{kind=link}

Courtesy of Lance Roberts of Real Investment Advice

The Fed Is Behind The Curve…Again

Over the last couple of months, I have been discussing the technical deterioration of the market that is occurring beneath the surface of the major indices. I have also suggested there is more than sufficient evidence to suggest we may be entering into a more protracted “bear market cycle.”

The caveat to this, of course, has been the potential for a renewed round of Central Bank interventions that would theoretically once again postpone the onset of such a decline. Previously:

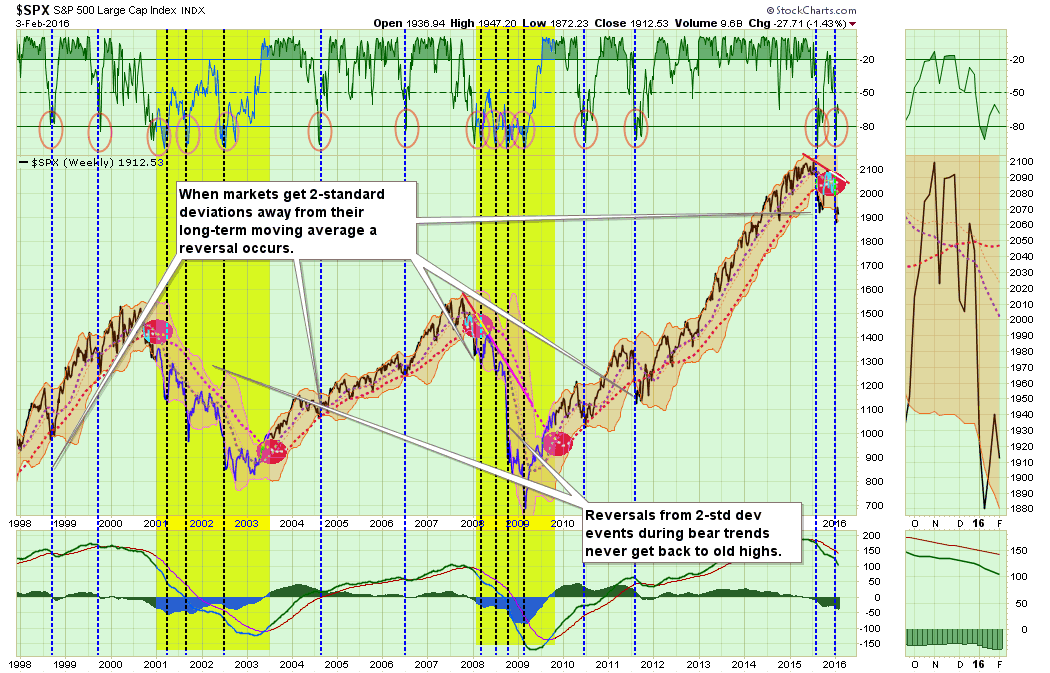

“The top section of the chart is a basic ‘overbought / oversold’ indicator with extreme levels of ‘oversold’ conditions circled. The shaded area on the main part of the chart represents 2-standard deviations of price movement above and below the short-term moving average.”

“There a couple of very important things to take away from this chart.

- When markets begin a ‘bear market’ cycle [which is identified by a moving average crossover (red circles) combined with a MACD sell-signal (lower part of chart)], the market remains in an oversold condition for extended periods (yellow highlighted areas.)

- More importantly, during these corrective cycles, market rallies fail to reach higher levels than the previous rally as the negative trend is reinforced.

Both of these conditions currently exist.

Could I be wrong? Absolutely.

This entire outlook could literally change overnight if the Federal Reserve leaps into action with a rate cut, another liquidity program or direct market intervention.”

This is just the most recent observation. I begin discussing the deterioration in the markets beginning last summer as early signs of the topping process began and I lowered portfolio model exposures to 50% of normal allocations.

However, despite the fact that interest rates have continued to trend lower, economic data and corporate profits have deteriorated, and inflationary pressures non-existent; most Fed speakers have sounded consistently hawkish and steadfast in their views of 4-rate hikes in 2016.

