We’re back baby!

Just yesterday, we were failing the Strong Bounce Lines on our Bounce Chart and suddenly we’re back at the Strong Retrace Lines (still concerning) because Trump put off his genocidal threats for two weeks – Nobel Peace Prizes for everyone!!! Well, certainly for Pakistan…

Will it last? Who knows, but let’s enjoy it while we can! Oil dropped almost 20% last night, from $115 to $94.53 with Brent crude falling to $93.91 – still below WTIC. Gasoline is back to $2.97 and Natural Gas is $2.72 and that happened without a single ship actually moving through the Gulf!

We did a special podcast last night covering the peace outbreak.

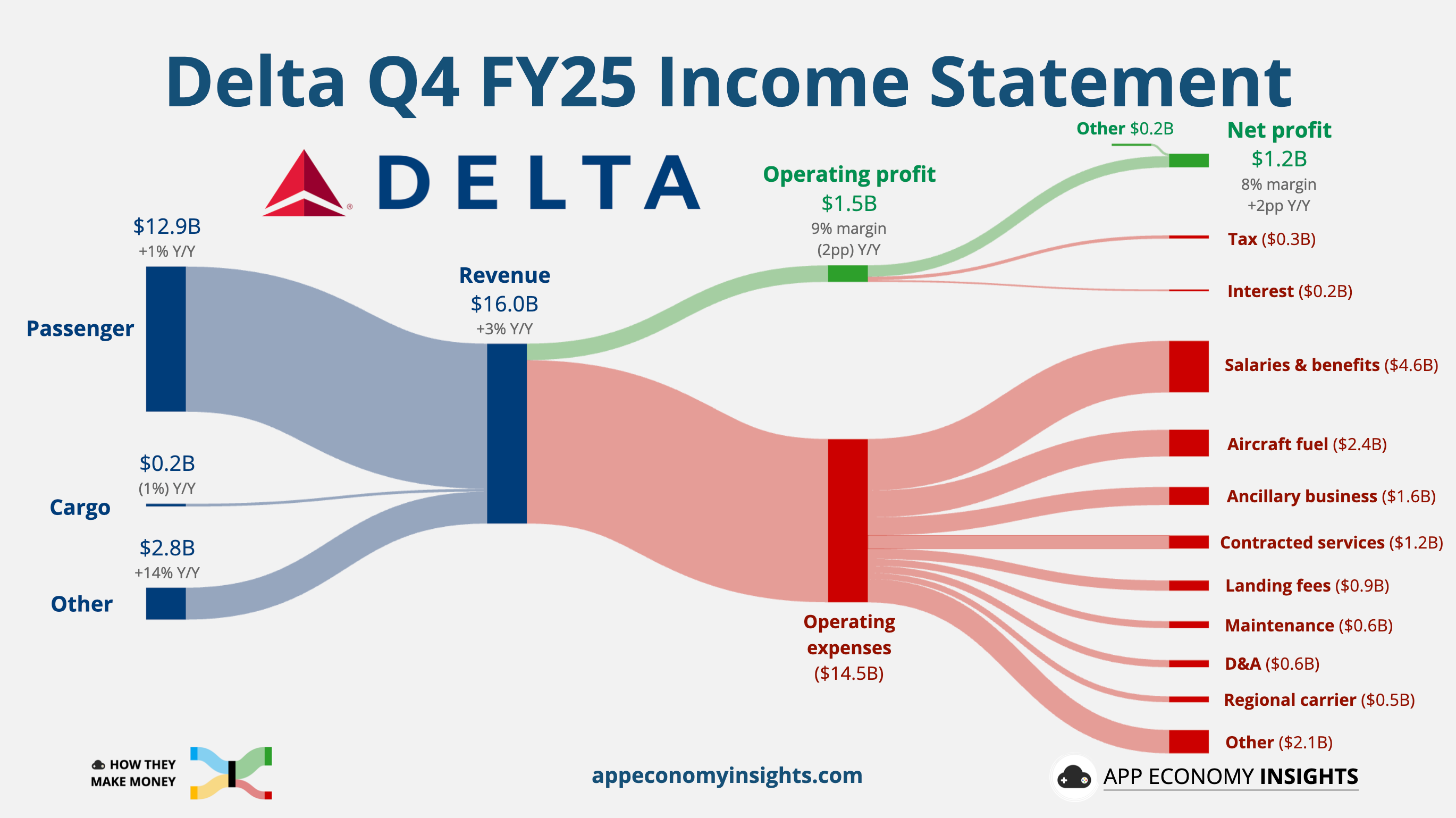

That’s right, EXPECTATIONS are everything – facts will have to catch up later. Oil is still 50% higher than the start of the war but that’s better than 90% so – YAY!!! – I guess… Delta Airline took a $2,000,000,000 hit on fuel costs in Q1 and, although that’s just the amount of our money Trump pissed away daily on his war – it’s still a lot of money to some people – especially an airline that only expected to earn $3.6Bn this year.

Nonetheless, that is “better than feared” and Delta is popping 11% this morning in anticipation of nothing else going wrong ever again and, of course, the ability to make it all back by raising baggage fees and charging you an extra $50 if you want to avoid sitting in the middle seat.

That was last Quarter so this Q might be -$800M but Delta still thinks they can make $7 per $73.60 share – so under 10x earnings despite the war is very impressive and we’ll see how the other airlines do as their earnings come in.

In fact, if earnings season proves resilient DESPITE the 40-day war – then they shall be all the more impressive looking forward. Inflation also inflates earnings and the Dollar is back to 98.60 this morning – down 1.5% from yesterday and that’s a large part of what’s boosting the indexes 2.5% this morning but, shhhhhh! – we’re trying to have a moment here…

