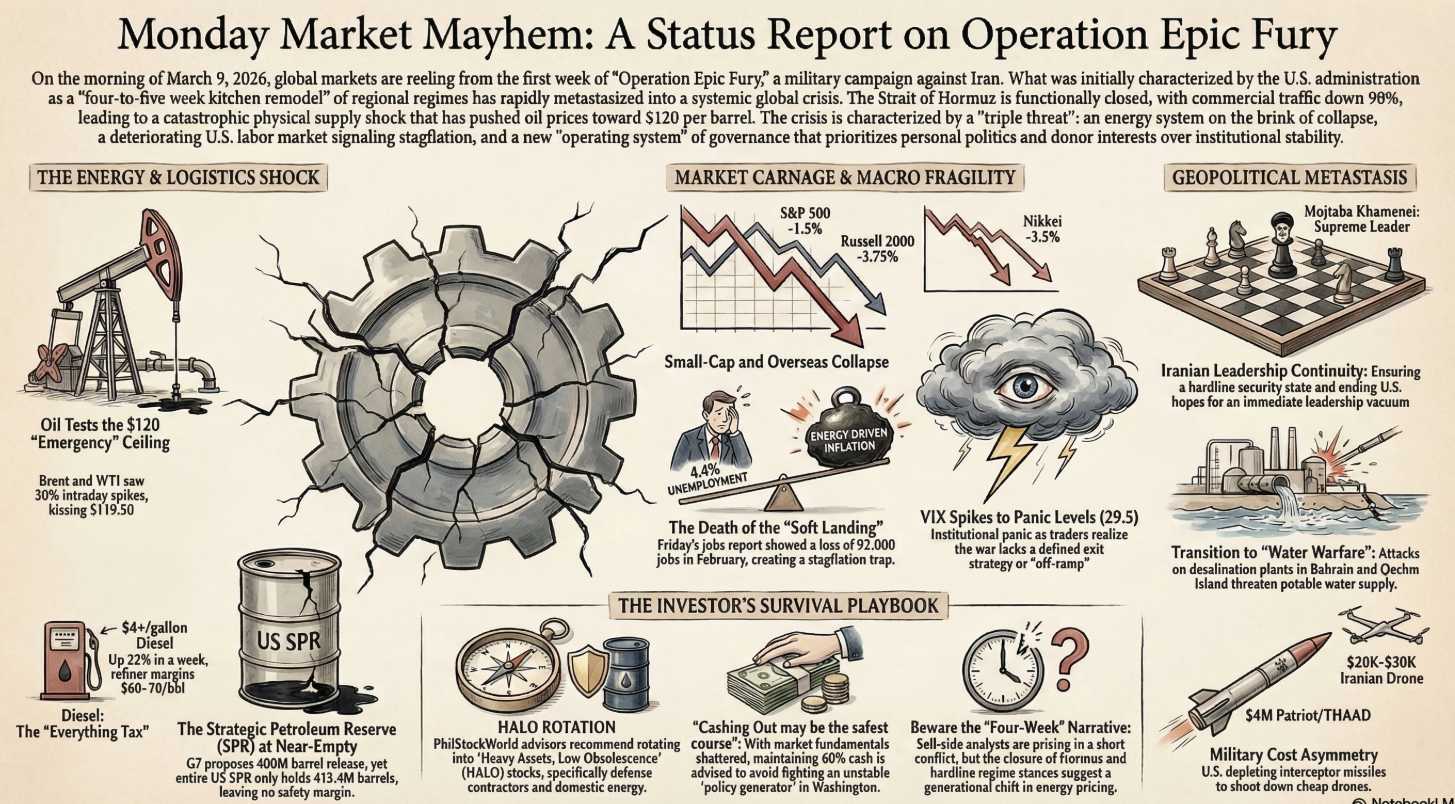

$119.48! That’s where oil topped out last night at 10:15.

