Courtesy of The Automatic Earth

Ben Glaha Cascade June 1941 "Parker Dam power project. View from California side into Arizona"

Ilargi: After having maintained for the past few years that Greece neither could nor would be allowed to default, EU leaders have finally given in. Of course, the word now is that this can be a default that doesn’t trigger a credit event, in which payments on credit default swaps come due. Good luck with that. The credibility of Europe in the financial markets is shot. Gone. Trillions more in taxpayer funds will be thrown at the issues, but it doesn’t matter anymore.

Not coincidentally, the change in attitude on Greece comes at a time when Italy has come under intense pressure. It’s time to cut losses. Getting Greece done will open up space and time to "save" Italy. Or so undoubtedly goes the reasoning. It’s not going to work.

Italy is not the EU periphery; Italy is very much in the heart of Europe. The country’s nominal GDP is over $2 trillion. And its debts are staggeringly high. As Ambrose Evans-Pritchard writes for the Telegraph:

Italy and Spain must pray for a miracle

Once again Europe’s debt crisis has metastasized, and once again the financial authorities face systemic contagion unless they take immediate and dramatic action. If the ECB’s Jean-Claude Trichet is right in claiming that Europe was on the brink of a 1930s financial cataclysm a year ago – and I think he is – it is hard see how the threat is any less serious right now.

Fall-out from Greece flattened Portugal and Ireland last week. It is engulfing Spain and Italy, countries with €6.3 trillion ($9 trillion) of public and private debt between them.

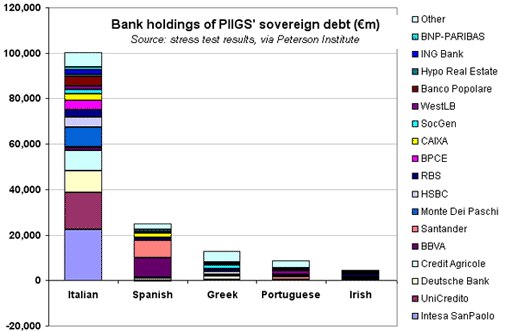

Ilargi: Holders of this debt are first, of course, Italian banks, as this graph shows. The two last banks in the row, Unicredit and SanPaolo, hold some 40% of Italian sovereign debt. In the past few days, trading in Milan was temporarily halted for both, albeit at different times.

Obviously, this graph shines a light on other things as well. For one, European banks’ holdings of Italian debt is 7-8 times bigger than that of Greece. Where it’s taken European leaders forever to accept, as they did today, that there will have to be haircuts for private investors. When time comes to address Italy’s debt, "haircut" won’t be an appropriate metaphor. It’ll be more like putting their heads through a lawnmower, and without anaesthetics.

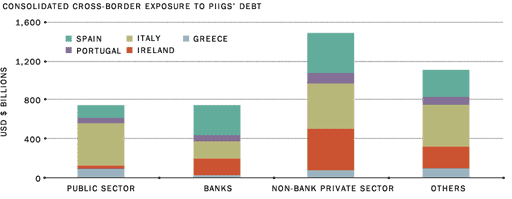

If we broaden our scope to look beyond banks, and include other institutional investors in PIIGS debt, this is the picture we get:

Graph: Federal Reserve Bank of St. Louis

Clearly, it’s not just the banks that will get hammered (or lawnmowered) . Pension funds, insurance companies etc. are right up there with them. Total "cross-border" exposure then looks as follows:

That’s a neat $3.23 trillion right there. In sovereign debt. The EU bail-out fund is presently about $700 billion, and Germany has stated that enlarging it is out of the question.

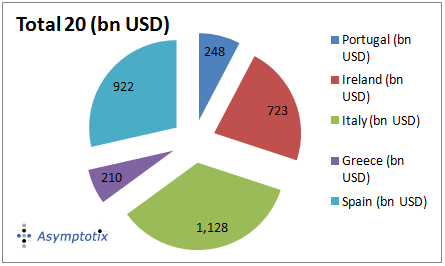

Another interesting graph is this one:

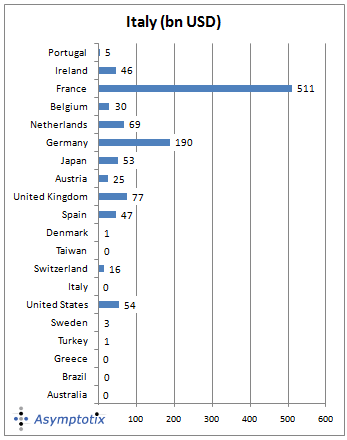

As you see, French banks have a completely outsized exposure to Italy. Which means that if the markets come after Rome, they’ll hit Société Générale, BNP Paribas and Crédit Agricole too. There’s no way they won’t. Here’s the overall PIIGS exposure for banks per country:

Paris will -need to- step in to try and save its financial institutions. The first steps in that direction are already being taken. The International Accounting Standards Board (IASB) has advised Europe to implement their International Financial Reporting Standard 9 (IFRS 9), which is nothing but a sly and underhanded mark to fantasy trick posing as a "standard". Think the US’ FASB 157. Basically, IFRS 9 allows investors to hold assets at cost as long as they don’t try and sell them. That Greek haircut which is being discussed shaves off as much as 60% of debt value. But they may still appear on the books at 100%.

That’s really great. Unless you would like to know what your shares are really worth, and those your pension fund holds. Who needs transparency, or reality, when you can just spend your days dreaming of riches? We’re all crackheads now.

