Courtesy of The Automatic Earth

A low thunder rolling ‘cross the plains

"Workers in a tobacco field, Puerto Rico; The straw shed in the background is a hurricane shelter"

Ilargi: It’s hard sometimes, and potentially unrewarding too, to write about topics where you know beforehand that a significant part of the data will need to remain opaque by default, and then still feel like you need to address them. As my regular readers know, I’ve talked about derivatives, CDS in particular, quite a bit recently in connection with the Greek restructuring, default, reprofiling (pick your own term and color the pictures), see for instance The Derivatives Pressure Cooker and Credit Downgrade Swaps.

After publishing the last piece I received a very nice email form Mike ‘Mish’ Shedlock, which very simply said: "Very Good". I thanked Mish for the kind words, and said: "I’m sometimes getting the feeling I’m kind of alone in hammering on about the role derivatives play in all this." Mish pointed me to an article he wrote the same day, June 15, in which he quoted Kash at Street Light, who on Monday June 13 wrote:

Indirect US Exposure to the Euro Debt Crisis, part 2

[..] Unfortunately, it’s very difficult to get any good information about banks’ derivatives exposures. The major US banks tend to downplay their exposure to the Euro debt crisis in their SEC filings.[..]

The aggregate CDS exposures of the big US banks are certainly large enough to be plausibly consistent with the BIS estimate of about $100 bn in indirect exposures to peripheral Europe.[..] … it seems reasonable to guess that the total net open positions on CDS protection sold to third parties by the big US banks is between $1,500 and $2,000 billion.

Ilargi: At least that’s something. But I still don’t think it’s the real story. And frustrating as it might be to be always left with incomplete sets of numbers, because derivatives are largely dealt over the counter, meaning no-one’s keeping track of anything, I noticed some news items today that merit further scrutiny.

Derivatives are the $800 trillion or more gorilla in today’s financial room. There would very and quite simply not be anything remotely approaching the tense talks on Greek debt that we see if not for the derivatives exposure of some of the main parties involved in these talks. It’s not about a handful of billions of dollars the IMF will or will not fork over; that’s what these guys literally pay for their peanuts. The problem lies in the bets, the wagers, in the shape of default swaps, to the tune of trillions of dollars, that are out there, and that risk being triggered by a default being declared a "credit event", either by the ratings agencies, or the International Swaps and Derivatives Association, or both.

A mjaor part of this is that nobody knows how big this is. There are estimates of the total derivatives market flying around, but they are to a large extent private deals, for which there’s no all-encompassing clearing house. How large is that part? Well, we don’t know, do we? The overall derivatives market was estimated at one point by the Bank for International Settlements to be over $1 quadrillion. Lately I see numbers in the vicinity of $600 trillion. But have really that many of these contracts been wound down, and no new ones engaged in? I find that hard to believe, I don’t see why or how any of this would have been wound down, but I don’t know anymore than anyone else does.

So let’s get to those news items I mentioned. A British consulting firm, Fathom Financial Consulting, released a report ostensibly based on numbers provided by the UK Department of Business, that claims British banks could be on the hook in the Greek crisis for £366 billion, or $590 billion. That’s a very far cry from the $8 or $10 billion or so commonly reported in actual bond holdings. It’s equivalent to about £14,640 , or $23,5000, per British family, a quarter of the yearly GDP. And that’s just for Greece! Shit, guys that’s just Britain, and it’s just Greece. Let that sink in.

By way of comparison, French banks have an exposure to Greece in direct holdings that’s about 4 times as big as their UK counterparts. Does that mean France could lose $2.36 trillion in case of a Greek default? Who’s to know? And who knows anything about Fathom Financial Consulting anyway? Still, their report is interesting in that it’s (one of) the first that tries to incorporate derivatives into the total exposure numbers for financial institutions. And we need that kind if data, badly. Shaken AND strirred, please.

Second news item: The New York Times published an editorial today, and what is the subject? You guessed it, derivatives.