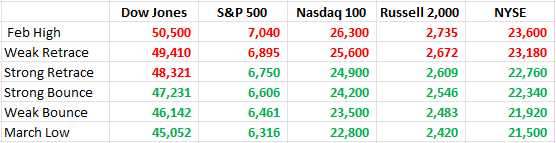

The S&P is down just 4.4% for the year – after being down about 8% for a day last week and that thin, blue line on top is the Dollar – and you can see how it has a very direct short-term correlation to the index – like the one it’s having this morning. Will it last is the great question that needs to be answered.

There are certainly still PLENTY of stocks that are on sale. Microsoft (MSFT), for example, is down 20% for the year and AMZN and META are down 8% and TSAL is down 16% (we just cashed in our shorts on Thursday!). WMT, COST, KO and PEP were safety stocks and XOM and CVX are up over 20% – will they now sell off? Interesting times are ahead and there will be no lack of opportunities to deploy our CASH!!!

IBM is down 17%, CRM down 28% in the SaaSapocalypse – is that still on? INTU is down 35% – did that have ANYTHING to do with the war? It will be fun sorting all this nonsense out – won’t it?

The whiplash in Oil and the Airlines is the same story in micro. Brent going from $115 to the low‑$90s in a night didn’t magically undo a 40‑day war; it just shifted expectations from “unlimited Iran spiral” to “maybe we can live with $90 instead of $130,” which turns Delta’s extra $2B in fuel from an existential crisis to “painful but survivable.”

If Q1 earnings come in merely flat to slightly up with GDPNow limping along near 1.3% and a 40‑day war in the rear‑view, the market will happily file that under “better than feared” and start repricing for 2027 again. Even though, under the hood, the cost of capital is still high, the consumer is slowing and the only thing that really changed this week was the tone of a press conference and the level of the Dollar – which is the measuring stick for the market.

We have a two-week window of continued uncertainty – maybe less if things start blowing up again but, for now, let’s enjoy the peace!

– Oil Hits $115 (again)")

{kind=link}