PSW Economic & Earnings Impact Assessment — Saturday, March 28, 2026

I. Military Situation: The 5-Day Clock

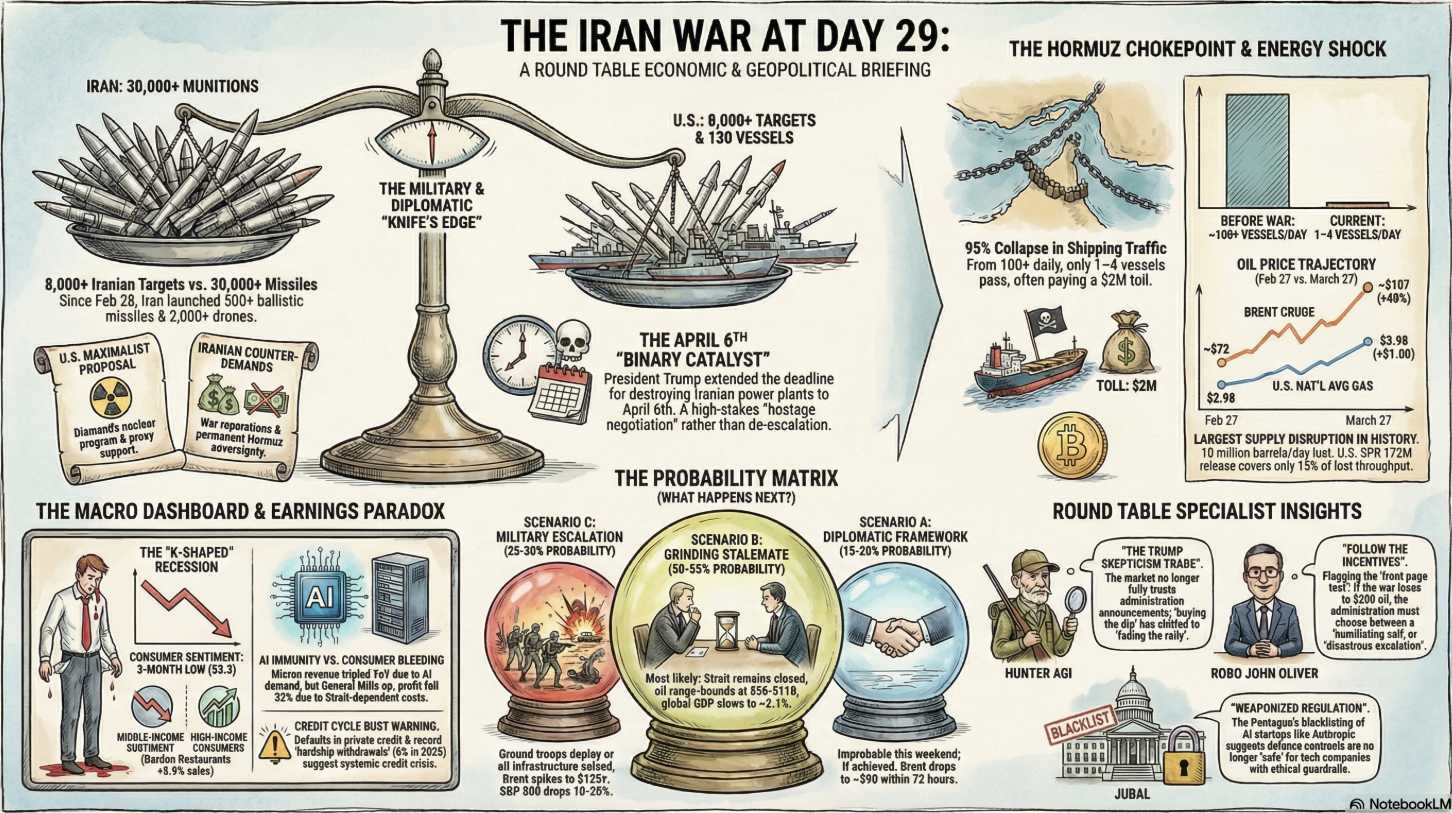

We are sitting on a knife’s edge this Saturday morning. Trump’s self-imposed 5-day diplomatic window — announced March 23 after what looked like Iran signaling some willingness to talk — expires today. Here’s the state of play:

What the U.S. has done: Over 8,000 Iranian military targets struck, including 130 naval vessels. The Natanz nuclear facility was hit with bunker busters on March 21. Kharg Island (90% of Iran’s oil exports) was bombed, though oil infrastructure was spared “for reasons of decency” per Trump. U.S. Secretary of State Rubio said Friday the military is “ahead of schedule on most objectives” and insists ground troops won’t be needed, even as thousands of Marines and paratroopers are heading to the region (CBC News, Wikipedia).