The euro-zone bailout of Greece is, in good part, a bailout of European banks. In France and Germany alone, banks hold some $90 billion worth of public and private Greek debt. The European Central Bank also holds Greek government debt, and the fear is that if Greece defaults, cascading losses could threaten all of Europe.

Are American banks also vulnerable? No one is sure. They are not big lenders to Greece, but they are big players in the derivatives markets. If Greece defaulted, a European bank holding a credit-default swap on Greek debt from an American bank would be entitled to a payout from that bank.

Credit-default swaps are the kind of derivatives that were behind the blowup of the American International Group and the near meltdown that followed in the global financial system. From the available evidence, it doesn’t appear that a Greek default would have the same destructive power, but no one is eager to test the proposition.

In his recent confirmation hearing to be the next leader of the European Central Bank, Mario Draghi, the central banker of Italy, warned that no one really knows who is on the hook for these risky financial instruments. “Who are the owners of credit-default swaps? Who has insured others against a default of the country?” he asked.

Warning of a potential “chain of contagion,” he argued against requiring banks to restructure Greek debt — which could involve extending repayment terms or writing off principal — even though Greece’s apparent inability to pay in full makes a restructuring all but inevitable. [..]

The uncertainty is greater when you consider that credit-default swaps are only one type of derivative that links banks worldwide. What dangers lurk in other derivatives, like those on currencies and foreign exchanges?

Ilargi: If nothing else, the NYT editorial staff confirm what I’ve been harping on for some time now: It’s about the derivatives, stupid! Why they chose today to -finally- address the issue is anybody’s guess. Perhaps they want their readers to understand that last night’s confidence vote in Athens means nothing: next week’s austerity vote (June 28) is a much bigger deal. Or perhaps it’s just a simple swipe at Republicans for stalling reform and regulation. "Republican lawmakers are bent on derailing reform by any means necessary, including starving regulatory budgets, impeding the confirmation of regulatory nominees and pressing regulators to adopt light-touch rules." Yeah, right, doh!, who’s in charge again?

Third news item. Harry Wilson at the Telegraph reports that the International Swaps and Derivatives Association (ISDA) has declared a credit event at Allied Irish Bank:

Allied Irish Bank has ‘defaulted’ says derivatives body

Banks that sold insurance on the debt of Allied Irish Banks will have to pay out to investors in the nationalised lender’s debt despite complex legal manoeuvres by the Irish authorities to avoid putting the lender into default.

The International Swaps and Derivatives Association (ISDA) yesterday said that a "credit event" had occurred on Allied debt, meaning the bank has effectively defaulted on its debt, a situation the Irish government has gone to extreme lengths to avoid. Credit default swaps (CDS) sold on Allied subordinated bonds and, crucially, its senior debt, have been activated by the decision of the ISDA determinations committee that decides whether a borrower has defaulted. [..]

While the Allied decision was in line with market expectations and covers only a relatively small number of bonds, it sets a precedent for upcoming decisions on Bank of Ireland debt that is likely to be more significant as the lender is the last major Irish bank not to be fully nationalised.

Of even more significance will be the read-across for CDS contracts written on Greek government debt and that of other indebted European governments. With a default by the Greek government regarded by most investors as a certainty, the issue is likely to become one of determining whether the form of the default allows holders of the bonds to exercise the CDS protection they have taken out on the bonds.

"There could be a big wake-up call here for investors. People still do not understand that a CDS credit event and default are two completely separate things," said one London-based credit trader.

Ilargi: Hmm. CDS payments due on Allied irish. We have no clue, nobody does, how much money is involved here. But don’t be surprised if it’s enough to bankrupt a bank or two or three. I’m not saying that wlll happen, just that the amounts involved may well be sufficient to trigger such events, if left alone. Whether it will actually come about depends on talks like the ones that have been going on in Athens for the last, eh, what, forever?!

