{kind=link}

Reminder: Pharmboy is available to chat with Members, comments are found below each post.

Throughout the global pharmaceutical industry, 47% of respondents are ‘more optimistic’ about revenue growth for their company over the next 12 months relative to the previous 12 months. A further 28% of respondents are ‘neutral’ about revenue growth as compared with 23% who are ‘less optimistic’ about their company’s revenue prospects (InfoGrok). China is expected to continue to be a large part of the industry's growth, where the EU (obviously) is expected to slow down. Overall, though, the pharma industry is still working through its patent cliff, with the final last call for a few blockbusters (The Calm Before the Storm).

This is the second installment of the Big Pharma Review where the pipelines of GlaxoSmithKline, Novartis, Eli Lilly, Sanofi, and AstraZeneca will be updated/discussed (Part 1 is here).

GlaxoSmithKline (GSK) has been in the headlines recently for its desire to acquire Human Genome Sciences for $13/share ($2.6B). The company has plenty of cash, and it is not like it cannot afford HGSI, as GKS has a market capitalization of $114B. The company generates revenue of $43B and has a net income of $8.6B. GSK has also increasing its stake in Theravance (THRX – article on THRX here), and bought a German company, Cellzome, which uses a proteomics technology to analyze the efficiency of a drug and for safety profiling research.

The company's flagship products are in respiratory (Seretide/Advair (named Beyond Advair) and Avodart). In recent news, two experimental melanoma medicines (dabrafenib and trametinib) slowed the progress of cancer with few skin complications in an early study. Dabrafenib works by inhibiting BRAF, a mutant gene that spurs cancer cell growth in about half of melanoma patients, while trametinib is designed to thwart a related protein called MEK, which helps tumors resist an assault on BRAF. The drug combination had a lower incidence of rash and skin lesions than had been previously reported with Roche’s Zelboraf, according to a study of 77 patients with advanced melanoma, the most-severe form of skin cancer.

