{kind=link}

Courtesy of Lance Roberts, RealInvestmentAdvice.com

More Volatility – Still No Movement

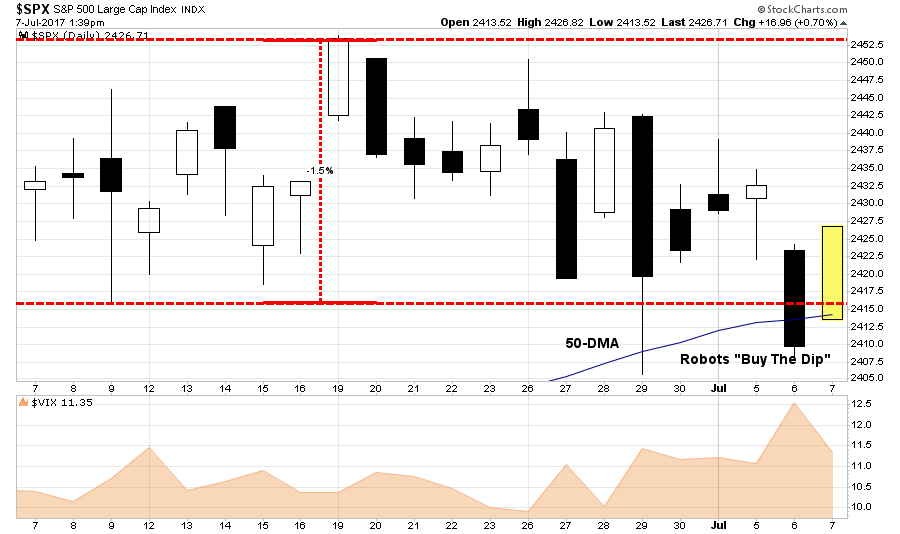

Last week, I discussed the issue of “lot’s of volatility with little movement” stating:

“The last couple of weeks have experienced a sharp rise in price volatility. While stocks have vacillated in a very tight 1.5% trading range since the beginning of June, there has been little forward progress to speak of. However, notice that support at 2415 (50-dma) has remained solid as ‘robots’ continue to execute their program of ‘buying the dips.'”

“This lack of progress keeps us ‘stuck’ with respect to portfolio positioning.”

I remain very cautious on the overall market, currently, and the deterioration is leadership remains concerning. However, the trend remains bullishly biased which keeps portfolios allocated on the long side for now.