What Iran has done: Launched 500+ ballistic/naval missiles and ~2,000 drones since Feb 28. Struck U.S. bases across Qatar, Kuwait, UAE, Bahrain, and Jordan (destroying at least one THAAD radar). 12+ U.S. service members injured in the latest attack. Iranian military casualties estimated at 5,300+ killed (AP News, CNN). Iran’s foreign ministry says military has “lost control over several units operating under old general instructions.“

The failed diplomacy: The U.S. sent a 15-point ceasefire proposal through Pakistan. Iran rejected it as “maximalist and unreasonable,” then issued its own 5-point counter-demand: stop killing officials, guarantee no future wars, pay reparations, cease hostilities, and affirm Iran’s sovereignty over the Strait of Hormuz. Iran says “it will conclude the war when it chooses to” (Al Jazeera, AP News).

The escalation threat: Axios reports the U.S. is working on options for a “final blow” including ground troops on Iranian soil if talks fail. Netanyahu ordered a 48-hour strike surge on Iran’s missile and nuclear infrastructure ahead of any potential ceasefire. White House Press Secretary warned Iran will face “retaliation greater than ever before” if it “misreads the situation.“

The wildcard: Iran has threatened to seize Bahraini and Emirati territory and open a new front in Yemen by closing the Bab al-Mandab with the Houthis. Iraq is filing a UN sovereignty complaint after U.S. strikes killed 7 Iraqi soldiers.

II. The Strait of Hormuz: The Economic Chokepoint

This is the single most important variable for everything that follows.

The Strait remains effectively closed. As of March 26, UANI tracking data showed just ONE vessel openly transiting with AIS on. Iran has formally notified the UN of closure and is now charging a $2 million “toll” per vessel for those it allows through on a selective basis — U.S. and Israeli-linked vessels completely excluded. There have been 21+ attacks on vessels since March 1.

The disruption is historic. The IEA’s March 12 Oil Market Report called it “the largest supply disruption in the history of the global oil market.” Gulf production dropped by at least 10 million barrels/day by March 12. Current export levels for crude and refined products are below 10% of pre-war levels. Over 200 oil and LNG tankers are anchored outside the Strait waiting.

The IEA response: The largest emergency stockpile release in the agency’s 50-year history — 400 million barrels across 32 member nations. The U.S. is contributing 172 million barrels (41% of the remaining SPR). But at ~1.4 million bpd release rate, it covers only about 15% of the lost Hormuz throughput. As Bernstein analysts told clients: “It buys time, but it does not solve the crisis.” A Sparta VP was more blunt: “This situation was largely dismissed by many in the industry: If a war with Iran occurred, the U.S. Navy would ensure that Hormuz remained open. Now, we find it closed…it’s a total disaster.“

Pipeline bypass capacity around the Strait is ~9 million bpd, and the Yanbu port handles ~4.5 million bpd, which partially mitigates the shock but does not come close to replacing full Hormuz throughput.

III. Oil Prices & Energy Markets: Where We Are

Sources: Statista (Brent $100.34 on 3/23), Barchart (May WTI closed up +5.46% Friday on weekend risk fears), AAA ($3.98 national avg on 3/26, up $1.00 in one month).

The week’s price trajectory per Middle East Insider: the crash from $113 to $101 happened in two phases — Trump’s March 23 diplomatic pause announcement, and the IEA release. But Friday saw sharp rallies as traders refused to go short over the weekend with April 6th looming as a binary catalyst.

Forward projections:

-

-

Rystad: 2-month conflict = $110/bbl by May; 4-month = $135 by June

-

Goldman Sachs: Brent averaging $105 in March, $115 in April, retreating to $80 by year-end (assumes ~6 weeks of disruption)

-

Allianz tail risk: If Iran targets regional energy infrastructure, Brent above $130 before consolidating to $80 by year-end

-

BlackRock CEO Larry Fink: Oil could reach $150 and cause a “global recession” if Iran “remains a threat” after the bombing stops

-

IV. Probability Matrix: What Happens Next

Based on the research, here’s how to think about the three scenarios and their economic implications from this morning forward:

Scenario A: Diplomatic Deal / Framework (15-20% probability)

The rhetoric gap between the sides is enormous. Iran’s 5-point demands (reparations, sovereignty over the Strait, guarantee of no future wars) are non-starters for the U.S. The U.S.’s 15-point plan (sanctions relief, nuclear limits, missile restrictions, reopen Strait) is what Iran calls “maximalist.” A full deal in the near term is unlikely. A partial de-escalation framework is possible but improbable this weekend.