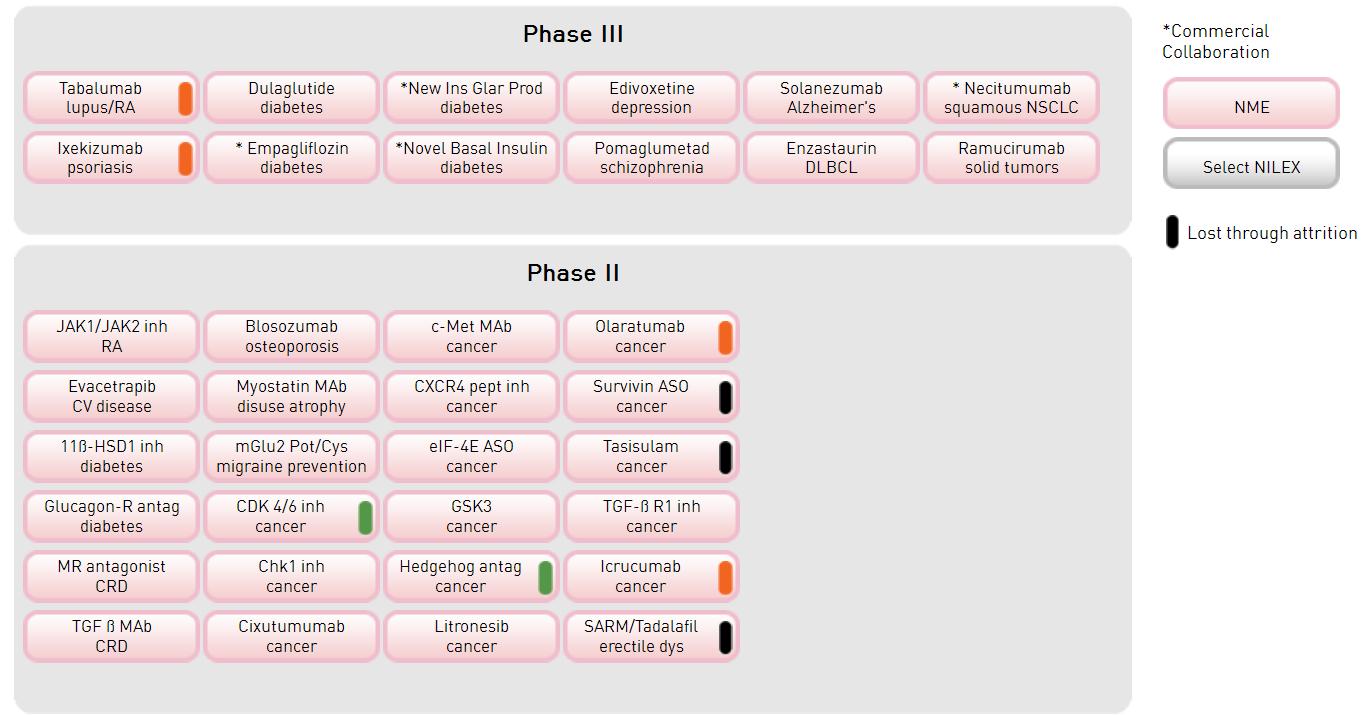

Vaccines, cardiovascular and dermatology (with its Stifel acquisition from a few years ago) will continue to drive growth. David Redfern of JPM has a very good slide deck from its 2011 Conference on GSK's revenue and pipeline here (PDF of GSK's pipeline here), and the company will be one that continues to deliver earnings and a nice dividend over the years to come.

![]()

Novartis (NVS) is a very well diversified pharmaceutical company and operates under four divisions: Pharmaceuticals, Generic (Sandoz), Eye Care (Alcon), and Consumer Health. The company has a market capitalization of $133B, generates revenues of $59B, and has a net income of $10B. Sandoz is about 16% of revenue, and remains the second largest generic maker behind TEVA. Its lead products are Prilosec and Levenox (biosimilar with Momenta). In the pharmaceutical wing, there are no more drugs ready to be tested for FDA approval in 2012, Novartis could have up to seven ready to be tested in 2013. The previous article about NVS is here. The company pays a 4.8% dividend yield, so if one likes a good pipeline, solid revenue growth, and diverse earnings exposure, NVS is a good one to own.

The last three companies noted below are ones that have lost, or are losing its portfolio faster than a speeding bullet. Lilly will lose over 70% of its revenues, Sanofi over 45%, and Astra over 40% of revenues out to this year (2012). There are two ways to regain these lost monies, grow internally – which is proving to be difficult, or grow by acquisition. Which will they choose or will they be forced to choose?

Eli Lilly (LLY) has a market capitalization of $47B and generates revenue of $24B and has a net income of $4.4B. I originally wrote about LLY here, and the company remains lite on the pipeline and forward looking revenues. The company is known for its two strongest therapeutic areas, antipsychotic/antidepressant and diabetes care.

Others feel differently, as Mel Daris at SeekingAlpha notes that LLY is 'Ready to Soar'. Cymbalta and a cancer treatment Alimta did well, but all I have to do is look at the graph below (from this Forbes article), and I know that I would not, could not recommend buying LLY – Period.

![]()

Sanofi Aventis (SNY)….where to start. My original article about the company is here, and not much has changed, even with the acquisition of Genzyme for (gulp) $20B. The company has a market capitalization of $96.5B. The company generates revenue of $44.6B and has a net income of $6.2B. With the loss of Plavixx ($6.3B in sales and co-marketed with BMY), and a host of other drugs, SNY needs to fill its coffers. The company has cut about 30% of its costs (hummm), and like LLY, the company has signed up with Covance to co-develop drugs. The deal with a contract research organization (CRO) is strategic is two ways: it makes development costs cheaper as the CROs get a portion of the revenue of anything that flows to market, and it makes things move faster in the development timeline as SNY gets preferential treatment when it needs to launch studies. SNY is trying to become a leader in the vaccine world, and they are competing with MRK and GSK on this front. Time will tell if this large pharma that has merged through the years, will be able to produce top of the line drugs for the next stage of its time-line.

AstraZeneca (AZN) has a market capitalization of $55B and the company generates revenue of $33,.6B and has a net income of $10B. There has not been a AZN article yet, but maybe there should be. The company is desperate to stuff their pipeline (see the projected revenues graph with LLY above). Recently AZN bought Ardea Biosciences for $1.2B fpr their gout and cancer drugs, but this is hardly enough to offset the >$6B loss of Symbicort and Seroquel. The company has a FGFR2 inhibitor for cancer (read about the target here), as well as it has teamed up with BMY on dapagliflozin, which was rejected by the FDA for diabetes until more data became available. The EU recently recommended the drug. Overall, the company boasts a 9% dividend yield (for how long?), but Cramer, on the June 22, 2012 MadMoney Show, did recommend going with LLY over AZN. Maybe AZN is not so bad after all!