What is the Carry Trade?

Courtesy of Eric Falkenstein’s Falkenblog

I recently mentioned the Carry Trade, and it wasn’t obvious what I was talking about, so here’s a short description. The Carry Trade in currency markets is when you borrow in the currency with the low interest rate, and then invest that in the currency with the higher interest rate. If the exchange rate does not change, this generates a positive return. Uncovered Interest Rate Parity is a theory that connects current to future spot rates. This theory states that you have two ways of investing, which should be equal. First, you can invest in your home country at the riskless rate. So if the US interest rate is 5%, you can make a 5% return in one year, in USD. Alternatively, you can buy, say, Yen, invest at the yen interest rate (each currency has a different risk-free rate), and then convert back to USD when your riskless security matures. For this to be equal, you need something like:

rusd=ryen + Appreciation in Yen

Where rusd is the US interest rate, etc. So, if you make 5% in USD, an American investor should receive that same return in yen, via the interest rate in yen, plus the expected appreciation/depreciation in the yen against the dollar. If the interest rate in yen is 1%, this means one expects the yen to appreciate by 4%. When the foreign interest rate is higher than the US interest rate, risk-neutral and rational US investors should expect the foreign currency to depreciate against the dollar by the difference between the two interest rates. This way, investors are indifferent between borrowing at home and lending abroad, or the converse. This is known as the uncovered interest rate parity condition, and it is violated in the data except in the case of very high inflation currencies. In practice higher foreign interest rates predict that foreign currencies appreciate against the dollar, making investing in higher interest rate countries win-win: you get appreciation on your currency, and higher riskless interest rates while in that currency.

Now the rates of expected return via the two investment paths can differ according to risk, so academics have been trying to explain this pattern via ‘risk’. So one can imagine, looking at the yen, or the dollar, or various European currencies in the 1970’s, etc., trying to tie each to some measure of a home currency’s risk factor: consumption, the stock market.

Like high returns to low volatility stocks, it is difficult, but not theoretically impossible, to make sense of the higher currency returns to high interest rate currencies. Robert Hodrick wrote a technical overview of the theory and evidence of currency markets in 1987. He summed up his findings in this paragraph:

We have found a rich set of empirical results… We do not yet have a model of expected returns that fits the data. International finance is no worse off in this respect than more traditional areas of finance.

Hodrick looked at CAPM models, latent variable models, conditional variance models, models that use expenditures on durables, or nondurables and services, Kalman filters. None outperformed the spot rate as a predictor of future currency prices. Hodrick leaves off with the idea that ‘simple models may not work well’.

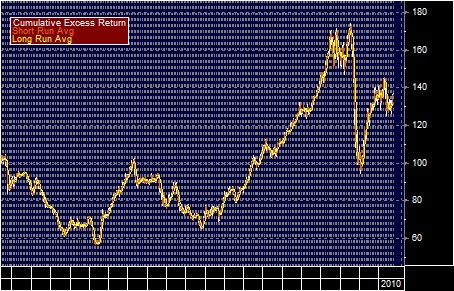

For the next 20 years, and many hedge funds specialized in the ‘carry trade’, which was as simple as it was successful: lend capital to high interest rate currencies, enjoy the high riskless rates and currency appreciation on the spot rate; borrow capital at the low interest rate currency, and make money on the depreciation of this debt over time. In 2008 these strategies suffered significantly, but the net effect is still there is no clear relation between risk and return in currencies. Below is the total return to going long the Australian dollar (a high interest rate currency) short the Yen (a low interest rate currency), from 1990 to 2010. Note on average it makes money (about 1.5%).

Brunnermeier, Nagel and Pedersen (2008) noted that

Overall, we argue that our findings call for new theoretical macroeconomic models in which risk premia are affected by funding and liquidity constraints, not just shocks to productivity, output, or the utility function.

What they mean is that the carry trade continued to work 30 years after being identified by Farber and Fama, and it has continued as a puzzle because no reasonable risk factor can explain it.