{kind=link}

Courtesy of Charles Hugh-Smith of OfTwoMinds

Just as the Federal Reserve cannot directly force you to stick the needle of monetary heroin (debt) into your arm, it also can't force employers to pay employees more.

The official policy of the Central Bank (Federal Reserve)/government is: inflation is necessary for "growth," i.e. economic expansion. The unstated reason for this official support of inflation is that it's easier for borrowers to service their debts as their income inflates.

To take an extreme example: let's say a homeowner has a mortgage of $100,000, an annual wage of $40,000 and annual mortgage payments of $10,000. At 100% annual inflation in both prices and wages, the home mortgage remains fixed at $100,000, the payment remains fixed at $10,000 but his earnings double to $80,000.

Where the mortgage payment initially took 25% of his earnings, now it only takes 12.5%. Yippee Skippy, the homeowner has an "extra" 12.5% of his earnings to support more consumption and debt: thanks to inflation, the homeowner can now buy a car on credit and use the "extra" 12.5% of earnings to pay the auto loan.

Central banks around the world seek inflation for another reason: the Keynesian Cargo Cult that dominates all central banks and governments believes with quasi-religious certainty that people respond to inflation by buying more stuff now rather than later: since prices will rise in the future, it makes sense to buy stuff now at "lower prices compared to next year's prices."

This is called bringing demand forward, as the demand to buy stuff is shifted from the future to the present.

In an economy dependent on debt-based consumption, inflation is absolutely essential to reduce the real costs of servicing old debts so households can afford to buy more stuff on credit. This is the basis of the Fed's insistence that inflation is equivalent to "growth"–inflation enables households to continue adding more debt to buy more stuff, as long as earnings inflate along with prices.

There are three problems with the Fed's "inflation is growth" scenario:

1. Earned income (wages and salaries) don't inflate along with prices

2. Rising inflation and low interest rates crimp lender profits and increase risks

3. Bringing demand forward exhausts households' ability to fund additional consumption with debt.

To date, all the Fed's efforts to generate inflation have bypassed earned income: wages and salaries have declined when adjusted for inflation. Hourly wages: stagnant since 2008.

source: Rising Wages Where? Real Wages Post First Annual Decline Since 2012

Real household income has declined across the entire income spectrum:

Here's the same data in chart form, courtesy of Doug Short:

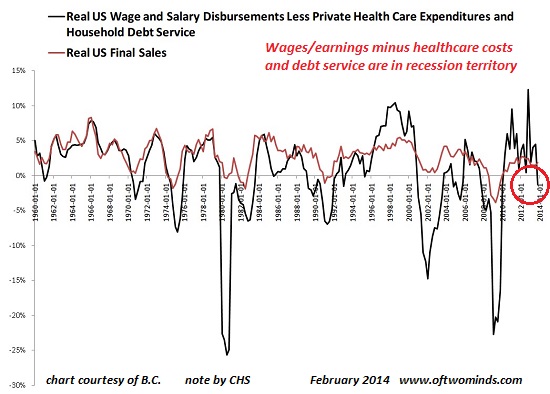

Deduct healthcare expenses and debt service, and what's left of wages for the rest of life's expenses is tanking: Courtesy of longtime correspondent B.C.:

Debating the real rate of inflation has become a financial parlor game because the real rate of inflation depends on the household's demographics, locale, expenses and income. Anyone paying the unsubsidized costs of healthcare or college tuition is experiencing crushing inflation (i.e. loss of purchasing power), while the low-income or retiree household receiving federal subsidies (i.e. no exposure to the real costs of higher education and healthcare) experiences low inflation.

But even the official measures of inflation reflect the destruction of purchasing power wrought by supposedly low inflation when wages are stagnant while costs keep rising:

source: What Inflation Means to You: Inside the Consumer Price Index (Doug Short)

Inflation: A Six-Month X-Ray View (Doug Short)

Fed policies have inflated asset prices but left earned income in the ditch. Please read How Effective Have The Fed's QE Programs Been? (STA Wealth Management) for a fuller understanding of the perverse consequences of the Fed's "inflation is growth" policies.

Though nobody in official circles dares discuss it, the reality is inflation coupled with low interest rates reduces lenders' profit margins and increases systemic risk. In an economy in which wages are stagnating or declining in real terms while major expenses are galloping ever higher, the only way lenders can expand borrowing is to lend to marginal borrowers–households who would not qualify for loans under prudent risk management.

For evidence of this, we need only look at the explosive rise in subprime auto loans and higher-education student loans: In a Subprime Bubble for Used Cars, Borrowers Pay Sky-High Rates (New York Times)

Lastly, there are limits on how much future demand can be brought forward when wages are declining. The Keynesian Cargo Cult has absolute faith in the notion that consumers faced with inflation will buy more today rather than pay more next year.

But the facts do not support the Keynesian Cargo Cult's misplaced faith. In Japan, where the central bank and government have struggled for years to generate price inflation as the means to "re-start growth," wages have fallen by 9% in real terms since 1997. (source: Voodoo Abenomics: Japan's Failed Comeback Plan Foreign Affairs)

When prices rise faster than incomes, people can't afford to buy as much. Soconsumption necessarily declines as prices go up and purchasing power goes down.There is nothing mysterious about this, but the Keynesian Cargo Cult is unmoved by mere fact and common sense.

Just as the Federal Reserve cannot directly force you to stick the needle of monetary heroin (debt) into your arm, it also can't force employers to pay employees more. Prices don't just rise for consumers; they rise for producers and employers as well. Every tick up in healthcare costs and producer costs increases the need for businesses to slash the one large expense they still control: payroll.

We all see the desperate gimmicks corporations are deploying to lower costs while keeping prices the same: reducing package sizes, putting less product in each package, selling "individual servings" at higher cost per ounce, lowering quality of the product, using more fillers, and so on.

The ultimate hubris of the Keynesian Cargo Cult (which includes the global economy's central banks) is the naive notion that they can manipulate an entire system with a few levers such that the desired outcome–and only the desired outcome–is the output.

The idea that you can change one input in an interconnected system of systems and only affect the one output you want is not just naive and simplistic: it requires a level of blindness and incompetence that is off the charts.