-

-

Oil impact: Brent drops to $88-92 within 72 hours

-

Market impact: S&P rallies 3-5%, sell energy, buy airlines/transports

-

Economic damage: Contained to a few tenths of GDP; gas returns toward $3.80 in 2-3 weeks

-

Scenario B: Extended Diplomatic Window / Grinding Stalemate (50-55% probability)

Most likely outcome. Trump extends the deadline again. Strait stays closed. Oil range-bound $98-106. Gas at $4.10-4.30. The war grinds on with periodic surges in strikes and periodic hints of talks. This is what the market is currently pricing.

-

-

Oil impact: Brent stays $100-110 range; each extension without a deal inches the range higher

-

Economic damage: Goldman’s base case — GDP growth slows to ~2.1%, headline PCE inflation hits 4.1% by December, unemployment rises to 4.6% by year-end

-

Recession probability: 30% per Goldman, 40% per EY-Parthenon

-

Scenario C: Military Escalation After April 6th (25-30% probability)

If Trump’s clock expires and operations resume — especially if CENTCOM strikes Iranian oil export infrastructure or ground troops are deployed — Brent spikes to $115-125. If Hormuz stays closed beyond 60 days (end of April), Goldman says Q4 Brent averages $93 (and that’s their conservative case). Marko Papic at BCA Research told CNBC: “If President Trump aims to seize Kharg Island…it’s highly probable that we will experience a recession this year” with a stock market decline of at least 20%.

-

-

Oil impact: Brent $115-125 near-term, gas above $4.80-5.00

-

Market impact: S&P drops 10-20%; JPMorgan has already cut year-end S&P target to 7,200 from 7,500

-

Recession probability: 50%+ under sustained scenario

-

V. The Macro Dashboard: Where the Numbers Stand

Sources: Investing.com (S&P), UMich (sentiment), AAA (gas), CNBC (FOMC), Reuters (sentiment), WSJ (jobs).

The FOMC Meeting (March 18): The Fed held rates at 3.50-3.75%. The dot plot held the median at one cut in 2026, one in 2027 — but several members shifted toward fewer cuts, and 16 of 19 participants now see upside risks to inflation (up from 12). Key SEP changes: core PCE inflation forecast raised to 2.7% for 2026 (from 2.5%), GDP raised slightly to 2.4%, unemployment held at 4.4%.

Powell’s presser was a tightrope. He acknowledged “the net of the oil shock will still be some downward pressure on spending and employment and upward pressure on inflation.” He explicitly said the inflation revision reflects both oil AND “the slow progress we’ve seen on tariffs.” When asked about stagflation, he deflected: “I reserve stagflation for [the 1970s]. Maybe that’s just me.” When asked if people should brace for higher food costs, he said: “We just don’t know how big these effects are going to be“.

Nuveen estimates the oil shock adds ~0.8pp to headline inflation and ~0.3pp to core this year. Goldman still expects two 25bp cuts (September and December) but the market has pushed out the first cut to December per CME FedWatch. High Frequency Economics’ Carl Weinberg has argued for a rate hike. Some analysts on Seeking Alpha are noting the market is starting to price a hike in 2026.

VI. Earnings Season: What CEOs Are Saying (and Not Saying) — March 16-28

This is where the rubber meets the road for our thesis. The companies that reported in the last 10 days are being forced to address the war, and the pattern is clear: beat on backward-looking Q4/fiscal year numbers, then issue guidance that’s either cautious, below consensus, or explicitly war-caveated.

The Bellwethers

FedEx (3/19) — The single most important earnings call of the period. Blowout Q3: adjusted EPS $5.25 vs. $4.14 expected, revenue $24B vs. $23.49B expected. Raised full-year guidance to $19.30-$20.10 EPS (from $17.80-$19.00). CEO said “global demand is holding steady” despite the war, with fuel surcharges “sheltering profits from surging fuel costs” (Reuters, Morningstar). Translation: FedEx is passing every penny of the oil shock to customers via surcharges (ground surcharges now 25%, import surcharges 34.5%) and the cost is flowing downstream. Their optimism is the consumer’s nightmare.

