{kind=link}

Courtesy of Charles Hugh-Smith of Of Two Minds

The Fed's substitution of debt for income has only doomed the nation to a deeper, more painful realignment of real income and expenses.

The economic "recovery" has been based on a simple premise: debt can be substituted for income with no ill effects. As real household incomes have declined, the legitimate foundation of additional spending–more income–has eroded for the bottom 90%.

Even the ephemeral foundation of additional debt-based spending–the Fed's beloved wealth effect–has eroded for all but the thin layer at the very top of the wealth pyramid.

To replace this diminished income, the Status Quo has substituted debt as the source of additional spending: household debt, corporate debt and government debt.

But debt is not income. Rather, debt requires income to be diverted to pay interest and principal. So substituting debt for income ends up further depleting declining income.

This scheme of keeping a bloated, inefficient Status Quo afloat with debt is not a success–it's a failure on an epic scale.

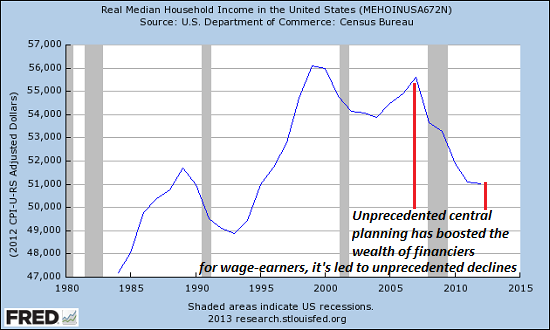

Let's start by reviewing household income, which has declined in real (adjusted for inflation) terms. The drop in real income is across the board; those in the top rungs have experienced a smaller relative decline than their lower-income brethren, but they still has less purchasing power than they did six years ago.

Here's another look at the same basic data:

Here's real median household income:

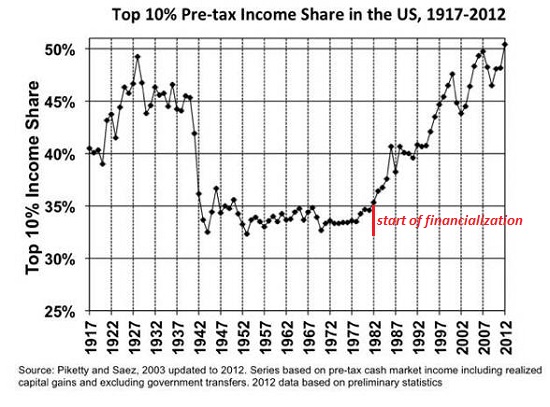

Some apologists claim median income doesn't reflect how well most households are doing in the New Normal. As researchers Piketty and Saez found, the gains in income have all accrued to the top 10%. So while this might be good news for Porsche dealerships in wealthy enclaves, it doesn't follow that the economy is healthy because a relative handful of households are doing very well for themselves.

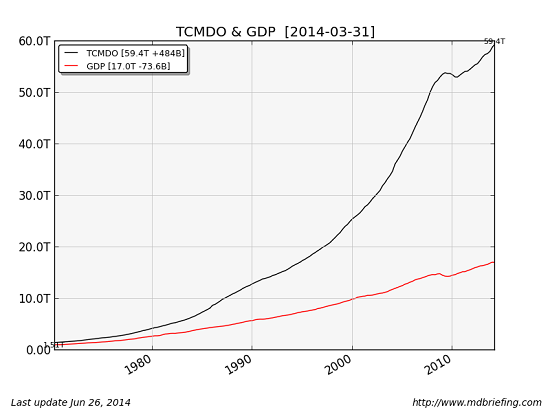

If we add up all debt–household, finance, corporate and government–we see debt has soared and growth has stagnated: this is a classic case of diminishing returns as more debt is required to add each additional increment of GDP.

At some point, additional debt is taken on to simply make interest payments; at that juncture, there is no consumption/buying taking place with the new debt: it's simply keeping the borrower out of default.

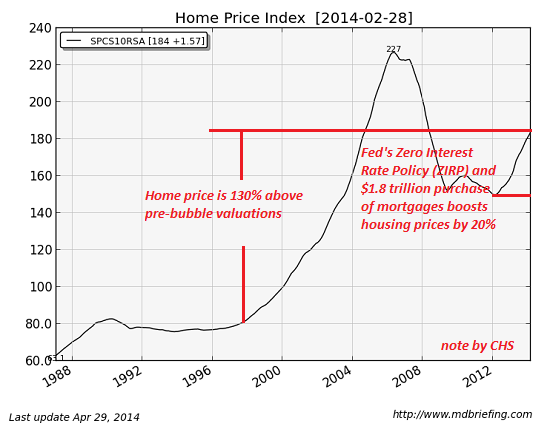

The Fed has pulled out all the stops to reflate the housing and stock market bubbles, as a means of boosting the wealth effect, i.e. the belief that people who see their homes and 401K accounts rising will feel wealthier and therefore more likely to borrow and spend money on stuff they don't need.

Housing has entered an echo-bubble:

But alas, these unprecedented Fed-inflated bubbles haven't pushed household wealth up to previous levels. The power of the wealth effect is greatly diminished when wealth has yet to recover to previous levels.

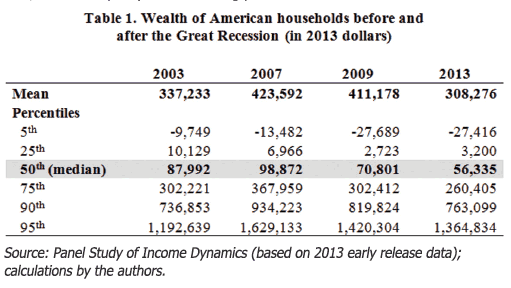

source: Wealth Levels, Wealth Inequality And The Great Recession (PDF)

Even the top 10% have seen their real wealth decline sharply from the peak in 2007. So much for the wealth effect, which can only work on those with short memories.

The scheme of substituting debt for income to prop up a corrupt, bloated and ineffective Status Quo is a financial game with a predictable end: even with low interest rates, each additional unit of debt requires more future income be diverted to pay interest and principal. As income erodes due to Fed-induced inflation and other structural deformations, spending more of the diminishing income pie on servicing debt becomes increasingly destructive–especially to the core dynamic of our consumerist economy: taking on more debt to consume more stuff.

No wonder so many households are behind on their debt payments: Delinquent Debt in America (Urban Institute): An alarming 77 million Americans — 35 percent of adults with credit files — have debt in collections reported in their credit files, with an average debt amount of nearly $5,178.

Substituting debt for income can fill the widening gap between income and expenses for a few months. Beyond a few months, however, the household, company or nation that wants to avoid insolvency and default must align expenses with real income (as defined by purchasing power of the income).

Six years is not a few months. The Federal Reserve has gamed and manipulated the financial system to enable every person and entity in the U.S. to take on more debt at lower rates of interest. The past six years have been a grandiose gambit that additional debt-based spending would magically transform a financialized, debt-dependent, bloated and ineffective economy into a productive economy based on prudent risk management and investment of capital.

Sorry, members of the Fed–magical thinking doesn't work in the real world. Your substitution of debt for income has only doomed the nation to a deeper, more painful realignment of real income and expenses, and a more devastating recognition of phantom assets and collateral.