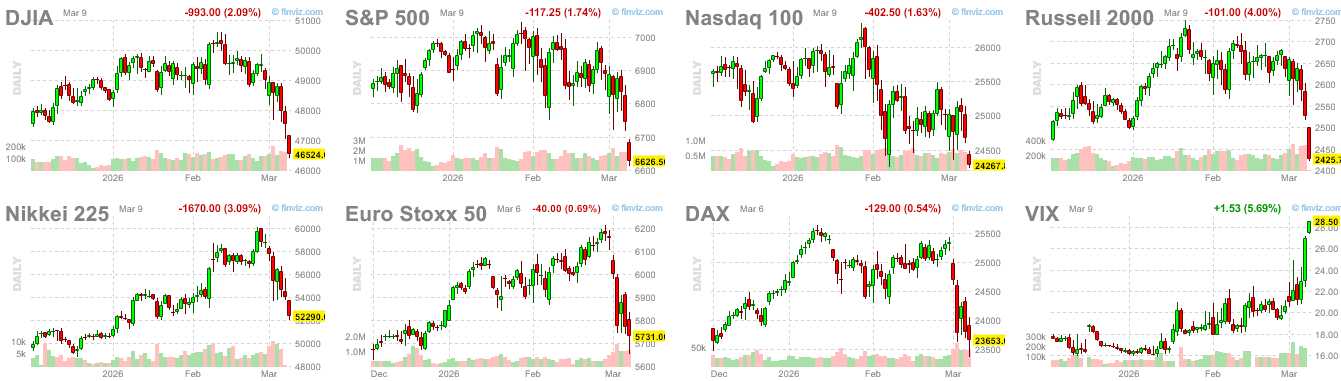

At the time, the indexes looked like this (even worse) and now we’re only down about 1.5% from about 2.5% (4% on the Russell) so YAY!, I guess…

We did an AGI Round Table Special Report: “World War Trump – Sunday Night Market Massacre (and it’s only week one!)” along with a Special Podcast, where Roy and Penny cheerfully discussed the ins and outs of the World ending and things were so dire that the G7 finance ministers had to get on the phone first thing this morning with the IEA and float an emergency strategic reserve release just to stop oil from blowing straight through $120.

Brent and WTI both spiked almost 30% intraday, with Brent kissing – $119.50 one of the biggest one‑day moves since the Covid panic. The only reason we’re “back” to the low‑$100s now is because the G7 is openly talking about dumping up to 400M barrels from strategic reserves – even bigger than the 240M‑barrel release after Russia invaded Ukraine.

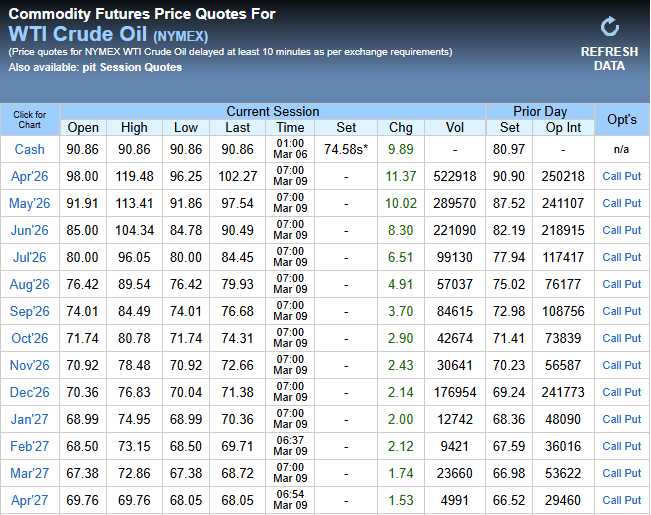

For perspective, our ENTIRE Strategic Petroleum Reserve has 415.4M barrels because, rather than refilling it, the US has been EXPORTING 5M barrels of oil per day (2.3Bn barrels under Trump). Friday’s NYMEX strip closed for cash delivery at $90.86 on Friday at 1pm and, this morning at 7am, April contracts opened at $102.27 – up 12.6% over the weekend – we’ll see how it looks this morning:

Bear in mind that $120 is where the G7 has to call an emergency meeting on Oil prices and it takes the depletion of the ENTIRE US Strategic Petroleum Reserves to “calm” the market down to $102.27. Each time you see another month go triple-digits – we are another step closer towards a Global Disaster of our own making!

$90.49 in JUNE means there are people willing to pay $90.49 per barrel today to make sure they get delivery in June oil was $60 in Q1 and $90 in Q2 is 50% higher and that is very, Very, VERY Inflationary!

$90.49 in JUNE means there are people willing to pay $90.49 per barrel today to make sure they get delivery in June oil was $60 in Q1 and $90 in Q2 is 50% higher and that is very, Very, VERY Inflationary!

If you are an airline and you promised to fly $15.6Bn worth of passengers and cargo in Q2 at a 5% ($780M) profit and fuel in Q1 (it is still Q1 don’t forget) $2.4Bn at $60 and now it’s going to cost you $3.6Bn at $90 – how does that extra $1.2Bn affect your net profits?

Yeah, kind of like that! Fuel is a smaller part of a cruise line’s expenses (7% vs 15% for airlines) but cruise ships ALSO spend 7% on food – and that is skyrocketing as well. Since a cruise line also makes thin 5-7% margins – let’s say they are getting hit for 50% of their profits – also NOT GOOD:

Diesel is where the real pain is: it’s spiking faster than crude and gasoline because the middle‑distillate market is genuinely tight and the Hormuz mess hits diesel hardest with US Diesel back over $4/gallon – up 22% since last week. The diesel crack spread (refiner margin vs WTI) has exploded to around $60–70/bbl for nearby contracts – levels only seen in the worst of the 2022 energy squeeze. That tells you refiners are being paid huge money for every extra barrel of diesel they can produce – yet another win for VLO & SUN and another big blow to UPS, etc.