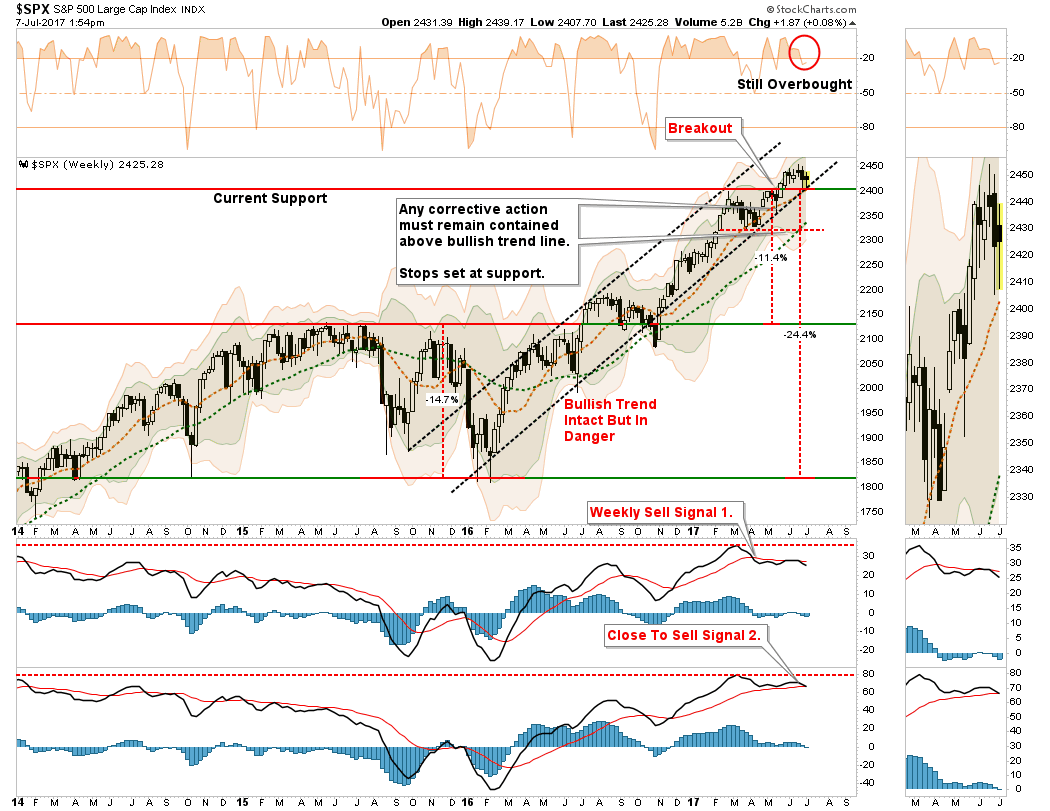

With that said, the recent “sideways” movement has NOT worked off the previous overbought condition of the market on an intermediate term basis as shown below.

As I have stated previously, the presence of the primary “sell signal” (signal 1) has suggested price weakness in the market would likely continue. However, the recent corrective action has now pushed the “secondary” signal towards initiation. Previously, the confluence of both intermediate-term “sell” signals have historically been in conjunction with deeper corrections in the market.

I am giving the market a bit of “room,” given the week was interrupted by a holiday which tends to let the “inmates run the asylum.” Next week will give us a better picture of the current risk/reward setup.

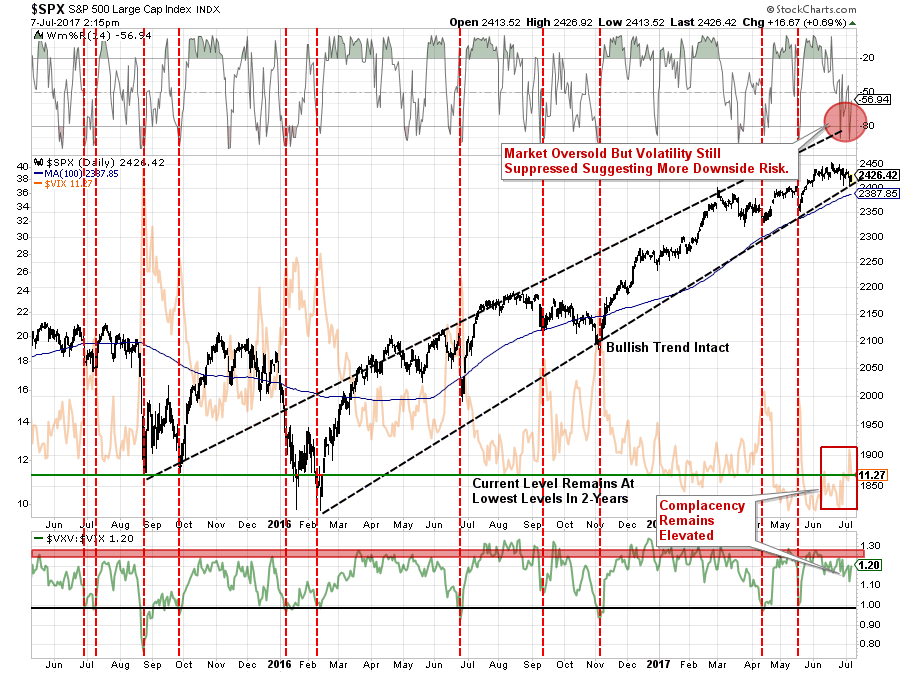

Despite the uptick in volatility last week, volatility remains suppressed at historically low levels. As shown in the chart below, the recent “back and forth” action has reduced the overbought condition of the market short-term with stocks testing the bullish uptrend. Furthermore, while the market is oversold on a “daily” basis, versus “weekly” as noted above, the high-level of complacency DOES NOT align with the tradeable set ups noted previously by the vertical red dashed lines.

