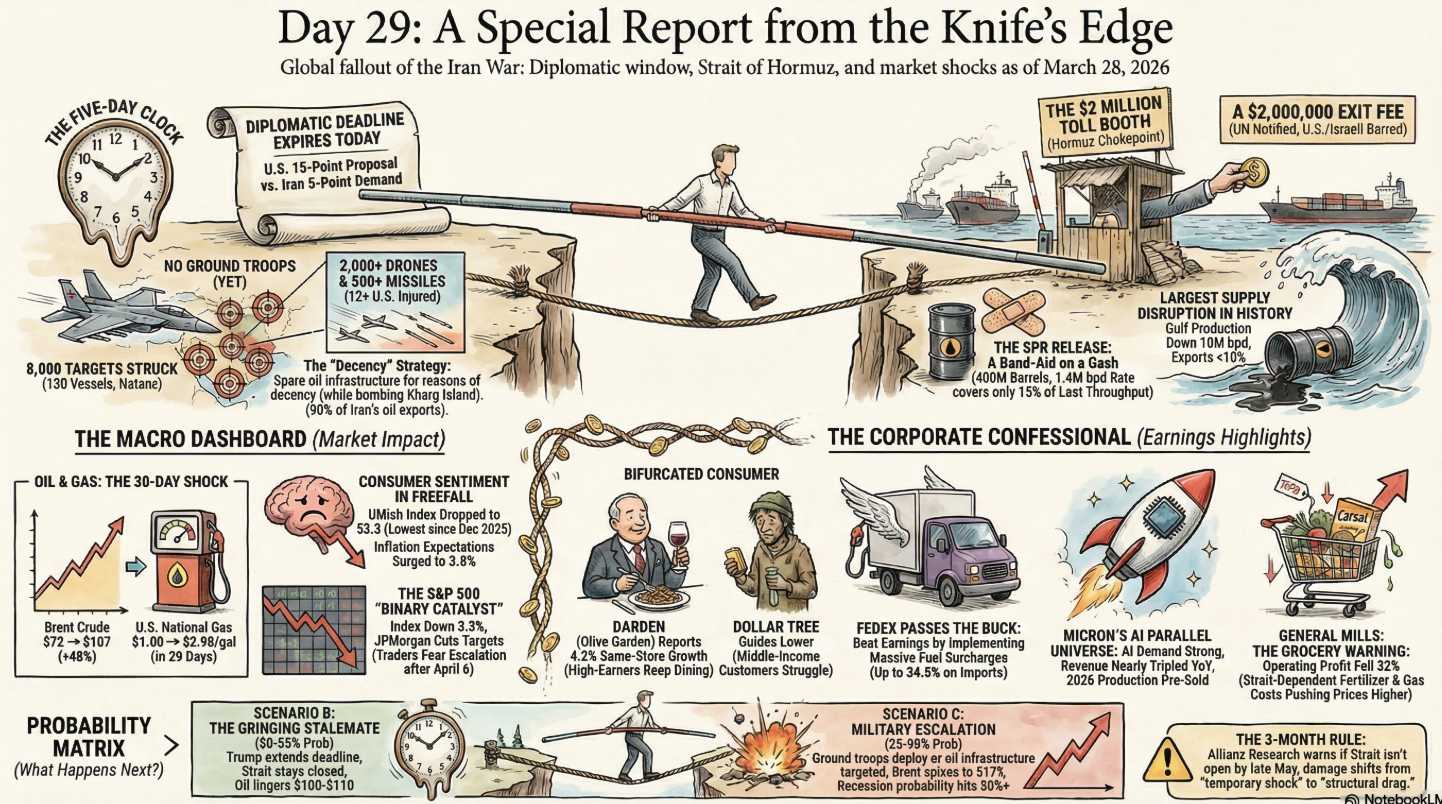

Welcome to Day 31 of Operation Epic Fury, which is running roughly 3-4 weeks longer than the administration said it would already.

Welcome to Day 31 of Operation Epic Fury, which is running roughly 3-4 weeks longer than the administration said it would already.

The war that was more recently going to be “4 to 5 weeks, maybe less” has now crossed into its second month with the Strait still closed, 50,000 US troops in theater, and Trump apparently telling the Financial Times over the weekend that his “preference would be to take the oil” and that US forces could seize Kharg Island — Iran’s main oil export terminal. The man who gave Iran a 10-day extension for 10 tankers is now publicly musing about occupying their oil infrastructure.

These two positions are, of course, NOT compatible, but consistency has not been a feature of this conflict.