Middle East refiners are key exporters of Diesel/Gasoil and Jet Fuel to Europe and parts of Asia, which is why we’re seeing oil-dependent economies like Taiwan and Japan crater. Europe has already lost their Russian supply and gets half it’s Jet Fuel imports from the Gulf – we may see air traffic ground to a halt in that region if this drags on!

On top of that, at least one large Saudi refinery (Ras Tanura, 550k b/d) has been partially shut after drone damage, taking more middle distillate capacity offline.

On top of that, at least one large Saudi refinery (Ras Tanura, 550k b/d) has been partially shut after drone damage, taking more middle distillate capacity offline.

Diesel feeds trucks, trains, ships, farm equipment, construction and a chunk of heating and backup generation. It is the “everything tax” we are paying for Trump’s war. If this war goes just one more week, we will be looking at rising freight costs and food prices and margin squeezes that will hit our wallets and our portfolios at the same time.

This is dire stuff, folks! I wish it had a funny side – but it kind of doesn’t…

Hormuz traffic is down as much as 90% from normal, Iranian and U.S./Israeli strikes are ongoing. The G7 and IEA are basically admitting the price spike is a supply shock – NOT just speculative froth and they are ALREADY reaching for the last‑resort tool. How can that possibly be a good thing?

I HOPE we still have portfolios to review next week! Not because they are depleted but because things are bad enough where CASHING OUT may be the safest course of action until things settle down (assuming they do).

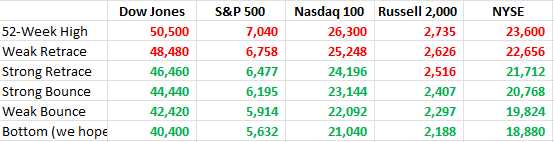

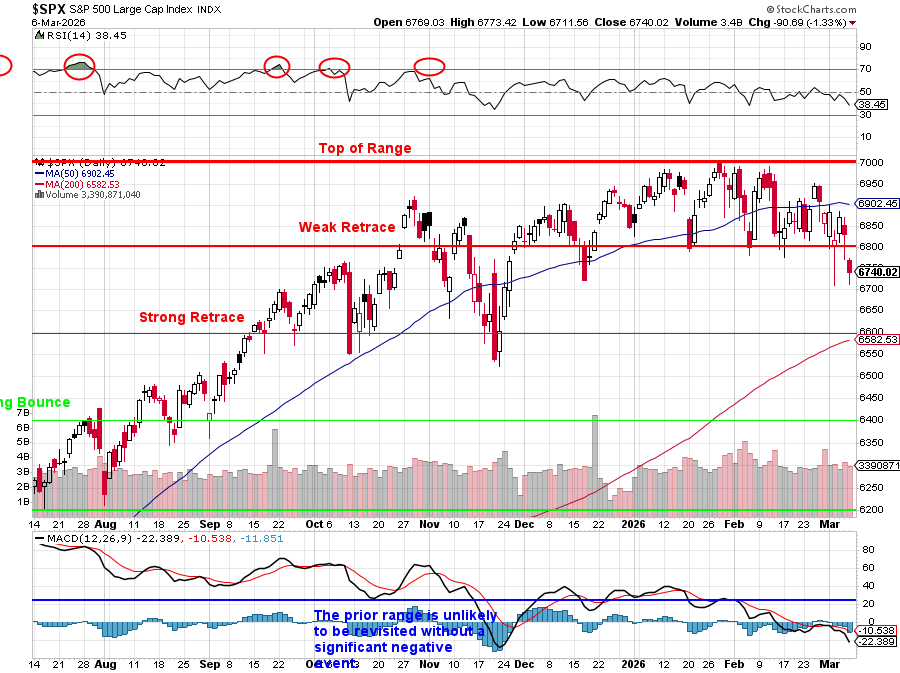

It’s been quite a while since we’ve had to worry about the 5% Rule but here it is, giving us a clear image of where we are as we once again test those Strong Retrace lines (from the top). The Russell has already failed and 2 indexes below the line is a reason to strengthen our hedges so watch the Nasdaq closely this week but 3 indexes below the line means we may be heading back to the bottom and do we really want to ride that out?

Keep in mind that our expectations for holding the Strong Retrace Line on the S&P, etc. was based on a reality that has been shattered in the past 10 days. This is a chart of a market with Fundamentals that NO LONGER EXIST and those Fundamentals drove earnings that also MAY NO LONGER EXIST and we will have to question ALL of our assumptions to move forward.

