Credit Spreads:

A credit spread is implemented by simultaneously buying and selling options at two strike prices resulting in a credit to the investor. The investor is trying to sell the more expensive option and finance the purchase of the less expensive option by using part of the proceeds from the sale.

Let’s say the stock of ZUY is trading at $10. The $15 strike price call is priced at $3.00 and the $20 strike price call is priced at $1.00. If the investor sells the $15 strike price call at $3.00 and buys the $20 strike call for $1.00, the investor’s account is credited $2.00 per contract? (A call option consists of a contract for 100 shares of stock.) If the investor sells 10 contracts (buys 10 calls with strike price of 20 and sells 10 calls with strike price of 15),, he is credited with $2000 in his account (each contract being for 100 shares of stock). The risk of the trade is the difference between the two strike prices multiplied by the number of contracts multiplied by 100 less the credit received. For this example –

Strike price difference is $5, i.e., $20 – $15 = $5

Number of contracts 10 (each contract controlling 100 shares of stock)

Risk = $5 * 10 *(100) = $5000

Total Risk = $5000 – $2000 (credit received) = $3000

Technically no matter what happens to this trade the investor cannot lose more than $3000.

Please note the credit spread can be constructed for either Calls or Puts.

A call credit spread established at the top of the prevailing price of the instrument of choice is called a Bear Call Spread because we do not want the stock or index to breach the short (sold) call of the spread, i.e. in this example, we do not want the stock to go above $15 – the strike price of our sold calls. The Put credit spread established at the lower price range of the prevailing price is called a Bull Put spread, so named because the desired outcome is that the stock or index of choice does not fall to the point where it breaches the short put of the spread.

Iron Condor:

An Iron Condor is a combination of a Bear Call spread established on the top range of the stock or/index and a Bull Put spread at the bottom range of the stock or index. The goal is to establish a long enough range for both the Bear Call spread and the Bull Put spread and to set it up so that at the time of establishing the trade both spreads are close to being equidistant from the price of the instrument. In effect, we are trying to give the Condor a wide wing to enable the instrument of choice to oscillate back and forth during the duration of the trade but we do not want the price to breach either short option positions. The second goal is to establish the Iron Condor in a limited timeframe (5 weeks or less to expiration) so that time decay works in our favor. Technically, with each passing day that the stock or index does not move extremely in one direction or the other, the credit spread decays and the Iron Condor begins to show profitability.

Bear Call Spread

Sell RUT Jan 11 840 Call Quantity 55

Buy RUT Jan 11 850 Call Quantity 55

Bull Put Spread

Sell RUT Jan 11 685 Put Quantity 55

Buy RUT Jan 11 675 Put Quantity 55

The RUT index at the time of setup had a price of 770. This gives us a range of 70 points to the upside and 85 points to the downside before either short strike prices to be breached.

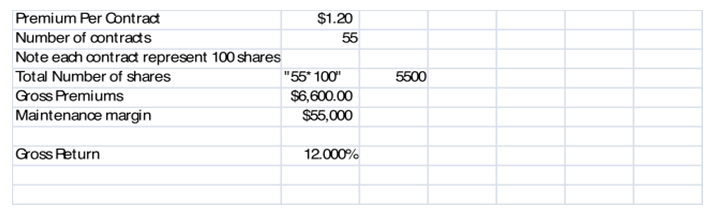

Gross premiums per contract is $1.20

From the above, if the index stays within our range for the duration of the trade, then we make a 12% return on our “maintenance margin.” (what do you mean by “maintenance margin”?), note: that the maintenance margin is the collateral or margin that your broker will require before allowing you to set up the trade.

Maintenance Margin

Even though you have two spreads, technically you can only lose in one direction and you should make sure your broker is not charging you separately for each spread. If you are charged separately for each spread this will significantly reduce your return and take up too much of your trading or investment capital. Your maintenance margin should be calculated by taking the difference in strike price for just one leg of the spread multiplied by the number of contracts

For the above example we arrive at our maintenance margin by subtracting either our call spread strike prices (850-840 =10) or our Put spread strike price (685-675 =10) then multiplying by the number of contracts/shares (10*5500 =$55,000).

If you your broker requires maintenance margin on both sides of the spread this will result in twice the amount required in this case $110,000, which will tie up significant amounts of capital and reduce your return by half form 12% to 6%.