I have been steadfast in my claims that hiking rates given the current economic conditions is a mistake and will rapidly push the markets and economy towards a reversion. To wit:

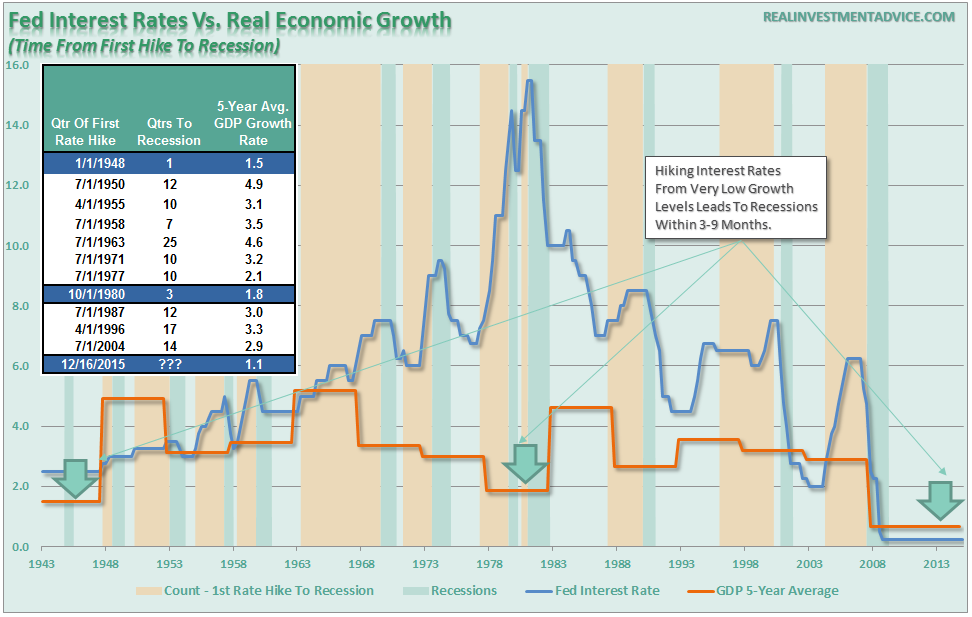

“Looking back through history, the evidence is quite compelling that from the time the first rate hike is induced into the system, it has started the countdown to the next recession. However, the timing between the first rate hike and the next recession is dependent on the level of economic growth at that time.

When looking at historical time frames, one must not look at averages of all rate hikes but rather what happened when a rate hiking campaign began from similar economic growth levels. Looking back in history we can only identify TWO previous times when the Fed began tightening monetary policy when economic growth rates were at 2% or less.

(There is a vast difference in timing for the economy to slide into recession from 6%, 4%, and 2% annual growth rates.)”

“With economic growth currently running at THE LOWEST average growth rate in American history, the time frame between the first rate and next recession will not be long.”

It is now becoming quite apparent that the majority of economists, analysts, and Fed members have been quite mistaken in their assessments of the impact of global turmoil and the collapse in commodity prices on the domestic economy. (Read my previous commentary on oil and China)

From Market News: (Via ZeroHedge)

“Top Federal Reserve policymakers are leaving little doubt the financial turbulence and souring of the global economy could have significant implications for U.S. monetary policy, but they are loathe to draw too many conclusions about the appropriate path of interest rates at this juncture.

One thing is for certain: The tightening of financial conditions that has taken place since the Fed began raising short-term rates in mid-December is a matter of considerable concern to the Fed, New York Federal Reserve Bank President William Dudley said in an exclusive interview with MNI Tuesday.

But, it was supposed to signal the US economy is ‘strong enough’ to sustain a lift off and decouple from the rest of the world which is scrambling to cut rates. Guess not.

As MNI adds, “a weakening of the global economy accompanied by further appreciation in an already strong dollar could also have “significant consequences” for the U.S. economy, Dudley told MNI.”

“I can give you my own interpretation,” the committee’s vice chairman replied. “I read that as saying we’re acknowledging that things have happened in financial markets and in the flow of the economic data that may be in the process of altering the outlook for growth and the risk to the outlook for growth going forward.”

“But it’s a little soon to draw any firm conclusions from what we’ve seen,” he cautioned.”

If history serves as any guide, with the entire flow of data from economic underpinnings, high-yield markets, commodity prices and deteriorating profits screaming for help, by the time the Fed “draws any firm conclusions” it will be far too late to make any real difference.