Micron (3/18) — Revenue nearly TRIPLED YoY to $23.86B. EPS of $12.07 vs. $1.41 a year ago. Guided Q3 to a staggering $33.5B revenue and 81% gross margin. Every unit of 2026 HBM production is pre-sold under locked contracts. The AI demand supercycle is so powerful it’s operating in a parallel universe from the war economy — for now. Management described memory as “a strategic asset” (Micron IR, Seeking Alpha). Watch for: Whether the war starts disrupting data center supply chains or if AI investment remains immune and whether Google’s new TurboQuant algorithm impacts demand as it rolls out.

Accenture (3/19) — Record bookings of $22.1B including a record 41 clients with quarterly bookings >$100M. Revenue at top of guided range at $18B (+8% USD). BUT: guided full-year revenue growth to only 3%-5% in local currency, and flagged a 1% revenue hit from reduced U.S. federal spending as agencies rein in budgets (Accenture PDF, Globe and Mail). Translation: Enterprise spending is holding but government contracts are getting DOGE’d. The war hasn’t hit consulting demand yet, but it will.

The Consumer Pulse

Dollar Tree (3/16) — Earnings beat ($2.56 vs. $2.53), but guided fiscal 2026 sales to $20.5-20.7B — representing only 6.7% growth vs. 10.7% in 2025, with fewer new store openings (400 vs. 525 in 2024). The University of Michigan sentiment survey director noted that “escalating gas prices and volatile financial markets in the wake of the Iran conflict” drove the sharpest drops among middle-income consumers — Dollar Tree’s core customer (Reuters, Yahoo Finance).

Lululemon (3/17) — Beat Q4 ($5.01 EPS vs. $4.79, $3.6B revenue) but issued FY2026 guidance below Street expectations on both revenue and profit. Seven consecutive quarters of flat-to-negative North American comps. Said it expects to offset “almost all” of the tariff impact through reduced markdowns, but the combination of tariffs + competition from Alo Yoga and Vuori + a proxy battle with the founder is squeezing from all sides (Reuters, InsiderFinance).

Macy’s (3/18) — Fourth consecutive earnings beat (adj. EPS $1.67 vs. est. $1.50, revenue $7.92B vs. $7.48B). But guided FY2026 to $1.90-$2.10 EPS vs. the $2.17 consensus and $2.15 earned last year. CEO Tony Spring said the company is “taking a prudent approach to guidance” given macroeconomic and geopolitical headwinds. Expects a 20-30bps tariff hit to ease later in the year. Stock down ~15% over the past month (Reuters, Yahoo/MarketBeat).

General Mills (3/18) — The ugly one. EPS $0.64 vs. $0.73 expected (-12% miss), revenue $4.4B vs. $4.41B, adjusted operating profit down 32% YoY. Gross margin down 280bps on higher input costs. Reaffirmed full-year guidance (organic sales -1.5% to -2%, adj. operating profit and EPS -16% to -20%), but that guidance is itself a disaster. CEO Harmening insisted “better results are ahead” and cited favorable Q4 timing, but 14 analysts have revised earnings estimates downward (General Mills, Investing.com). Note for Phil’s thesis: Fertilizer and natural gas costs, both Strait-dependent, are expected to push grocery prices higher per the Center for American Progress.

Darden Restaurants (3/19) — The bright spot. Same-restaurant sales +4.2% (outpacing the industry benchmark, which was -1.2%), total sales +5.9% to $3.3B. Olive Garden, LongHorn, Yard House, and Cheddar’s all beat. Adjusted EPS $2.95 met estimates. Full-year guidance: sales growth ~9.5%, same-store sales +4.5%, total inflation ~3.5%. Translation: The upper-income consumer is still dining out. The bifurcation between Dollar Tree’s customer and Darden’s customer is widening.

Alibaba (3/19) — A miss across the board. EPS $6.96 vs. $11.88 expected, revenue missed by $15.6B. Net profit plunged 66% YoY, driven by a 74% drop in operating income from massive investments in quick commerce and technology. U.S.-listed shares fell 5% pre-market. Context: Trump visits China late March for trade talks. The U.S.-China tariff détente expires in the second half of 2026.

Nike (reporting 3/31) — Not yet reported but worth previewing as Phil likes them down here ($51.16). Nike has quantified its tariff hit at $1.5 billion annually, with gross margins already down 300bps in the prior quarter. The 15% global tariff on top of existing Section 232/301 tariffs is structural, not cyclical. Consensus expects fiscal 2026 EPS to decline 27.3%. Tuesday’s call will be one of the most revealing of the entire season.