🧠 What Happened Over the Weekend

It was not a quiet weekend. Buckle up:

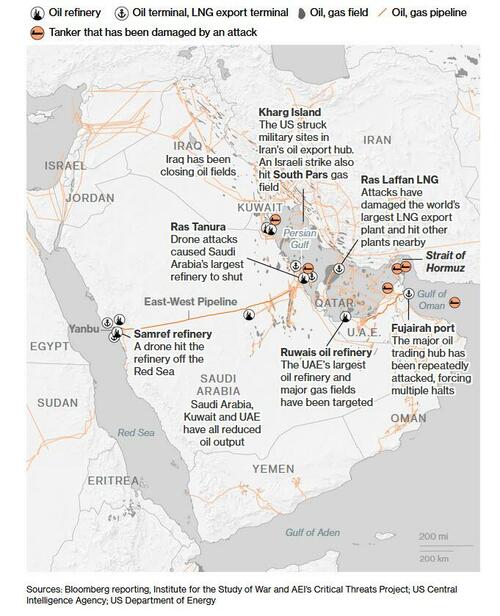

The Houthis rejoined the fight. After staying out of the conflict since February 28, Yemen’s Houthi rebels fired two ballistic missiles at Israel on Saturday per Al Jazeera. This matters enormously — the Houthis spent 2024 paralyzing Red Sea shipping. Their return means a potential two-front maritime chokepoint problem: Hormuz and Bab el-Mandeb simultaneously. The Red Sea WAS just starting to recover. Now it’s back in play.

Tehran lost power. Strikes hit electrical infrastructure Sunday, cutting power to parts of Tehran and Alborz province. It was restored within an hour, but Fortune confirmed the power grid is now being targeted — despite Trump’s “pause” on power plant strikes. The pause applies to US strikes. Israel, as always, does what Israel does.

The IAEA confirmed Iran’s Khondab heavy water plant sustained severe damage. Fortune reported the IAEA made this determination Sunday. Heavy water is used in plutonium production — one of the original stated war objectives. This is genuine progress on the nuclear goal, but it’s not stopping anything else.

Iran hit Prince Sultan Air Base again. NYT confirmed two KC-135 aerial refueling tankers sustained considerable damage and 12 Americans were injured. That’s the same base that was hit earlier in the war. Iran is deliberately targeting US military assets in Saudi Arabia repeatedly — testing whether Saudi Arabia will eventually kick the US out, which would be a strategic catastrophe.

Iran threatened US universities in the region. The IRGC warned all faculty and students to stay at least one kilometer from US-affiliated campus grounds in the Middle East. This is a new category of target threat that nobody needed.

The Pentagon is preparing a ground invasion. Washington Post reported the Defense Department is planning “weeks of ground operations” — not a full invasion, but special forces and conventional troops targeting strategic sites, with Kharg Island specifically cited as a likely first objective. 3,500 Marines arrived aboard the USS Tripoli over the weekend, joining the ~50,000 US troops already in theater. Iran’s response: any American ground forces will be “destroyed.”

Total confirmed dead: 4,500+. Per Fortune: roughly three-quarters in Iran, 1,200+ in Lebanon, dozens in Israel and Gulf states, 13 US troops.

The Diplomacy: Still Alive, Still Toothless

Pakistan, Turkey, Egypt, and Saudi Arabia foreign ministers convened in Islamabad over the weekend. They’re talking. Iran is still publicly rejecting any direct talks while privately relaying messages. The April 6 (one week!) deadline ticks. The gap between the two sides’ positions — Iran wants reparations and Hormuz sovereignty; the US wants zero enrichment and proxy group disbandment — hasn’t closed by a millimeter.

NPR noted that Israel is intensifying strikes specifically to hit as much arms manufacturing as possible before any ceasefire locks those targets in. The country whose military actions would need to stop for any deal to hold is racing to make the war as irreversible as possible before diplomacy succeeds.

One genuinely interesting detail: Iran’s Parliament Speaker Ghalibaf — the man who is apparently the lead Iranian negotiator while publicly denying he’s negotiating — issued a threat this morning that the US must condemn the bombing of Iranian universities by noon today or US university campuses in the region become targets. A 12pm deadline on a Monday morning. Trump is going to love setting that one against his April 6 deadline.

Oil and Markets: Monday Morning

WTI: ~$102 (up 2.4% per Trading Economics), Brent: ~$112+. Oil surged over the weekend on the Houthi news, the ground invasion reports, and the sheer exhaustion of anyone still believing in a quick resolution.

