{kind=link}

Courtesy of Pam Martens.

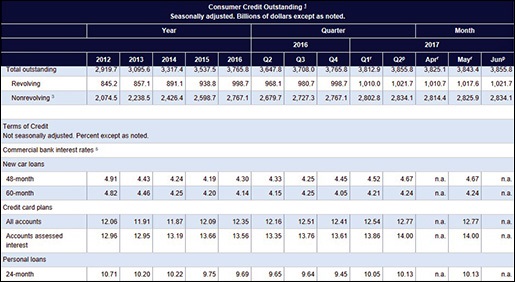

Source: Federal Reserve

By Pam Martens and Russ Martens: August 9, 2017

On August 7 the Federal Reserve released an updated report on consumer debt. It raises more questions about how the big Wall Street banks are making all those billions of dollars in profits.

Since 2012, the benchmark 10-year U.S. Treasury note has yielded below 2.5 percent for the majority of that period. But according to the Federal Reserve chart above, on all consumer credit card accounts assessed interest, the interest rate charged to consumers has moved from 12.96 percent in 2012 to 14 percent as of May 2017. (The 14 percent figure is defined as follows by the Fed: “The rate for accounts assessed interest is the annualized ratio of total finance charges at all reporting banks to the total average daily balances against which the finance charges were assessed (excludes accounts for which no finance charges were assessed).”

From 2012 to the end of the second quarter of 2017, total consumer debt has expanded from $2.9 trillion to $3.855 trillion on a seasonally adjusted basis, according to the latest Fed report.

One has to seriously question if the persistent subpar growth rate of 2 percent or less for the U.S. economy and the continuing closures of retail stores is directly related to the obscene interest rates being charged to U.S. consumers by the mega Wall Street banks that hold the majority of credit card debt. The 14 percent average rate blurs the fact that many consumers are being charged in excess of 20 percent on their credit cards. In a Town Hall speech in New York City on January 5, 2016, Senator Bernie Sanders had this to say about needed reforms to rein in Wall Street abuses:

…