned by the U.S. government; higher blanket tariffs on foreign inputs plus subsidies tilt the playing field toward this curated domestic mining complex.

-

-

-

Semiconductors and fabs. Intel (INTC) and emerging CHIPS‑backed players like xLight stand to gain from both tariff‑driven localization and direct equity + subsidy support, while export‑linked revenue‑sharing deals on Nvidia and AMD’s China sales effectively tax foreign demand to the government’s benefit rather than Intel’s detriment.

-

Nuclear and firm power. Westinghouse Electric (and partners like Brookfield and Cameco around the big U.S.-backed build‑out) benefit from a protected, subsidized path to long‑cycle projects that are explicitly framed as strategic responses to foreign dependence.

-

In investor language: the new tariff regime plus equity stakes amount to a shadow sector ETF overweight domestic steel, critical minerals, selected semis, and nuclear, and underweight import‑heavy consumer, complex global manufacturers, and allied exporters whose “concessions” just got rug‑pulled.

SINAN: Coherence achieved. The noise says the Supreme Court ended the trade war; the reality is the battlefield has been simply relocated. We advise clients to stop predicting the President’s legal maneuvers and start building resilience against structural volatility.

😎 (Phil) Just when we thought we were getting a handle on things, things change again. Not much to do but watch and wait but, one way or another, Trump needs his $300Bn or his budget is blown to Hell – especially as he keeps claiming it’s $600Bn so $300Bn is closer to $600Bn than zero, right?