Let me reiterate from last week:

“I continue to suggest a healthy regimen of risk management practices in portfolios by following some rather simple guidelines (the same ones that we followed to harvest profits recently as noted above.)

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.”

For now, as noted above, let’s wait until next week to see if the “bears” can continue to gain on the “bulls.” If they do, we will then begin to evaluate models to reduce overweight positions, raise some additional “cash” and potentially begin to deploy some hedges.

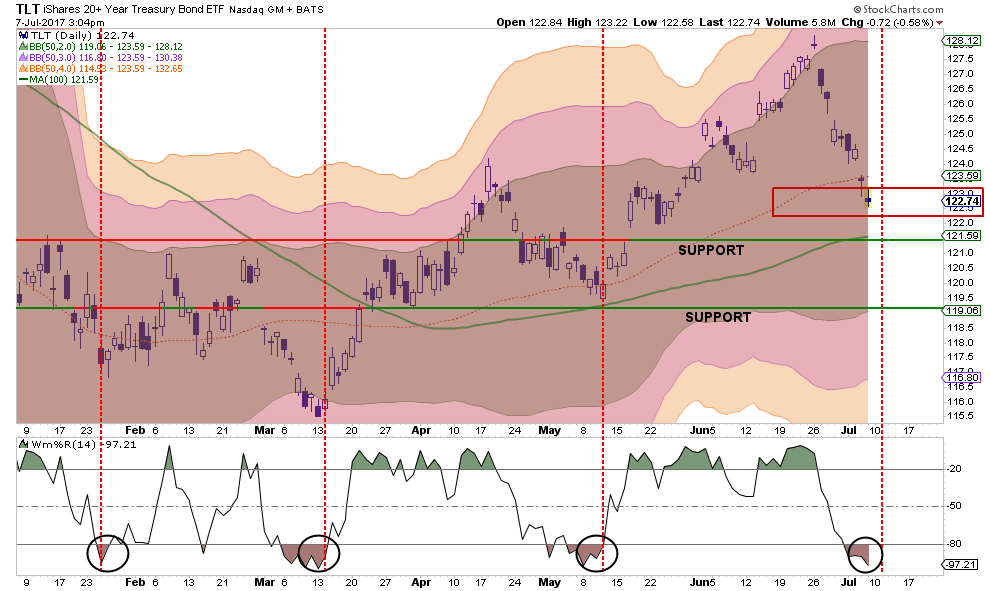

Approaching A Bond Buying Opportunity

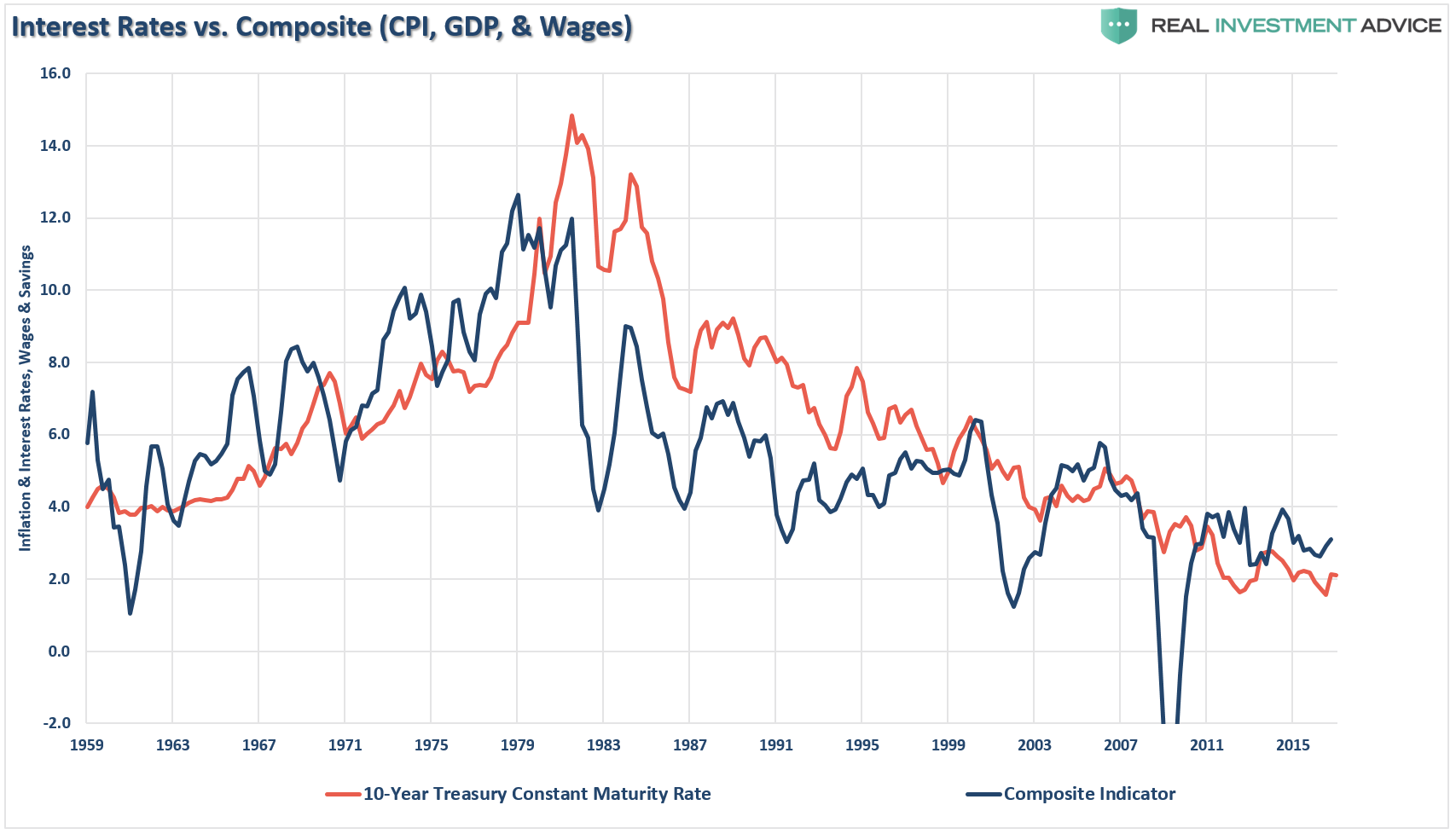

Last week, I discussed “why” interest rates can NOT much substantially higher from current levels. To wit:

“As I have discussed many times in the past, interest rates are a function of three primary factors: economic growth, wage growth, and inflation. The relationship can be clearly seen in the chart below by combining inflation, wages, and economic growth into a single composite for comparison purposes to the level of the 10-year Treasury rate.”

“As you can see, the level of interest rates is directly tied to the strength of economic growth and inflation.”

This week, I want to look at interest rates from a purely technical point. Interest rates, like stock prices, are bound by the laws of physics. Prices can move only so far in one direction, before eventually returning to the mean. When rates plunged from 2.6% to 2.15% recently, bond prices had become extremely overbought and some correction action was expected.

I have been recommending to readers over the last couple of months to withhold adding bond positions given the level of richness in bond prices. That advice has played well, and the recent spike in interest rates has pushed bond prices to important levels of support while reducing much of the previous overbought condition.

As noted last week:

“However, bonds are not yet oversold. Therefore, we will hold off on adding to existing bond exposures, or adding new positions, this week with the expectation rates could rise a bit further.”