But the game is on, and on the wagon, so to speak. As the NYT editors said: "[..] credit-default swaps are only one type of derivative that links banks worldwide". In other words, having to pay out on Allied Irish CDS can push the same banks over the edge that are counterparties to Greek CDS, and so on and so forth. And again, I’ve said it before: these things were never meant to pay out. They were designed to hide debt, to allow financial institutions to use their capital for further bets and wagers. AIG was once the biggest of the lot; TARP and QE2 have served, to the tune of, what, $2 trillion now?!, not even to pay off what’s owed, but just to keep a lid on things.

It’s starting to look like that "CDS to hide debt" idea might be backfiring. But, then again, all the Merkels and Obamas and Papandreous and Geithners and Junckers on this planet will try with all their might to prevent that from happening. And they have virtually limitless access to your money, and that of your children, to do just that. They have exactly zero chance of succeeding, but that won’t keep them from trying: their jobs, their social status, perhaps even their very lives depend on it.

There’s a low thunder rolling across the plains, and it’s coming this way. There’s nowhere to hide; we’ll have to live through it. It’s called debt deflation. Derivative debt deflation. Financial crisis? You ain’t seen nothing yet.

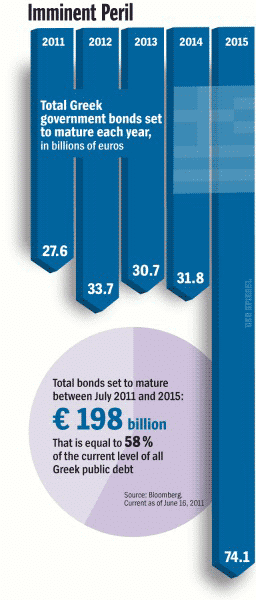

And since pictures say more than a trillion dollars’ worth of words, I thought I’d leave you with this one from Der Spiegel. From this, please draw your own conclusions on the future of Greece, the Eurozone, and all the derivatives written on them by all the banks in the world. C’mon, you can do it, it ain’t hard.

Reading List (click here for full length articles)

Britain could be hit with losses of up to £366billion from the collapse of the Greek economy, it has emerged. The potential devastation of banks and other City institutions would be equal to 24 per cent of our annual national output, or £14,640 for every family in the UK.

Allied Irish Bank has ‘defaulted’ says derivatives body

by Harry Wilson – Telegraph

Banks that sold insurance on the debt of Allied Irish Banks will have to pay out to investors in the nationalised lender’s debt despite complex legal manoeuvres by the Irish authorities to avoid putting the lender into default.

The International Swaps and Derivatives Association (ISDA) yesterday said that a "credit event" had occurred on Allied debt, meaning the bank has effectively defaulted on its debt, a situation the Irish government has gone to extreme lengths to avoid. Credit default swaps (CDS) sold on Allied subordinated bonds and, crucially, its senior debt, have been activated by the decision of the ISDA determinations committee that decides whether a borrower has defaulted.

Greece and You

by NYTimes Editorial

The euro-zone bailout of Greece is, in good part, a bailout of European banks. In France and Germany alone, banks hold some $90 billion worth of public and private Greek debt. The European Central Bank also holds Greek government debt, and the fear is that if Greece defaults, cascading losses could threaten all of Europe.

Greek Prime Minister Giorgios Papandreou survived a confidence vote on Tuesday night. But the battle against national bankruptcy will get no easier in the coming weeks. Protests indicate that opposition to his austerity path is growing and he faces a crucial vote next week.

EU urged to block Greece bail-out

by Louise Armitstead – Telegraph

European leaders have been urged to scrap plans for a second Greek bail-out – as the Athens government wins a critical vote of confidence in parliament.

Leading London-based think tank Open Europe has claimed that a fresh bail-out, expected to be around €120bn (£106bn), will almost triple taxpayers’ existing exposure to Greek debt. “Despite a second Greek bail-out being EU leaders’ preferred option, it is only likely to increase the economic and political cost of the eurozone crisis,” said Open Europe in a report.

