{kind=link}

Courtesy of Charles Hugh-Smith of Of Two Minds

A long-time reader recently chastised me for using too many maybes in my forecasts. The criticism is valid, as "on the other hand" slips all too easily from qualifying a position to rinsing it of meaning.

A long-time reader recently chastised me for using too many maybes in my forecasts. The criticism is valid, as "on the other hand" slips all too easily from qualifying a position to rinsing it of meaning.

That said, given that we're in uncharted waters, maybe is prudent and certainty is extremely dangerous. I have long held that the financial policy extremes that are now considered normal are unprecedented in the modern era: extremes in debt, leverage, risk, complexity and willful obfuscation of these extremes.

Consider the extent to which sky-high asset valuations and present-day "prosperity" depend on extremes of leverage: autos purchased with no money down, homes purchased with 3.5% down payments and FHA loans, stocks bought on margin, stock buybacks funded by loans, student loans issued with zero collateral, and so on–an inverted pyramid of "prosperity" resting precariously on a tiny base of actual collateral.

Since we have no guide to the future other than the past, we extrapolate past trends. Human nature hasn't changed over the short time-frames of civilizations (i.e. the past few thousand years), so in terms of human drives, emotions and responses, the past is an excellent guide to the range of human responses to crisis, euphoria, greed, fear, etc.

But extending trends is a shifting foundation for forecasts, as trends end and reverse, generally without telegraphing the end of an era. Few in 1639 China foresaw the collapse of the status quo Ming Dynasty a mere five years hence.

With the hindsight of history, we can discern the cracks in the Ming Dynasty before its collapse, but once we shift to our own era, things become less certain.

In my view, we're drifting in uncharted seas.

I have covered the dangers of certainty before: Certainty, Complex Systems, and Unintended Consequences (February 14, 2014)

What I see as extremes that must necessarily end badly, others see as mere extensions of recently successful policies and trends. Let's review a few of the many extremes that we now accept as ordinary and harmless.

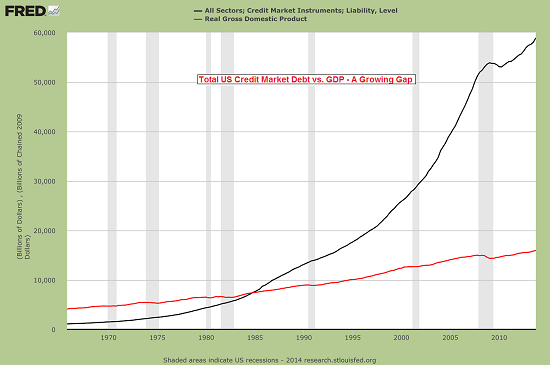

Consider how much new debt is now required to lift GDP ("growth") off the flat line:

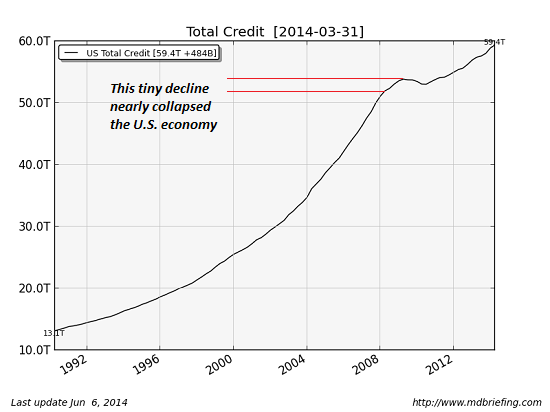

The slightest pause in the expansion of credit nearly collapsed the entire global economy:

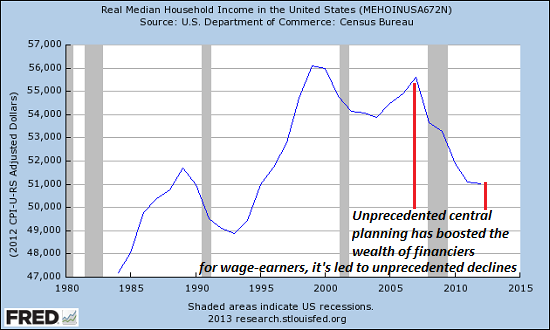

Extraordinary central state and bank policies have boosted the wealth of those closest to the Federal Reserve's money spigot and left everyone else poorer:

