To cash out or not to cash out - that is the question?

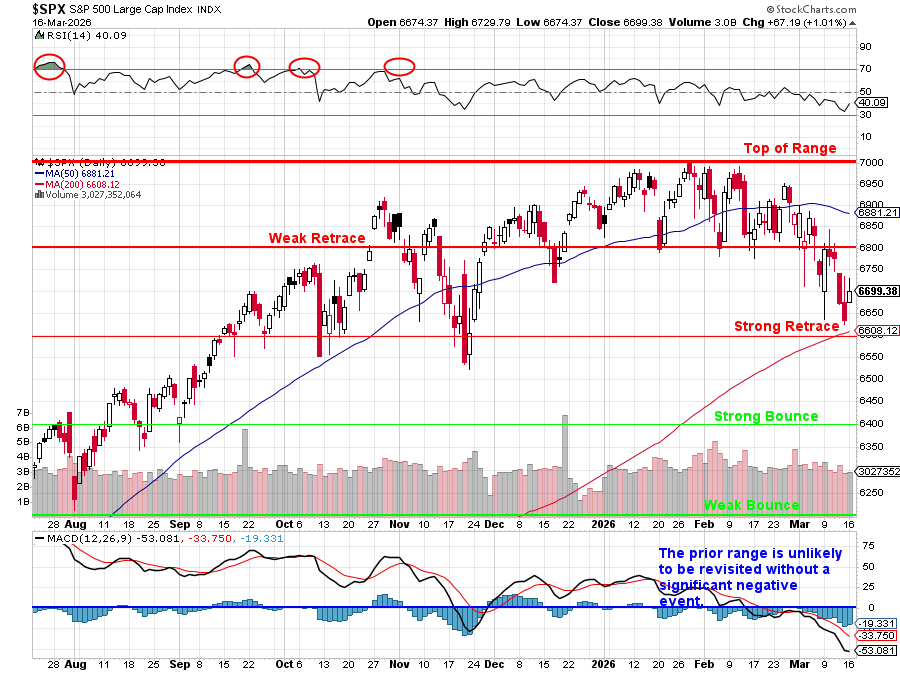

It was exactly a month ago that we did our February Review and, at the time, the S&P 500 was at 6,836 - after testing the top of the range in our January (13th) Review but there's a reason it's called the "Top of Range" and now we're bouncing off the "Strong Retrace" line (6,600) and, so far, the whole thing is a 5% pullback.

The problem is, this isn't a technical pullback based on valuation, this is a pullback based on FUNDAMENTAL changes to the Global Situation as there is now a war, that is costing the US over $1Bn per day (+ lives) and is causing shortages of oil and critical materials that usually ship through the Strait of Hormuz and we don't know when it's going to end - partially because we're not quite sure why it even began.

War is about making choices. We WERE going to spend $1,000Bn on AI Infrastructure but we're diverting $100Bn per quarter to a war that, if we win, gains us nothing (OK, let's say "security"?). But we're driving up the cost of 15M barrels a day consumed in the US by $30 so $450M/day is $40Bn per quarter up in smoke.

Meanwhile, farmers aren't getting fertilizer during spring planting season and that will lead to food shortages and higher prices for what does get grown and there's many more Billions - we spend more on food than gas but food isn't going up 50% (we hope) so let's call that $20Bn down the toilet.

None of these things lead to Productivity Gains (GDP Improvement) - we're just paying more for the same or less than we had before. Even Trump's "excursion" (don't mention the war!

and Promises War Crimes")

{kind=link}