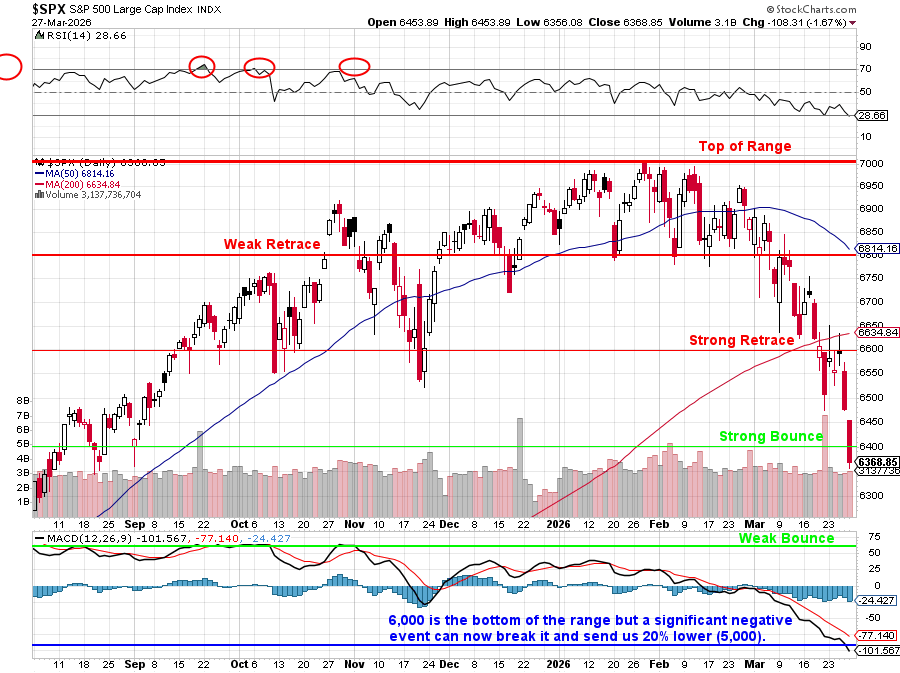

Friday’s close was ugly: Nasdaq officially entered correction territory, down 10.7% from its peak. The Dow joined it in correction. The S&P 500 — the last major holdout — is teetering. The Russell 2000 is already deep in correction. This is now a broad market deterioration, not a sector-specific move.

TheStreet notes futures are actually edging higher this morning — a holiday-shortened week (Good Friday market close) with positioning thin and short-covering likely. Don’t mistake light-volume Monday morning futures gains for conviction. Powell is speaking this morning at 10:30 and the Futures are higher (1%) in hopes he says something doveish.

The Morningstar/MarketWatch summary from Sunday night nailed the sentiment: “investors are waking up to the reality that the economic effects of the Iran war are likely to last longer than first expected.” That’s the entire story in one sentence. The market spent four weeks pricing in a quick resolution. It is now, reluctantly and painfully, beginning to price in the alternative.

Notice the RSI on the SPX has fallen to 28.66 – indicating short-term oversold and primed for a bounce – which pre-market traders are taking advantage of to drive the indexes higher on no actual positive news.

The Week Ahead: What to Watch

April 6 is the hard date. Trump’s extended pause on power plant strikes expires Monday evening next week. By then either: (a) some form of in-person talks have happened in Islamabad and there’s a framework to point to, or (b) Trump bombs power plants and the war enters a genuinely new and darker phase, or (c) TACO #4.

The ground invasion timeline is the new wild card. The Washington Post’s reporting wasn’t a leak — it was almost certainly deliberate signaling to Iran that the military option has escalated from “air campaign” to “boots on the ground at Kharg Island.” Whether that moves Tehran or hardens them further is the $104/barrel question.

Economic data this week: Consumer confidence and the March jobs report land Friday — except markets are closed Friday for Good Friday, so Thursday becomes the last trading day of the month. Expect the jobs data to show the first real war-impact signals on hiring and confidence. Goldman’s recession probability at 30% and unemployment forecast at 4.6% are going to get tested against real numbers this week.

One month in. Still no deal. Still no ships. Still escalating on every front. The “4 to 5 weeks” is up — and the only thing that changed is there are now 50,000 US troops in the Middle East and a Marine battalion floating toward Kharg Island.

See also our special weekend AGI Round Table Report: The Iran War at Day 29 – Where We Stand (if we had legs!)

😎 It’s a short week (closed Good Friday) but we’re still getting some earnings reports including Nike (NKE), who we think are getting stupidly oversold at $51. Our Long-Term Portfolio position on them is down about $10,000 and we WILL spend some money to improve the position if we need to after earnings – unless they say something truly horrific – we’re happy to give them a couple of years to turn things around.