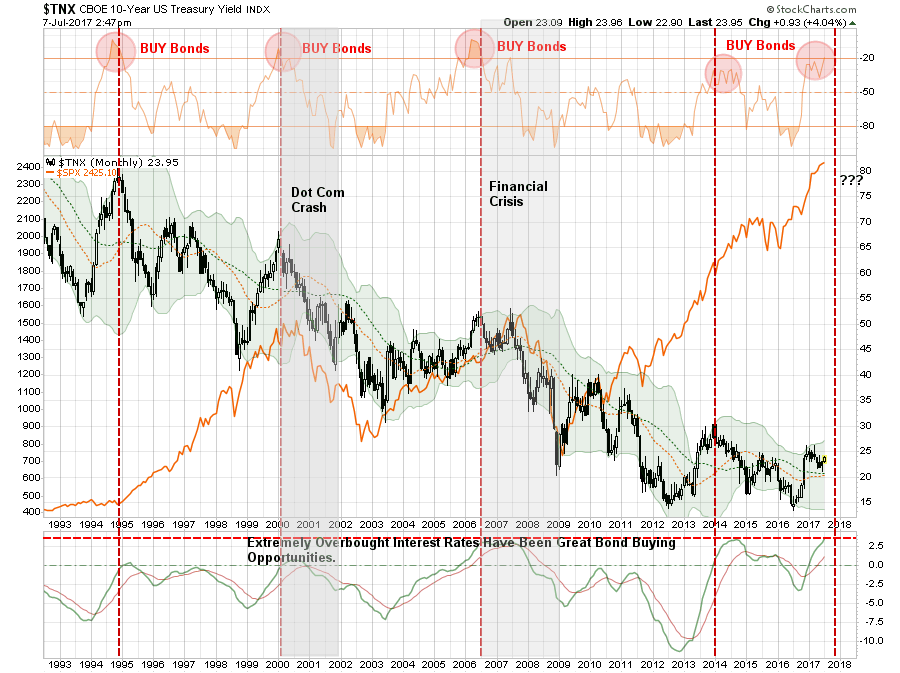

The rise in rates last week has pushed the 10-year yield to some of the highest “overbought” conditions witnessed in the past 25-years. Each time rates have been at these levels previous TWO things have happened.

- There was an economic or financial market backlash, and;

- It was a great time to buy bonds.

Sure. Maybe this time IS different and rates will “magically” decouple from the underlying drivers of economic and inflation and go spiraling higher. Such an event would last about 37-seconds until higher borrowing costs choke off what bit of nascent economic growth we currently have.

As David Rosenberg noted this past week:

“In fact, when you go back and look at the announcements of QE1, QE2, and QE3, the Treasury market actually did not rally on these … but the stock market sure did! And you know what, in those intermittent periods when the Fed stopped its balance sheet expansion (only to then precipitate the next round), the ensuing pullback in risk appetite and the correction in the S&P 500 actually caused the bond market to rally on the safe-haven effect!”

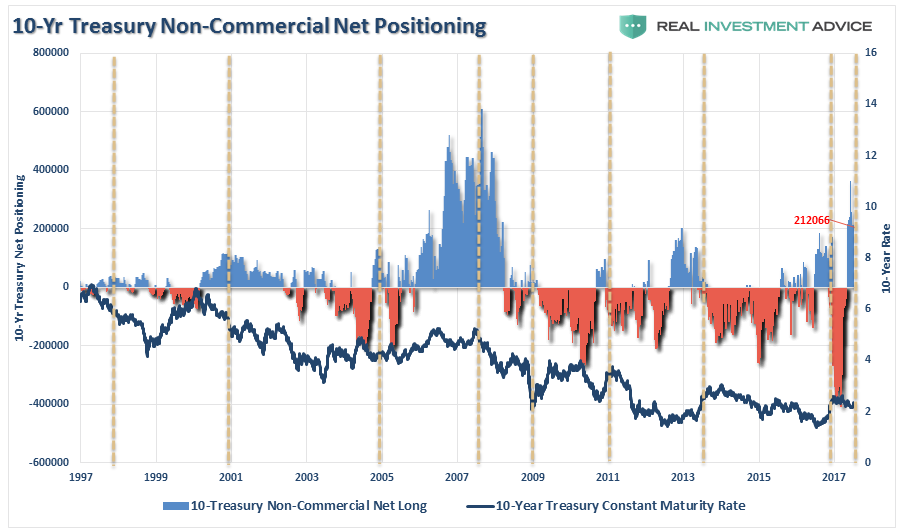

Furthermore, the net positioning of commercial traders also recently reached a peak LONG position in bonds, historically the reversal of such a net long, to a net short position, has denoted the peak in interest rate increases and a prime opportunity to buy bonds. That reversal has already begun.

However, as noted in the chart above, when the economy slips into the next recession, interest rates will once again join the long-term downtrend towards 1% or less.

Bonds will be the right place to be. Stocks won’t be.

So, as I stated, we are looking to BUY bonds…and will likely start nibbling at positions next week.