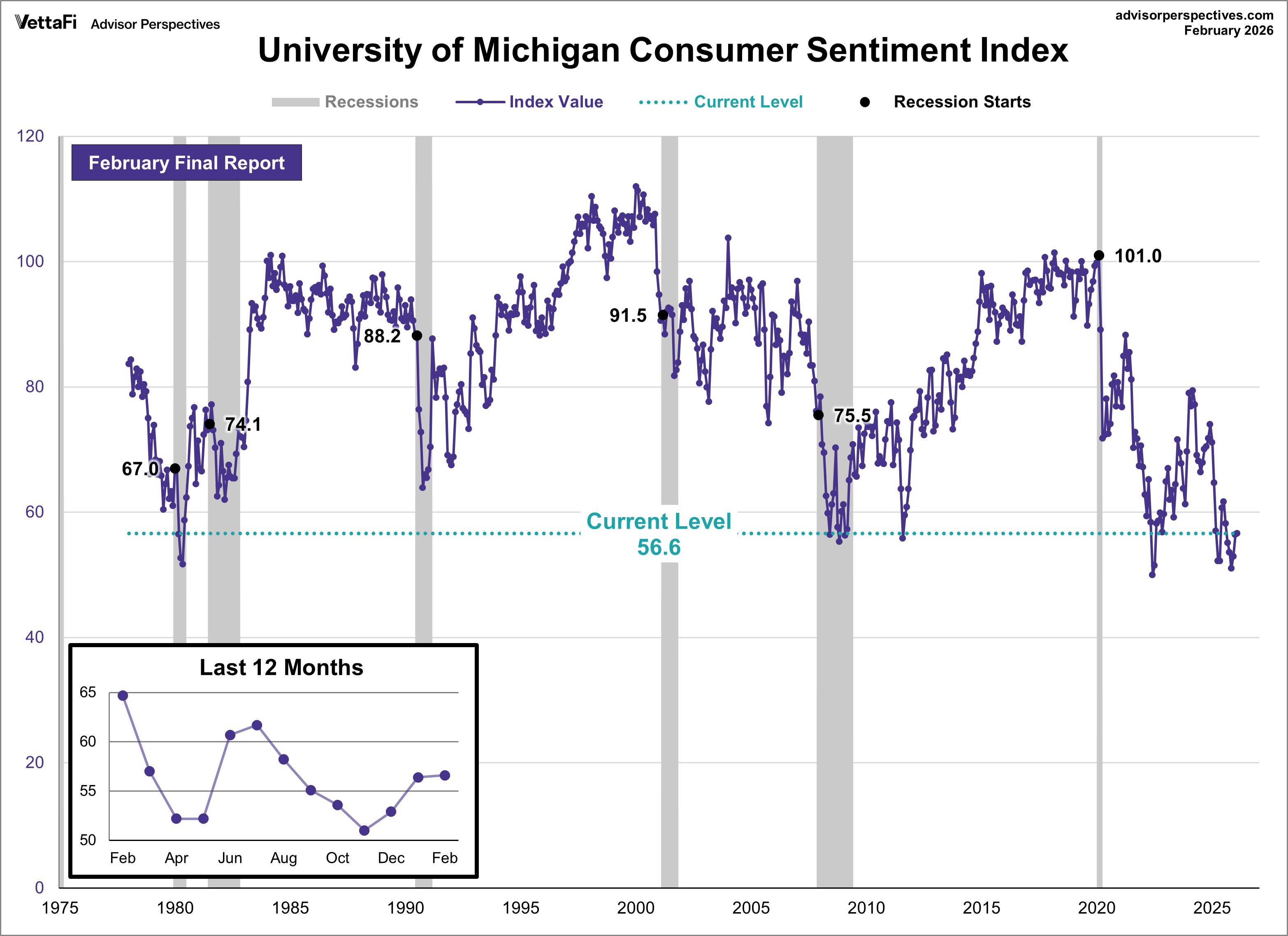

Unfortunately, as proven over and over again in study after study, it’s the American people who are paying these tariffs to the tune of 5% of their total income ($6Tn) and that is why Consumer Sentiment is now as bad as Covid, as bad as the 2008/9 Financial Crisis, WORSE than 9/11, WORSE than the Dot Com crash and as bad as the 1979 Iran Hostage Crisis which, according to Trump, made Jimmy Carter the worst President of all time – yes, this is worse than that, Mr Trump – the only 2-timer in this club:

Perhaps things can only get better from here and we have Feb Consumer Confidence tomorrow but that was also looking kind of scary in January (84.5) so the question is – what would have cheered everyone up since then?

Consumer Sentiment is at deep-recession levels because people feel squeezed and angry; Consumer Confidence is higher because jobs and incomes still look “OK but deteriorating,” not 2009‑style catastrophic. I’d expect tomorrow’s Confidence Report to stay weak and Recessiony, but not collapse to 2009‑type readings unless the Labor Data breaks down.

Sentiment focuses on Personal Finances, Buying Conditions and Long-Term Expectations so food, fuel and politics seer the Sentiment poll. Confidence is more about Business Conditions and the Labor Market and short-term income expectations. Consumer Confidence indexes 100 as the 1985 baseline – so we’re 15% worse off than we were since the last time the Mets won the World Series.

And, keep in mind, by the way, that Consumers are only just getting their increased Health Care bills in the past few weeks – how do you THINK that’s making them feel?

Lots of other data this week as we close out February with Chicago and Dallas Fed Reports this morning and, as usual, a couple of hundred Billion Dollars worth of Treasury auctions because Trump needs money! There’s Housing Data and we’ll see how uncertain Businesses are on Wednesday and Thursday is Durable Goods and Friday is PMI, Construction Spending and Farm Prices and we have 7 scheduled Fed speakers today and tomorrow (mostly tomorrow) but that’s it for the week:

And we’re still getting lots and lots of earnings reports from more and more consumer-facing companies so we’ll see if they are feeling the pinch but nothing matters more than NVDA Wednesday evening as their anticipated $65 BILLION in Revenues is supposed to justify the entire Nasaq – and the S&P – and the Dow.

That’s right, did you know NVDA is a Dow Component? It was added in Nov, 2024, replacing INTC and, at $189 vs $43 for INCT – it has added 1,241 Dow points – just from making the switch!

That’s why the Dow is a completely BS index that should be completely ignored by investors…

Anyway, we’ll see how things go today. The Dollar is down half a point so that should prop up the indexes somewhat and Trump’s deadline for Iran is counting down so that should keep oil ($66.90) and Gold ($5,168) sky high and even Bitcoin is catching a bid $66,097 as people around the World are scrambling for safe havens.

There’s a huge snowstorm shutting down the Northeast so congratulation to all who went long on Natural Gas (/NG) at $3 in our Friday morning call (10:27) to our Members in the Live Chat Room (join us here).

and Promises War Crimes")

{kind=link}