{kind=link}

Courtesy of Pam Martens.

Remember when the Department of Homeland Security was issuing those color-coded terrorist alerts? Well, they don’t do that anymore. They’re back to using plain ole black-and-white words to describe threats.

Apparently, however, the U.S. Treasury’s Office of Financial Research (OFR) thought it was such a cool idea that they’ve started color-coding threats to our financial security from the denizens on Wall Street: the gang that brought our country to its knees in 2008 while the most expensive military in the world was hunting down robed cave-dwellers in the Middle East.

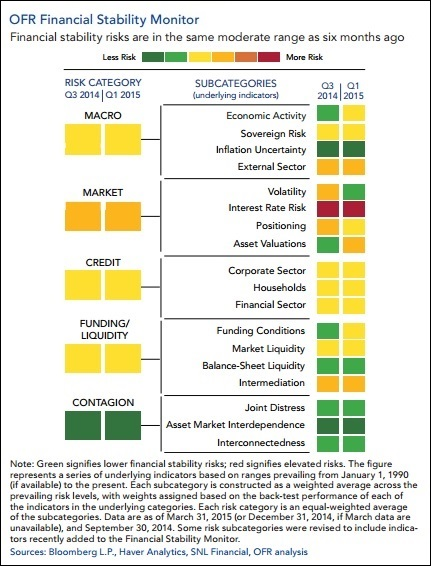

OFR’s color-threat alert is called the Financial Stability Monitor. The monitor is based on approximately 60 indicators and organized as a heat map: The closer an indicator is to the red end, the more elevated the risks; the closer an indicator is to the green end of the spectrum, the lower the risks. The Monitor, released yesterday, says that “financial stability risks remain moderate.” Unfortunately, when we studied the accompanying chart, we found that it’s based on first quarter data, meaning it’s almost three months old. (Imagine Homeland Security issuing a terrorist alert, then telling you it might not be all that reliable because it’s based on stale intelligence.)

Nonetheless, there’s some very interesting takeaways from the Monitor. First, even though the OFR has characterized the financial stability threat as “moderate,” a close reading of the report suggests a heightened threat. These are some key points from the report:

- Financial and economic risks have further decoupled, with financial risk-taking occurring against the backdrop of a tepid growth recovery.

- Global monetary policies and economic growth continue to diverge. Central banks in some advanced economies, led by the European Central Bank and the Bank of Japan, are conducting highly expansionary monetary policies, while in the United States, the Federal Reserve is closer to embarking on a tightening cycle.

- Foreign risks have increased, including intensified government financing risks in Greece and weakening economic fundamentals in key emerging markets.

- After a lengthy period of unusually low yields, long-term government bond yields in advanced economies have risen abruptly since April. The speed and volatility of the correction have been significant, demonstrating the fragility of market liquidity and the vulnerability of markets to shocks during periods of low volatility and extended bond duration…

- Although low volatility previously contributed to excessive risk-taking, the recent increase in volatility has not been accompanied by a proportionate decline in risk-taking.

- The migration of risks from banks to less-regulated sectors is a continuing concern. For example, non-bank institutions continue to increase their share of highly leveraged syndicated loans.

- Some market liquidity measures — the ability of market participants to sell assets with limited price impact and low transaction costs — signal a deterioration in liquidity. These changes have occurred along with a decline in the provision of liquidity by primary dealers, which could potentially reduce their willingness to buffer intense selling pressure.

Reduced liquidity, migration of risks from banks to less-regulated sectors, and rising interest rates sound to us like the perfect financial storm potentially in the making.

Indeed, the one area flashing red on the chart is interest rate risk. Gary Cohn, President and COO of Goldman Sachs, took to the radio last week to share his two cents on what’s likely to happen when the Federal Reserve finally hikes interest rates (after talking about it since what feels like the Paleozoic era).

…