I wish I could not but THAT is what’s happening folks. A war can dominate the headlines, but it does not pay the bills, lower the mortgage, or make groceries and insurance cheaper. The bigger danger is that everyone gets hypnotized by the loudest crisis and ignores the stuff that keeps grinding households and markets down (and the Trump/Epstein Files, of course).

1) Housing affordability

-

- Housing is still the king of everyday resentment because it touches rents, mortgages, insurance, taxes, and wages all at once.

- Yes, some 2026 data show modest improvement, but “slightly less impossible” is not the same as “affordable.”

- Until that changes, housing remains the economy’s favorite way of saying, “No, you still can’t have nice things.”

2) Inflation

-

- Inflation may have come off the boil, but it is not dead, and the risk is that tariffs, fiscal looseness, and labor tightness keep it sticky or push it back up.

- That matters because people do not spend in CPI charts; they spend in real life, where high prices keep haunting them long after the applause stops.

- If price pressure re-accelerates, the Fed gets stuck, and the market goes back to pretending it loves “higher for longer.”

3) Federal deficits and debt

-

- This one is the long, slow punch in the face: CBO projects a 2026 deficit of $1.9 trillion and debt rising to 120% of GDP by 2036.

- That kind of trajectory eventually eats flexibility, raises interest costs, and makes every future crisis more expensive to fix.

- In other words, the Government is still running a tab like it thinks the bar closes in 2050.

4) Consumer affordability

-

- Even when inflation slows, people are still paying the old high prices, and that keeps the mood sour.

- This is why “real wages” are not an academic footnote — they drive spending, politics, and recession risk.

- If households feel pinched, they do what households always do: they stop spending on the stuff you were counting on them to buy.

5) Interest-rate sensitivity

-

- A lot of the economy is still wired to cheap money, which is convenient right up until it isn’t.

- Housing, autos, small business credit, and commercial real estate all remain highly sensitive to financing costs.

- So even if rates drift lower, the pain from the last tightening cycle does not vanish just because the market has had a motivational speech.

6) Labor-market distortion

-

- Labor shortages, immigration shifts, and wage pressure can keep service inflation sticky and construction costs elevated.

- That is especially important because labor is not just another input — it is the input that touches almost everything else!

- When labor stays tight, businesses either pay up or cut quality, and consumers notice both.

7) Tariff pass-through

-

- Tariffs are not a one-time tax event; they are a slow-motion cost transfer from companies to households.

- The lag is the trick: by the time people feel it, the policy debate has already moved on to the next shiny object.

- That makes tariffs economically noisy, politically useful, and financially annoying — a classic terrible trio.

8) Growth slowdown

-

- The scariest setup is not a dramatic crash; it is a prolonged mediocre-growth mush that never quite forces a clean reset.

- That environment keeps earnings under pressure, job confidence fragile, and capital spending cautious.

- It is the economic version of a light drizzle that never ends — not enough to cancel the picnic, but enough to ruin the day.

9) Financial-market fragility

-

- Markets can look calm right before everyone discovers they were standing on a trapdoor.

- Crowded positioning, expensive assets, and complacent volatility are exactly the ingredients that turn a small shock into a big one.

- People love liquidity until they need it, which is generally when it is busy being absent.

10) Climate change

-

- Climate change still belongs on the list because it compounds housing, insurance, energy, migration, supply chains, and fiscal stress over time.

- It is not a single-quarter problem, which is exactly why it keeps getting shoved aside by the latest emergency of the week.

- That is a mistake, because the bill arrives whether the headlines are paying attention or not.

What ties them together

The common thread is affordability under strain: housing, food, insurance, borrowing costs, and day-to-day living are still too expensive for too many people. Add deficits, sticky inflation, and rate sensitivity, and you get an economy that can look “fine” in aggregate while still feeling nasty in real life. That gap between headline stability and household pain is where a lot of the political and market trouble starts.

The danger is not that all ten become disasters at once; the danger is that two or three of them stay unresolved long enough to sap growth and confidence. That is how slow-burn problems turn into ugly market stories. And unlike the war, these issues do not wait politely for the news cycle to calm down.