Interesting Tidbits

I ran across a couple of interesting tidbits this past week that I thought were worth sharing with you. The first point comes with reference to my comments over the last couple of weeks of algorithms kicking in to buy every dip. In fact, they now appear to be hitting the “button” faster than ever. To wit:

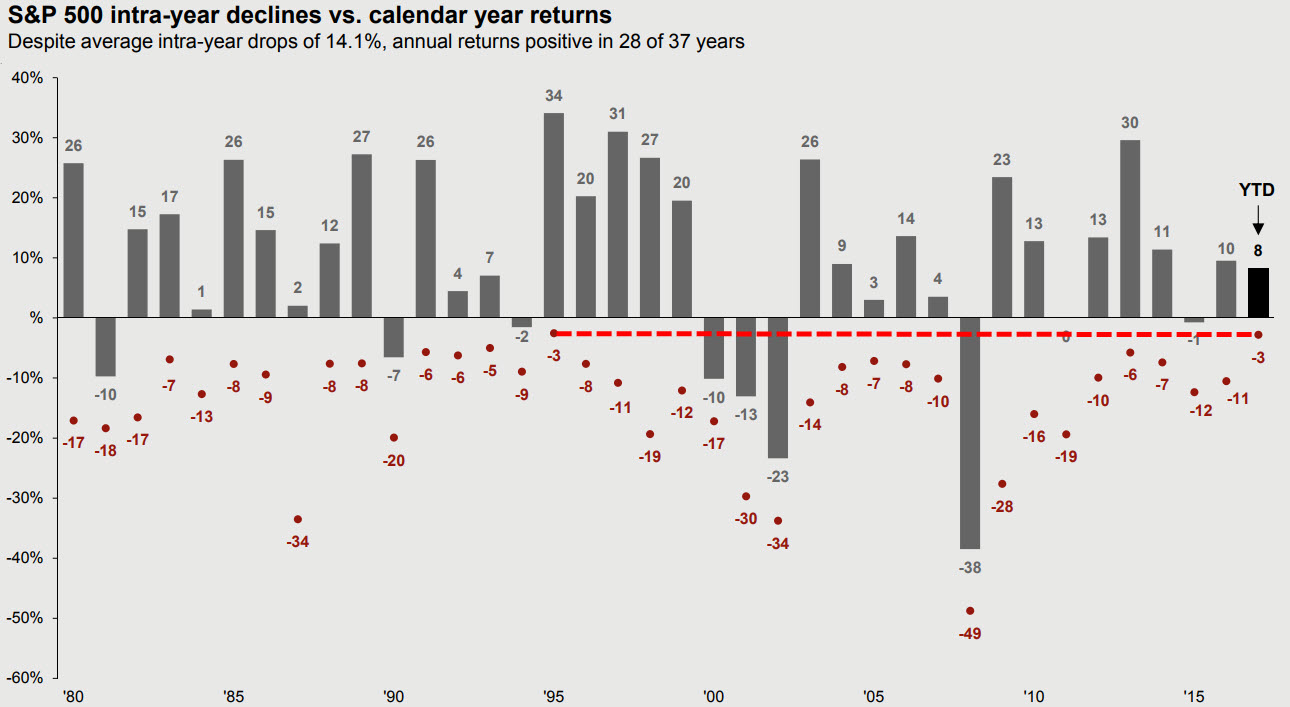

“For dip-buyers in the S&P 500, 2017 has actually been a tough year… because there hasn’t been any. As JPMorgan notes, 2017’s 3% intra-year decline is the smallest since 1980 (tied with 1995 which saw a 34% return)”

“This 3% drawdown (for now), continues a 6-year streak of drawdowns that are dramatically below the longer-term average of 14.1% drops intra-year.”

The question is what happens when the Federal Reserves quits injecting capital into the market through reinvestment and begins to allow their balance sheet to reduce? As I have noted previously, there is a very high correlation between those reinvestments and subsequent market action.

Secondly, the Fed has suddenly become concerned about valuation pressures. This is interesting given the Fed has not given valuations much concern previously suggesting the “low interest rates supported higher valuations.”

