Idea: Add Barclays (BCS) to the LTP as a discounted, capital‑return story with real operating momentum, not a “turnaround hope.”

Thesis: You’re buying a UK/US universal bank that just raised its profit targets, committed to large buybacks, and is trading around 0.7x tangible book and <9x forward earnings.ainvest+2

Why now

-

-

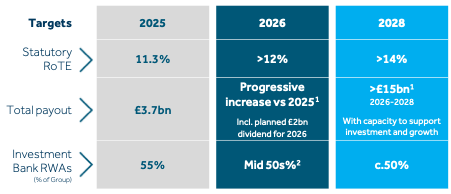

Earnings power is already there. 2025 pretax profit was about £9.1B, up 12% year‑on‑year, roughly in line with or ahead of analyst expectations.reuters+1

-

Targets just moved higher. Management lifted its return on tangible equity goal to >14% by 2028, from 12%+ by 2026 previously, with a 5%+ revenue CAGR target.sharecast+1

-

-

-

Capital return is serious, not cosmetic. Barclays has launched a £1B buyback for 2025, and laid out a plan to return £15B to shareholders between 2026‑2028, on top of prior commitments. At today’s valuation, that’s a material slice of the market cap being retired.investing+4

-

Why it’s cheap

-

-

BCS still trades at roughly 0.7x tangible book and ~0.8x book, versus a historical range closer to 0.9–1.0x when the story is in better standing.gurufocus+1

-

Forward P/E is under 9x despite double‑digit profit growth and a rising RoTE trajectory.[ainvest]

-

The discount reflects Euro‑bank PTSD, UK macro noise, and generic “banks are scary” sentiment, not a broken balance sheet.

-

Structural positives

-

Core focus: US + UK. Management is explicitly concentrating on higher‑return core markets (US and UK) and leaning on AI and digital to take out costs. That’s a cleaner story than trying to be everywhere.rte+2

-

US consumer banking build‑out. The planned acquisition of Best Egg, a leading U.S. personal‑loan originator, expands capital‑light consumer fee income beyond co‑branded cards. It’s a disciplined deal (high‑single‑digit P/E on 2026 earnings), not a late‑cycle fintech splurge.

")

")

")

")

{kind=link}