Interest Rate Predictions Come To Fruition

Well, that didn’t take long. At the beginning of this year, I wrote in the 2016 Market Outlook & Forecast the following:

“With the Federal Reserve raising interest rates on the short-end (Fed Funds), it will likely push the long-end of the curve lower as the economy begins to slow from the effects of monetary policy tightening.

From a purely technical perspective, rates have been in a long-term process of a tightening wedge. A breakout to the upside would suggest 10-year treasury rates would soar to 3.6% or higher, the consequence of which would be an almost immediate push of an economy growing at 2% into recession. The most likely path, given the current economic and monetary policy backdrop, will be a decline in rates toward the previous lows of 1.6-1.8%.(Inflation will also remain well below the Fed’s 2% target rate for the same reasons.)

“Of course, falling rates means the ongoing “bond bull market” will remain intact for another year. In fact, if my outlook is correct, bonds will likely be one of the best performing asset classes in the next year.”

When I wrote that missive, rates were at 2.3%. Yesterday, they touched 1.8% and intermediate and long duration bonds have been the asset class to own this year.

While rates will likely bounce in the short-term, I still suspect rates will finish this year closer to the low-end of my range.

Have Stocks Priced In A Recession?

I have read a significant amount of commentary as of late suggesting that the current decline in stocks have “priced in” the economic and earnings weakness we are currently witnessing.

Such is hardly the case. There are two primary indicators that warrant such skepticism.

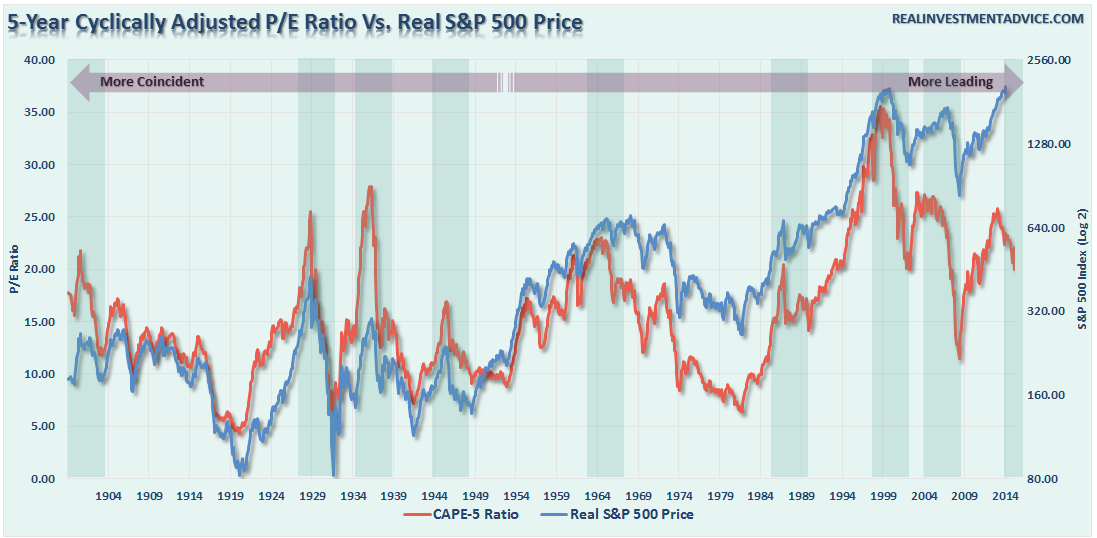

The first is valuations.

The chart above is a 5-year Cyclically Adjusted Price Earnings (CAPE) ratio (data source: Dr. Robert Shiller.) By speeding up the time frame from 10-years to 5-years, we find that valuation changes have shifted from being more coincident prior to 1970, to more leading currently. As shown, the downturn in valuations has been a leading indication of more severe market corrections particularly since the turn of the century.

The second is profits.

While still early into 2016, it already appears that earnings will post an annual decline for the second year running. Annual declines in earnings have historically been more evident during recessionary economic cycles (which only makes sense as consumption slows.)

It is not just me suggesting that risk is currently high either. Here is a note from RBC:

“Based on current valuations, the prices of most stocks don’t appear to have factored in a recession scenario, ‘hence the downside should we see a recession could be rather severe,’ RBC Capital Markets’ global equity team wrote in a research note to clients who believe the shares of most companies could still fall another 50% or more from current levels.”

Such declines have been consistent with past economic/earnings recessions as “overvaluation” reverts back to “undervaluation.”

Just some things to think about.