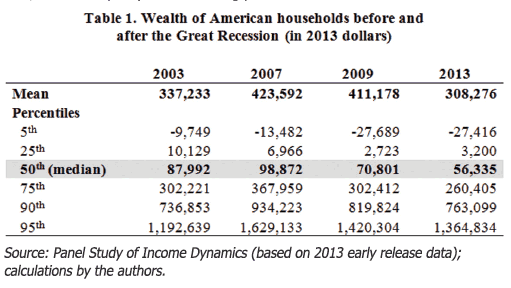

It's not just real income that's declined–so has household wealth.

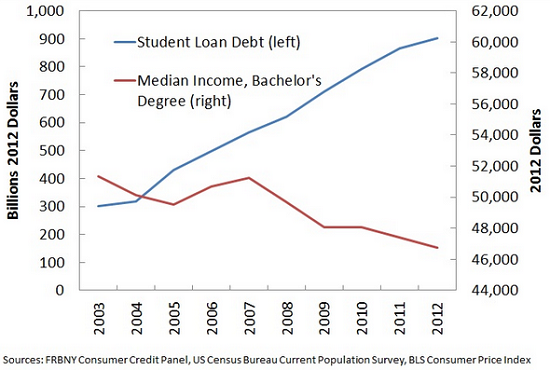

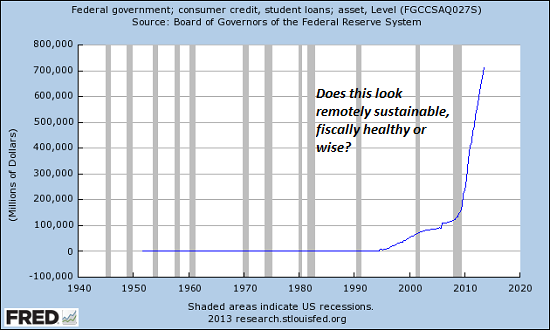

Incentives to borrow money to obtain a college degree are declining while student loan debt hits astounding extremes:

Feel free to extend this line of Federally funded student debt: where does it end?

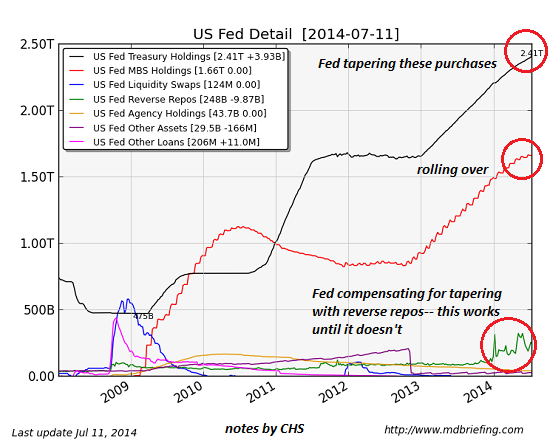

The Federal Reserve has pushed astonishingly extreme policies for six years. Now that the Fed owns significant chunks of the Treasury bond and mortgage bond markets, it's being forced to limit these easing programs:

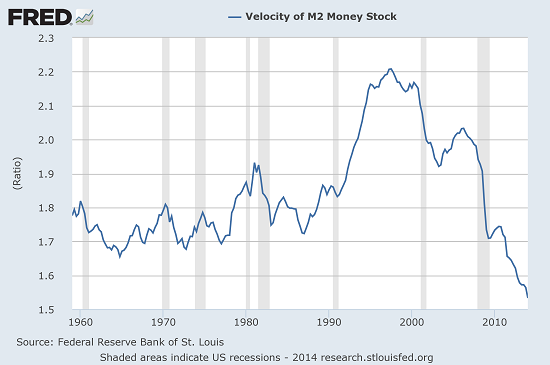

All the Fed money-printing and bond buying has sent money velocity in the real economy into a tailspin: this is good, right? No, actually it's a calamity. Money has slipped into a coma.

Extend the trendlines in these charts, and then ask yourself: where do they end? What will they trigger as they push ever deeper into uncharted waters?

Picture by unformat at Pixabay.