It’s very hard to get enthusiastic about the markets on such a sad day.

It’s very hard to get enthusiastic about the markets on such a sad day.

I’m reporting from Las Vegas this morning so I’ll keep this brief as I’m a bit behind already. We have a couple of good articles to mark his passing on the main page so I won’t make this another one – I’ll just repeat what I said to Members last night: He was our Willie Wonka of gadgets – showing us new and wondrous things that he clearly made for his own enjoyment but was kind enough to share with us and smart enough to make a fortune doing it.

As to AAPL’s stock. Steve’s death is long priced in and the stock would be at least $500 if he were still alive and healthy. If Tim Cook can prove that AAPL remains on track this quarter and next, we will see AAPL move that way this year. I would say buy on the dip but, looking at the pre-market movement – I don’t think there will be a dip past the one we’re already seeing.

The other big news of the day is the BOE not just holding rates steady at 0.5% but also increased the size of their asset-purchase program by $116Bn, bringing this round of QEQE (Queen Elizabeth) to $426Bn. That’s 5% of the UK’s $2.25Tn GDP, that would be the same as the Fed doing a $750Bn round of Quantitative Easing. Although the ECB did not respond in kind this morning (they did keep their rates steady), with Trichet stepping down no one expected it until the new regime takes over anyway.

The other big news of the day is the BOE not just holding rates steady at 0.5% but also increased the size of their asset-purchase program by $116Bn, bringing this round of QEQE (Queen Elizabeth) to $426Bn. That’s 5% of the UK’s $2.25Tn GDP, that would be the same as the Fed doing a $750Bn round of Quantitative Easing. Although the ECB did not respond in kind this morning (they did keep their rates steady), with Trichet stepping down no one expected it until the new regime takes over anyway.

Meanwhile, the World’s 5th largest economy just announced a 5% stimulus package so it’s probably not a good time to bet the markets lower! Unfortunately, the announcement did knock the Pound down from $1.55 to $1.53 (1.3%) and the Euro fell from $1.34 to $1.325 (1.1%) and that sent the Dollar up from 79.4 back to 80 (0.75%) and that took some of the wind out of what was a very big futures rally but we held our 1.5% lines yesterday (as expected in the morning post).

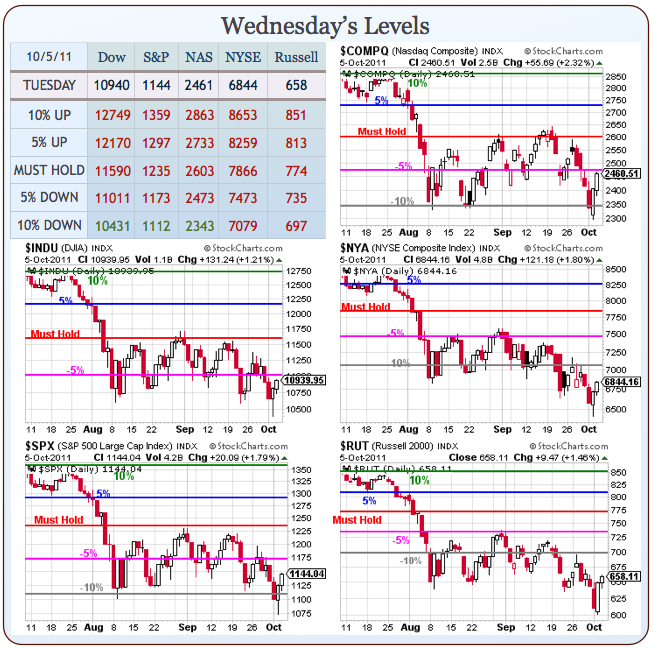

Unless the Dollar pops 80 (very doubtful), we should be testing those -5% lines on the Dow, S&P and Nasdaq as well as the -10% lines on the NYSE and the Russell – eventually, but maybe not today. TLT and the VIX have come down nicely so congrats to all the bullish faithful this week on braving the downturn with us but let’s not get cocky and take those profits off the table if we can’t stay green today.

We’re still not going to get excited until we get over those downtrends (see chart in yesterday’s post) on all of our indexes but that doesn’t stop us from making some solid profits playing the moves in between. As we get to the top of the downtrending range – we did take on some more hedges yesterday and will take more today if we fail those -5% levels, especially 11,000 on the Dow and 2,475 on the Nasdaq – we’re really not expecting a 30-point move today that the S&P needs to hit 1,173.

We’re still not going to get excited until we get over those downtrends (see chart in yesterday’s post) on all of our indexes but that doesn’t stop us from making some solid profits playing the moves in between. As we get to the top of the downtrending range – we did take on some more hedges yesterday and will take more today if we fail those -5% levels, especially 11,000 on the Dow and 2,475 on the Nasdaq – we’re really not expecting a 30-point move today that the S&P needs to hit 1,173.

Same Store Retail Sales are coming in very well for September as the US consumer is "not dead yet" with JWN and SKS (luxury) posting 10% gains, TGT up 5%, COST up 12%, M up 4.4%… Most of the retailers are beating estimates quite handily. Fortunately for our Corporate Masters – you don’t need more employees to make more sales as another 401,000 of our fellow Americans got pink slips last week. That’s in-line with expectations and shifts the focus back to tomorrow’s Non-Farm Payroll Report (8:30) and you know our goal is to get neutral ahead of that number!

We have Fed speak from Fisher at 11 and Geithner has a hearing with the Finanical Stability Council at 2pm but, other than that, we’re just waiting on the Jobs report tomorrow, although it’s Steve Jobs we’ll be thinking about today. Last item – Nouriel Roubini has a great tweet this morning:

Trichet leaves giving a finger to the markets thus leaving to Mario the dirty job of doing the right thing at risk of pissing off Germans