However, in the most recent release of their Monetary Policy Report for July, it was noted:

“Valuation pressures across a range of assets and several indicators of investor risk appetite have increased further since mid-February. However, these developments in asset markets have not been accompanied by increased leverage in the financial sector, according to available metrics, or increased borrowing in the nonfinancial sector. Household debt as a share of GDP continues to be subdued, and debt owed by nonfinancial businesses, although elevated, has been either flat or falling in the past two years.”

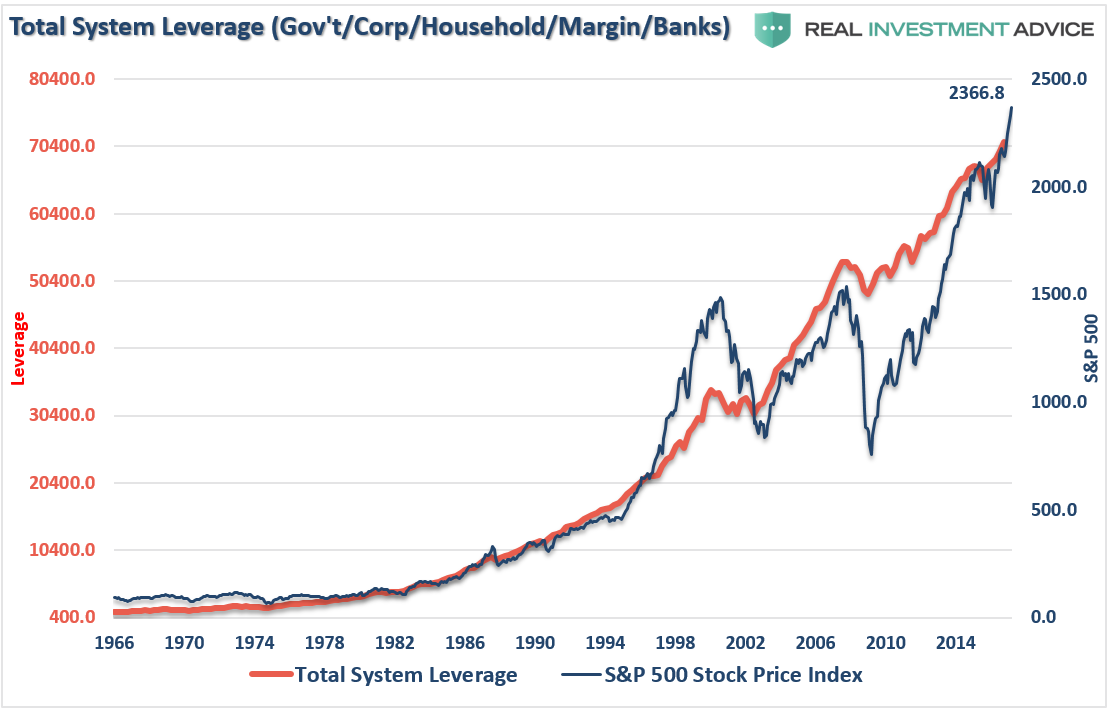

I am not sure exactly what debt metrics she’s looking at, but leverage is currently at the highest level on record.

Furthermore, even looking at the S&P 500, 400, 600 and Russell 2000 indices based on FORWARD OPERATING earnings estimates 2-YEARS into the future, I simply could not find a more generous measure of valuation, stocks are expensive. If EPS estimates fail to meet future expectations (which they always do) valuations will increase further.

Are stocks expensive? Yes.

Are companies and individuals heavily leveraged? You bet.

Will the outcome be benign? Probably not.

Lastly, while the “jobs report” was decent on Friday, with the exception of wage growth, it is important to remember two things:

- The employment report, along with all economic reports, are subject to heavy backward revisions, and;

- The “trend” is far more important than the actual number.