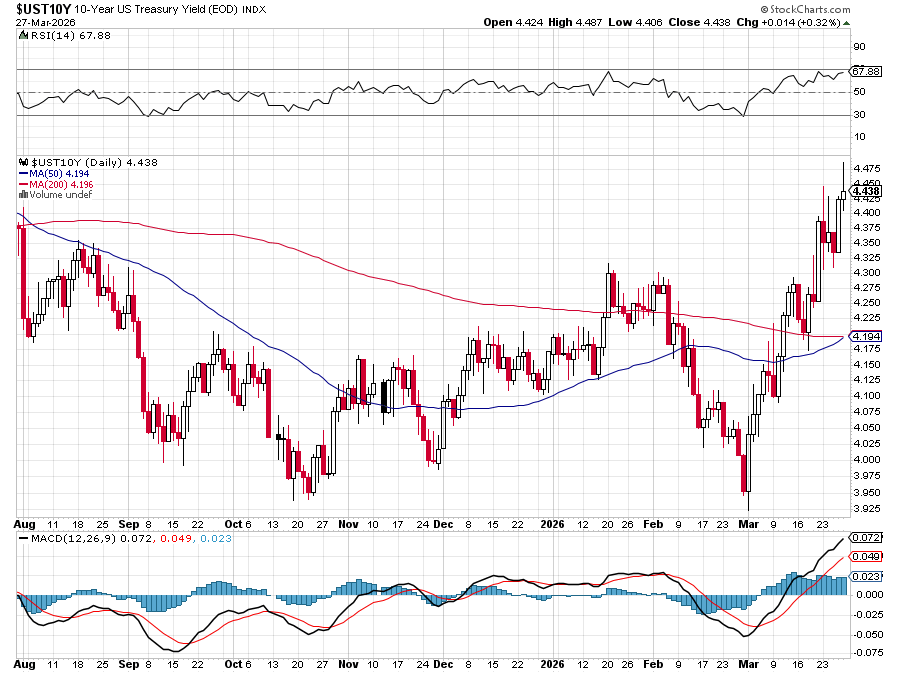

On the data front, Powell needs to calm things down this morning as the 10-Year Rate races to 4.5% – 0.5% higher than before the war began and this week we have some short-term auctions ahead of next week’s long-term auctions with the US looking to borrow 400 BILLION additional Dollars in April and 0.5% is $2Bn in additional annual interest alone!

That is this month’s borrowings alone and it all compounds quickly as our $40Tn debt rolls over at 0.5% higher ends up being $200Bn PER YEAR of additional interest payments PLUS the $200Bn cost of the war (requested by the DOD) is TWICE as much as ALL the tariff revenues and 8 TIMES MORE than all the combined DOGE cuts – for this idiocy!

There are 9 other Fed speakers scheduled this short week to push those bond sales and we get the Dallas Fed this morning and Farm Prices (rising!) in the Afternoon. Tomorrow is Home Prices, Chicago PMI, Consumer Confidence (ouch!) and JOLTS. Wednesday we get Retail Sales, PMI, ISM and Business Inventories and Non-Farm Payrolls are scheduled for Friday still – when the markets are closed – which seems weird…

There are 9 other Fed speakers scheduled this short week to push those bond sales and we get the Dallas Fed this morning and Farm Prices (rising!) in the Afternoon. Tomorrow is Home Prices, Chicago PMI, Consumer Confidence (ouch!) and JOLTS. Wednesday we get Retail Sales, PMI, ISM and Business Inventories and Non-Farm Payrolls are scheduled for Friday still – when the markets are closed – which seems weird…

The bounce chart is all red (the bottoms are gimme’s) and this morning’s open won’t even cover a weak (dead cat) bounce as we’re near a 10% bounce across the board so 2% would be a weak bounce – not 1%…

| Dow Jones | S&P 500 | Nasdaq 100 | Russell 2,000 | NYSE | |

| Feb High | 50,500 | 7,040 | 26,300 | 2,735 | 23,600 |

| Weak Retrace | 49,410 | 6,904 | 25,659 | 2,673 | 23,180 |

| Strong Retrace | 48,321 | 6,768 | 25,017 | 2,610 | 22,760 |

| Strong Bounce | 47,231 | 6,632 | 24,376 | 2,548 | 22,340 |

| Weak Bounce | 46,142 | 6,496 | 23,734 | 2,485 | 21,920 |

| March Low | 45,052 | 6,360 | 23,093 | 2,423 | 21,500 |

Be careful out there!

{kind=link}