Europe’s Dangerous Leap of Faith

by David Böcking and Carsten Volkery – Spiegel

When it comes to the euro crisis, Europe means business. That, at least, is the message sent by the decision to withhold a vital aid tranche until Greece passes a far-reaching austerity package next week. But the move could backfire.

One could be forgiven for thinking that hurdle races, long an Olympic discipline, originated in Greece rather than in England. Particularly these days. Prime Minister Giorgios Papandreou is doing all he can to keep his government together and prevent his country from going bankrupt. But the obstacles — a full year after the European Union and the International Monetary Fund put together a €110 billion aid package for the country — are myriad. And high.

Greece will get its next quarterly installment of bailout money only if the country’s Parliament passes a contentious package of budget measures, European finance ministers said after a two-day meeting in Luxembourg. They also made long-planned changes to the euro zone’s bailout funds.

Greek debt crisis: Straw says eurozone ‘will collapse’

by BBC

Jack Straw has predicted the collapse of the eurozone and urged the UK to consider the "alternatives" as the Greek debt crisis worsens. The Labour MP and former foreign secretary said the euro was facing a "slow death" and the 17-member eurozone "cannot last" in its current form. He was speaking as MPs discussed the prospect of a fresh bailout for Greece.

IMF ties Greek aid to bail-out pledges

by Peter Spiegel – Financial Times

The International Monetary Fund is blocking a critical €12bn ($17bn) aid payment to Greece just weeks before it is due, insisting it cannot go through without concrete assurances from European officials on a new Greek bail-out.

European finance ministers went into a meeting on Sunday believing the two issues had been separated and that the payment would go ahead as planned in early July once a new austerity plan was approved by the Greek parliament. Recent public commitments stating the EU would ensure Greece remains solvent through next year were thought to be enough to secure the backing of the IMF, due to disburse €3.3bn of the aid payment.

Greek Banks Feel Hostage to Debt Crisis

by Jack Ewing – New York Times

A whiff of tear gas still lingered outside the downtown headquarters of Piraeus Bank last week, a souvenir of clashes between the police and demonstrators in front of the nearby Parliament building. It was a fitting metaphor for the way that Greek financial institutions have been trapped in the middle of their country’s turmoil.

The funding gap faced by local government pension schemes in England has grown to £71.5bn, new research has revealed, despite a rally in equity markets boosting returns on investments.

Japan pensions bet on hedge funds to boost returns

by Chikafumi Hodo and Nishant Kumar – Reuters

Japan’s corporate pension funds, hobbled by a sluggish domestic stock market, are raising their allocations to hedge funds as they scramble to boost returns for the country’s aging population.

The move is part of a broader trend in Asia where institutions are looking to raise exposure to hedge funds in search for absolute positive returns and as confidence in the asset class improves, lifting prospects for the $2 trillion global hedge fund industry. Nearly all of Japan’s corporate pension funds, which collectively manage more than $900 billion, have lowered their guaranteed yield in the last decade from about 5.5 percent to below 3.5 percent on average, industry observers said.

Pension changes heading for ‘car crash’

by Nicholas Timmins

Government plans requiring employers to start enrolling their employees automatically into a pension scheme are heading for a “car crash”, a leading firm of actuaries and pension consultants has warned. A survey of finance and human resources directors at some of Britain’s biggest companies – the ones which will have to start auto-enrolment in October next year – shows that 40 per cent of finance directors are not aware of the deadline.

Three heavy hitter Republican senators have put forward a plan to restructure Social Security. Lindsey Graham (R-SC), Mike Lee (R-UT) and Rand Paul (R-KY) have sponsored the Social Security Solvency and Sustainability Act, S. 804.

Overall, I give this plan a “C”. That grade is composed of two distinctly different analyses. On the pure question of economics, I give the plan a “B”. But on the more critical issue of “Is this fair” I give the plan a “D”.