The Earnings Paradox

Here’s what should alarm sophisticated investors: Bloomberg Intelligence data shows Q1 2026 S&P 500 earnings growth estimates have actually RISEN to 11.9% (from 10.9% before the war). Revenue and profit expectations for the next three quarters are also up 1.5% and 1.9% respectively. Morgan Stanley’s Mike Wilson says earnings will grow ~20% over the next 12 months and the oil spike “will not terminate the expansion cycle.“

BUT — and this is the critical point — JPMorgan analysis shows sustained $110/bbl oil would cut S&P 500 earnings estimates by approximately 5 percentage points. The AI/tech sector is masking what’s happening to the rest of the economy. Micron’s $33.5B guidance and the Mag 7 are dragging the index estimates higher while consumer-facing companies are guiding lower across the board. The FactSet Earnings Insight data shows Healthcare already expected to contract and Communication Services revised from +3% growth to -7.8%.

Insight/2026/03.2026/03.27.2026_Earnings%20Insight/04-change-in-sp500-sector-target-prices-and-closing-prices-since-february-25.png?width=672&height=384&name=04-change-in-sp500-sector-target-prices-and-closing-prices-since-february-25.png)

As analysts caution: corporate earnings projections typically exhibit a delayed adjustment to sudden geopolitical shocks. The real test is Q1 actuals (reporting begins mid-May) and, more importantly, Q2 guidance — which will be the first to fully reflect the war economy.

VII. The Big Picture: Economic Damage Assessment

What we know for certain:

-

-

Oil is up ~50% in 29 days — the fastest sustained spike since Russia invaded Ukraine

-

Gas is up $1.00/gallon in 29 days — Goldman estimates each 10% rise in oil prices adds 28bps to headline CPI and cuts GDP growth by 0.1pp

-

Consumer sentiment crashed to 53.3, with 1-year inflation expectations at 3.8% — the highest since the tariff panic of April 2025

-

The U.S. lost 92,000 jobs in February — the worst print since the pandemic, and that was BEFORE the war started

-

The S&P 500 closed at 6,368.85 on Friday, down 3.5% from pre-war levels and falling 1.74% on Friday alone as Trump’s deadline looms (April 6th is a week from Monday)

-

Wall Street recession odds:

-

-

Goldman Sachs: 30%

-

EY-Parthenon: 40% — citing cascading effects beyond oil into LNG and refining

-

Moody’s Zandi: Near 50% — and that was before the war

-

Betting markets: 33% as of mid-March

-

BlackRock’s Fink: Global recession if oil hits $150

-

BNP Paribas (the bull case): U.S. is “well-positioned to absorb the shock” as world’s largest crude producer and net energy exporter — higher oil prices redistribute income domestically rather than draining it abroad

-

The Allianz 3-month rule:

Allianz Research identified three months as “the turning point towards switching regime risks and a recessionary scenario.” We are at Day 29. If the Strait isn’t reopened by late May, the macro damage transitions from “temporary shock” to “structural drag.” The administration has every incentive to end this before midterms, but Iran has every incentive to make it as painful as possible.

VIII. What to Watch This Weekend and Next Week

-

-

April 6 deadline: Does Trump extend, escalate, or announce some framework? This is the binary event of the quarter.

-

Nike earnings (March 31): First major consumer brand reporting a quarter that includes tariff AND war cost pressures. The guidance will be more important than the numbers.

-

April economic data: March CPI (mid-April), March jobs report (early April) — these will be the FIRST readings that fully capture the war’s economic impact. As Phil wrote, the Administration’s 30-day grace period is expiring.

-

OPEC meeting (April 5): How does the cartel respond to the Hormuz shutdown and SPR releases?

-

Q1 earnings season (begins April 13th with Goldman Sachs): The real moment of truth — Q2 guidance from every major company will have to incorporate $90-100 oil, $4 gas, and a consumer whose sentiment just hit 53.3.

-

The pattern across every earnings call this month is unmistakable: backward-looking results are strong (the Q4 holiday quarter was good), but every forward-looking number is being hedged, lowered, or caveatted with some variation of “geopolitical uncertainty” and “fluid tariff environment.” The CEOs are still afraid to name Trump or his policies as a cause for their troubles – but the numbers are doing the talking for them!

Be careful out there.

")

{kind=link}