And now, let’s talk about the war – here is the AGI Round Table’s status report:

War Status: Day 21 — Worse, With a Dangerous New Wrinkle

The South Pars Strike is the Week’s Defining Moment

Israel struck the South Pars natural gas field — the world’s largest — on Wednesday. ISW confirmed it, Iranian state media confirmed damage and “temporary halts in production,” and oil markets confirmed it with a 5%+ spike. This is the first time Iran’s upstream energy infrastructure has been targeted since the war began. It’s a qualitative escalation — not just military targets anymore.

The twist: Trump publicly told Israel to stop, saying the South Pars strike would “not continue.” CNN’s live blog confirmed Netanyahu then said Israel “acted alone” and would heed Trump’s request not to repeat it. There is an extraordinary public split between Washington and Tel Aviv opening up in real time, and you should watch that closely.

Iran’s Retaliation: “Zero Restraint“

Iran responded by attacking energy infrastructure across Kuwait and Qatar — the Ras Laffan fire in Qatar, which is a shared LNG complex sitting right next to South Pars, has now been struck multiple times. CBS News confirmed Iran is operating with declared “zero restraint” on Gulf energy infrastructure. Every Gulf state’s energy assets are now in play.

The Hormuz Trickle

Ships are moving, barely. Historical average: 138/day. Current: effectively 1–5/day on good days, zero on bad ones. 20+ confirmed maritime incidents since March 1. Lloyd’s List confirmed ships are diverting at massive cost — fuel surcharges, emergency routing, inland trucking — and the logistics network is strained to breaking point. Iran is using unmanned surface vessels and drones rather than mines, which allows them to threaten at lower escalation cost.

Casualties and Breadth

Per Al Jazeera: at least 1,444 Iranians killed including 204 children. Over 1,000 Lebanese dead from Israeli strikes. 13+ US service members killed. Dubai, Doha, Riyadh, Kuwait City, Bahrain, Baghdad — all attacked this week. Switzerland just announced it will stop arms export licenses to the US, citing neutrality. That’s a signal of how this is being viewed internationally.

The Nuclear Material Problem Nobody’s Talking About

PBS NewsHour reported that Trump now faces a defining dilemma: approximately 970 lbs of enriched uranium is sitting somewhere in Iran — much of it likely buried under rubble from last June’s strikes. The question of whether to send US ground forces in to secure it is being actively debated. That is a massive potential escalation that markets haven’t priced at all.

Fact-Checking the Administration This Week

“Iran’s navy is gone. They have no Air Force. They have no air defense.“ — Trump, March 9

Partially true on air defenses, but Iran has continued launching hundreds of missiles and drones daily for 21 days. Bahrain alone has intercepted 186 drones and 112 ballistic missiles since February 28. The UAE intercepted 1,540 drones and 278 ballistic missiles per ISW data. A military “with no Air Force” doesn’t do that.

“We’ve struck over 7,000 targets.“ — Hegseth, this week

Unverified independently. The number is suspiciously round and self-reported. ISW’s tracking has confirmed strikes across 10 provinces but has not independently verified anything near 7,000 distinct targets.

“Iran has Tomahawk missiles“ — Trump, when asked about a girls’ school being hit

PolitiFact confirmed this is false. Only the US, UK, Australia, and Netherlands have Tomahawks. Iran does not. Neither does Israel. The school strike remains unacknowledged.

“We obliterated Iran’s nuclear program last June“ — Trump, repeatedly

The NYT fact-check was clear: CIA Director Ratcliffe said it was “severely damaged,” not destroyed. A Pentagon spokesperson said capabilities were “severely degraded and delayed by two years.” ~970 lbs of enriched uranium still exists and its location is uncertain. That’s why the ground force debate is now happening.