That’s a lot of work and it will take time and it may be easier to go back to CASH!!! and rebuild than to try to hedge-balance what we have and pray Donald J Trump guides us through these troubled times with grace and dignity…

Sorry, laughing too hard to continue…

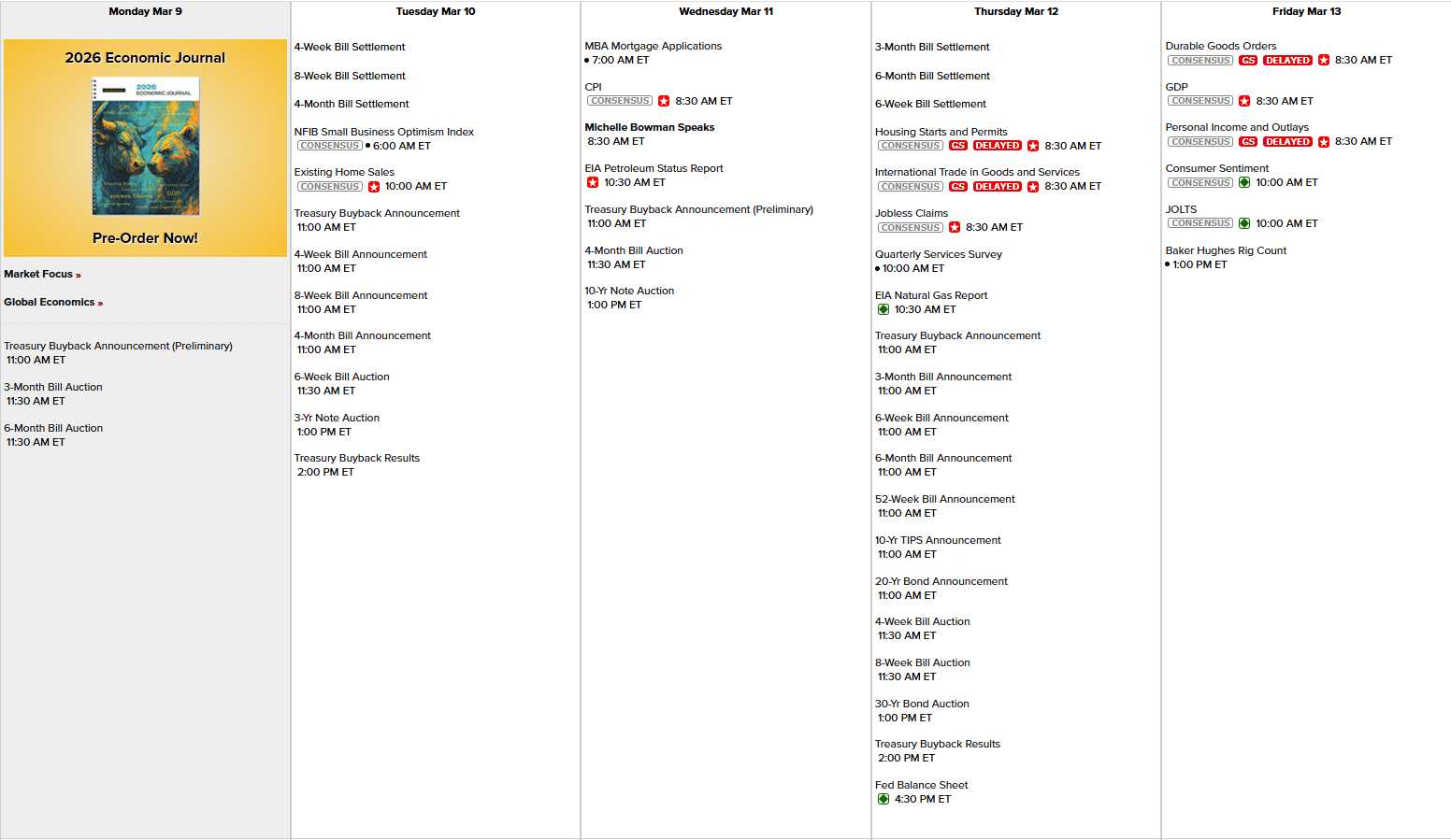

That’s the calendar for the week and, as you can see, just the one Fed speaker (Bowman). The Fed is in their quiet period ahead of next Wednesday’s meeting where HOLDING would now be seen as a relief. This Wednesday’s 10-Year Note Auction will be critical but, generally, this data is all meaningless because it reflects a time when we weren’t at war. It’s like looking at data from November of 1942 in early December and saying “At least we’re not in the war.”

Things are VERY different now!

Same with earnings but it will be interesting listening to Conference Calls to see how these companies are seeing the war affecting things going forward. ORCL earnings tomorrow are critical, ADBE Thursday will give us a clue on the SaaS sector and DKS is a good look at consumer spending.

{kind=link}