Courtesy of Charles Hugh Smith, Of Two Minds

Now that oil is an increasingly speculative play, we can expect wide swings in price and increasing volatility.

The reasons for oil to keep rising are well known–perhaps too well known.Let’s look at some charts to illustrate the swirling currents in the global oil market. Why do we care? Two reasons: the price of oil is approaching the "push economies into recession" level, and anyone who lives in an industrialized economy or who needs grain or energy from overseas to live will be directly impacted by the cost and availability of oil.

Both open interest and volume have risen significantly since 2006, suggesting oil is increasingly a speculative play, both long and short.

An unprecedented gap has opened between commercial long and short positions, suggesting some major punters are positioned to profit if oil falls.

Oil and gasoline are on a see-saw with the U.S. dollar. When the dollar rises (as measured by the DXY Dollar Index) then oil declines; when the dollar loses value, oil rises. If the dollar reverses its decline, then oil (if history is any guide) will fall (at least when priced in dollars).

The majority of proven reserves are in the Mideast, a region currently experiencing social unrest. That’s a polite phrase for incipient revolutions. It might all boil down to "meet the new boss, same as the old boss," but in the interim any disruption in supply would impact supply-demand and potential push prices much higher.

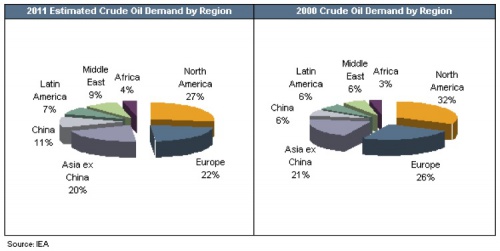

Note the increase in demand from the oil-exporting Mideast (less for you, importing nations) and Asia and the relative decline of North America and Europe.Lots of competition for those precious barrels available for export.

Meanwhile, back on the ranch, Americans have less disposable income. Costs for food, property taxes, tuition and healthcare are rising dramatically even as official inflation is low. As oil/gasoline creeps higher, then the American household has less money available to blow at the mall or the fast-food outlet.

That’s how you get a recession: higher costs for essentials and reduced consumer spending. Nothing dampens "animal spirits" like an empty gas tank and an empty pocketbook.

What’s in play is not just supply and demand, but the premium in the price of oil resulting from the rising speculation as traders and fund managers seek out commodity and global growth plays with all that "free money" that’s sluicing out of the Federal Reserve.

With oil swinging from around $50 per barrel in 2007 to $145 a barrel in 2008 and then plummeting to $32 a barrel in 2009, this increase in speculative trading has led to increased volatility. And that leads to an obvious question: could oil slump sharply, despite all the reasons typically given for higher prices, purely as a function of the speculative trade?

Massive increases in speculation don’t guarantee endless Bull markets: highly leveraged speculative trades can quickly reverse course when sentiment changes. Rising volume and speculative interest increase volatility as extremes of sentiment are reflected in large positions being taken on the long (Bullish) or short (Bearish) side.

Notice that both volume and open interest rose sharply from 2006. Since then, oil rose in a bubble-like spike to $145 per barrel, and then subsequently crashed back to $32 per barrel a few scant months later as the global recession took hold. It has since tripled to over $100 barrel.

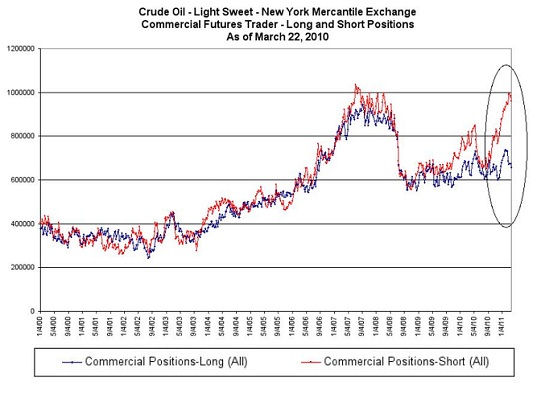

The third chart might give oil Bulls pause: the Commitment of Traders (COT) Commerical traders’ long and short positions in oil. Many investors and analysts look at COT for three basic categories of traders: small speculators, large speculators (such as hedge funds) and commercial traders, typically global corporations that hedge against big swings in commodity prices, and large financial institutions’ trading desks.

Note how the short interest of the commercial traders rose above long positions in the buildup to the price of oil peaking in 2008. As the price of oil marched ever higher, commercial traders sought out more protection in the form of short positions.

But the higher short positions might also reflect trading bets that the high price won’t last and a reversal is imminent.

Recently, long positions have declined while short positions have jumped. The spread between the two has widened to the largest gap in the past decade. Clearly, major players are betting (or hedging) that oil could drop precipitously.

A recent report from Goldman Sachs concluded that there is about $10 per barrel of speculative premium priced into oil. Given an expected rise in demand for oil as Japan replaces the electricity generation capacity lost from the Fukushima nuclear reactors, that would suggest there is no more than $10 a barrel downside in the price of oil.

Perhaps, but estimating the consequences of increased speculation is not a precise science. Given the COT chart above, it seems major players are either hedging a major decline in the price of oil or actively betting on it.

Ironically, higher prices lead to lower demand (recession) and lower prices. But in a speculative market, this volatility is a positive feature. Thus we can expect increased volatility and continuing swings in price as speculators drive price up and then reverse their trade to profit from declines.