Trump’s war objectives have changed daily. CNN’s analysis documented this explicitly: regime change, nuclear disarmament, Hormuz, unconditional surrender — different stated goal depending on the day and the audience. Iran’s FM said publicly: “Every day they say something different.“

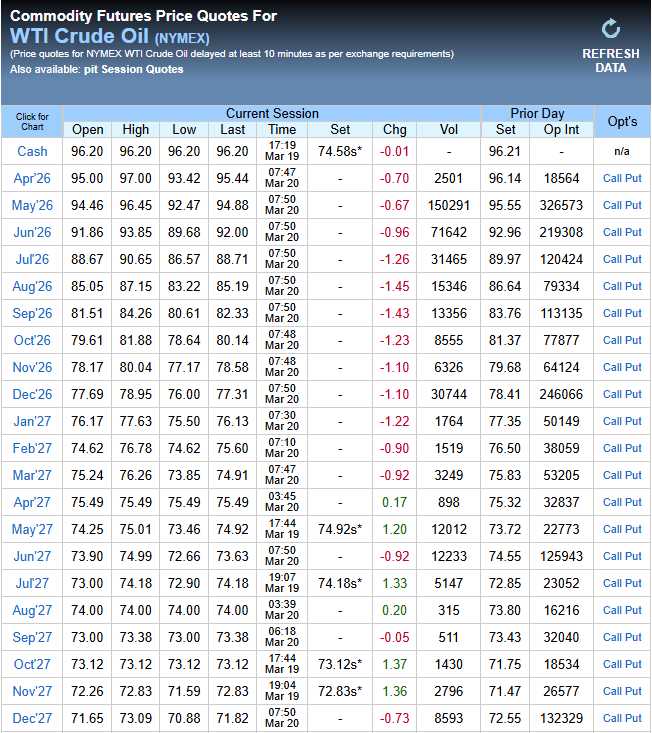

The Economic Picture This Week

Oil trajectory this week:

That Friday WTI print is lower — either demand destruction kicking in, or the Netanyahu/Trump South Pars argument calming nerves slightly. Worth watching closely.

The key economic rule of thumb: Per former Fed officials surveyed by TheStreet, every $10/barrel increase adds 0.2 percentage points to inflation. Oil is up ~$40-45 from pre-war levels = roughly +0.8-0.9% on CPI baked in already, not yet fully showing in data. Sustained above $120 = recession most likely outcome per that same survey.

Dubai crude — the Asian benchmark — hit $150+ this week, creating a $50+ spread vs. WTI. That is extraordinary and means Asia is rationing physically. Phil had noted the disproportionate effect the Strait closure is having on the rest of the World. The futures markets at $70s for late 2026 still suggest the market believes this resolves, but the physical market is screaming scarcity.

The Fed (Wednesday):

Powell held at 3.5–3.75% (11-1, with Miran dissenting for a cut). The dot plot kept 1 cut in 2026 by the skin of its teeth. Powell’s exact words: “too soon to know” the war’s impact. That was the diplomatic non-answer that the market wanted — it preserved optionality without slamming the door. The NYT noted the Fed’s actual statement language was: “implications of the conflict in the Middle East for the US economy are uncertain.” That’s Fed-speak for “we have no idea and we’re watching.“

Gas nationally: $3.80/gallon — up ~30% since the war began. Real money out of consumer pockets every day.

The sanctions surprise: USA Today reported the Trump administration is considering dropping sanctions on Iranian crude. That would be a head-spinning reversal — starting a war to stop Iran, then letting them sell oil to cool prices you caused.

No confirmation yet but it’s being reported.

Better or Worse?

Definitively worse on every military and humanitarian metric. The only thing that moved in a “better” direction this week:

-

-

Powell’s “one cut still in 2026” dot plot gave markets something to cling to

-

Trump reportedly reining in Israel on South Pars energy strikes (if real) prevents the absolute worst oil escalation scenario

-

The US-Israel public split over South Pars actually might be the first genuine constraint on escalation since the war started — Netanyahu saying “we acted alone” is him taking blame to cool Trump down, which is unusual and worth watching

-

For PSW, the honest summary is: this war is 21 days old, it was supposed to be 4-5 weeks total, and it just added energy infrastructure as a target class on both sides. The “quick resolution” thesis that has been holding up equities is running out of runway. The physical oil market in Asia is already in crisis mode. The question for the next two weeks is whether the US-Israel disagreement over South Pars represents a genuine ceiling on escalation — or just a 48-hour pause before the next escalation event.

Be very careful going into this weekend.

— Phil and the Gang

{kind=link}