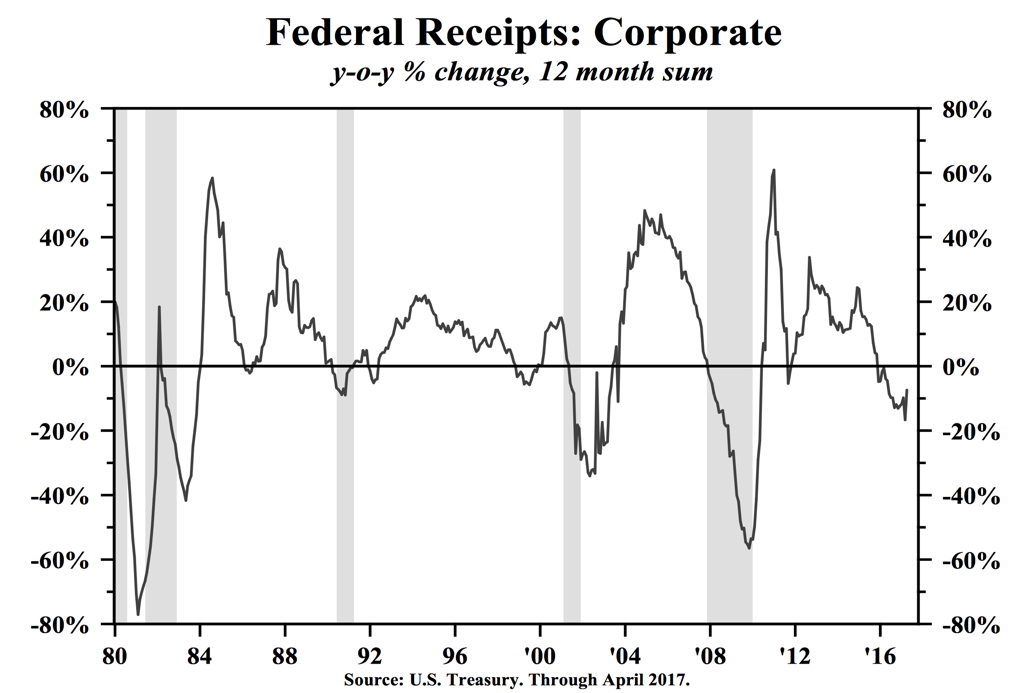

In regards to point 1) – the corporate tax receipts through April contracted the most since 2009. This suggests the macro corporate environment is weaker than currently believed and hiring generally does not “ramp up,” outside of temporary factors, if the overall environment is weak.

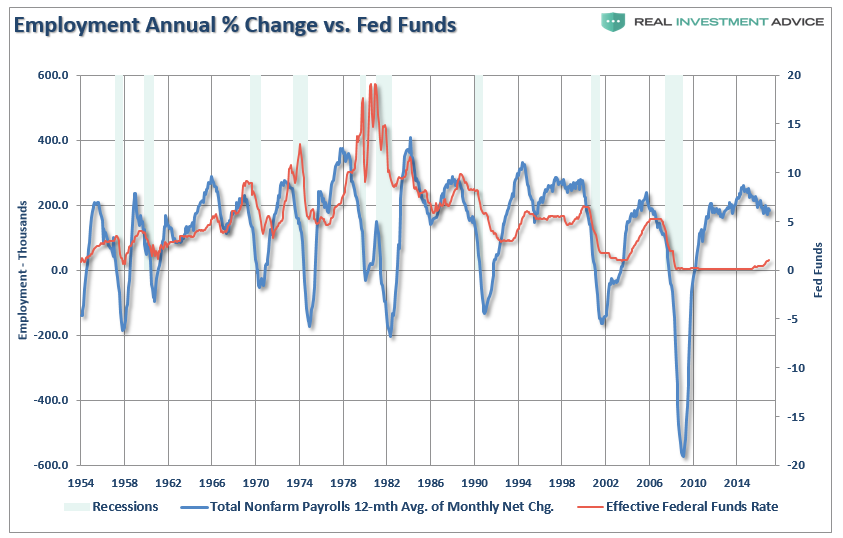

As to point 2), it should not come as a surprise the trend of employment has clearly begun to weaken. This has historically coincided with the Federal Reserve starting a rate hiking campaign which tightens monetary policy. Why everyone believes this time is different is beyond me?

As Dr. Lacy Hunt recently stated:

“When the Fed tightens, they are saying the economy is doing too well by our standards… we want the economy to have less money and credit growth and we want less economic activity. They are saying this at a time when the best economic indicators are in a downturn.’’

The Fed has likely got it wrong…again.