Another shrewd European plan that has France written all over it is this one, as reported by Reuters:

‘EU taxpayers to rescue bank test failures’

European countries will support banks that fail stress tests if those lenders cannot raise capital from investors within six months, according to a draft EU document seen by Reuters. The paper, being prepared for EU finance ministers to approve on Tuesday, is an about-face from promises by G20 policymakers in the wake of the financial crisis that taxpayers would never have to bail out banks again.

The European Banking Authority is due to announce next week the results of its latest stress tests of the region’s top lenders – 91 in all – in another attempt to reassure investors that European banks have been rebuilt against future shocks.

Ilargi: A third of the 91 stress-tested banks is believed to fail. Greek and Italian banks will be among them, some German, but looking at the graphs above is should be clear that it’s the main French powerhouses that deserve our scrutiny.

There is no way the EU/ECB/IMF troika can save Italy if and when it comes under too much pressure. Pretending that it can is useless, but a valiant effort to do just that will be made. By then, however, Greece will have been fed to the dogs. And judging from the amounts of exposure to Ireland, Dublin looks like a lost case too. Moreover, there is no reason the markets won’t come after Spain at the same time as Italy.

And then they can focus on France. This may sound far-fetched today, but that’s just a temporary notion. Remember, total public and private debt for Italy and Spain is €6.3 trillion, or $9 trillion. For just these two countries. And a lot of that is hiding in the vaults of the French banks.

The best thing to do would be to come clean, to mark all assets to market, to restructure what must be restructured, and to bankrupt those institutions that are in fact bankrupt. This will not be done. Instead, extend and pretend will be the official policy -though it will be called something else-, until it no longer can be. That’s what happened with Greece today: the official line went from "no defaults" to "sure, defaults, but…" in five seconds flat.

And that is the future for Italy too. And Ireland, Spain, Portugal. And after that France may have its turn. By then, though, the EU may have stopped functioning as a unit. Berlin, Paris and Amsterdam will reach a point where they’ll throw anyone at the wolves who threatens their positions. Not that that will do a single thing to save them; it will merely prolong the agony. Alternatively, there will probably be attempts at creating a true fiscal union across Europe, or even a political one.

But that will never come to be. It’s game over. The European leadership, having lost every inch of its credibility in the marketplace, is like the check player who refuses to admit defeat and insists on playing on and on even when the odds of winning are zero. Investors love it: they will get fed trillions of euros more in public funds, until that same public says "no mas".

Greece set to default on massive debt burden, European leaders concede

by Ian Traynor – Guardian

European leaders bowed to the inevitable and conceded that Greece is likely to default on its massive debt burden, which would be a first among the 17 countries using the euro. They also abruptly shifted tack in the eurozone debt crisis by raising the possibility of using the eurozone’s bailout fund to buy back Greek debt on the markets, meaning sizeable losses for Greece’s private investors and reduced debt levels for Athens.

Following 12 hours of fraught negotiations in Brussels haunted by the risks of contagion in the eurozone spreading to Italy, now being targeted by the financial markets for the first time in the 18-month crisis, the 17 governments of the eurozone pointedly failed to rule out a sovereign debt default by Greece.

European leaders are for the first time prepared to accept that Athens should default on some of its bonds as part of a new bail-out plan for Greece that would put the country’s overall debt levels on a sustainable footing.

The new strategy, to be discussed at a Brussels meeting of eurozone finance ministers on Monday, could also include new concessions by Greece’s European lenders to reduce Athens’ debt, such as further lowering interest rates on bail-out loans and a broad-based bond buyback programme.

It also marks the possible abandonment of a French-backed plan for banks to roll-over their Greek debt. "The basic goal is to reduce the debt burden of Greece both through actions of the private sector and the public sector," said one senior European official involved in negotiations.

German ‘Nein’ leaves Italy and Spain in turmoil

by Ambrose Evans-Pritchard – Telegraph

Italian and Spanish bond yields soared to post-EMU highs in a fresh day of credit turmoil after Germany blocked any meaningful measures to defuse the crisis.

Chancellor Angela Merkel called for more "frugality" in Italy, sticking to her script that Rome can solve its woes with an austerity budget. Her finance minister Wolfgang Schäuble said any boost to the EU’s €500bn (£440bn) bail-out machinery was "out of the question". Mr Schäuble denied reports that Berlin was ready to empower the fund to purchase Spanish and Italian bonds pre-emptively on the open market, a move seen by experts as vital to halt dangerous contagion to the larger economies.

The market’s verdict on EU foot-dragging was instant and brutal. Yields on 10-year Spanish bonds smashed through the 6pc barrier for the first time since 1997, made worse by warnings from the Castilla-La Mancha region that its deficit had become "extremely serious".

US hedge funds bet against Italian bonds

by Dan McCrum – Financial Times

US hedge funds are placing large bets against the value of Italian government debt, directly shorting the bonds of the eurozone’s third largest economy. The funds have increased the size of short positions in the last month, speculating that investor concerns over the country’s ability to fund itself may spread from Europe’s periphery to Italy, according to investors in the funds briefed on the strategy.

On Friday, yields on Italian government debt – the largest bond market in Europe – hit their highest levels since October 2002. Italy is now borrowing at its biggest premium over German bunds, the benchmark for the region. The move followed the surfacing last week of tensions between Silvio Berlusconi, prime minister, and Giulio Tremonti, Italy’s finance minister, over the country’s proposed austerity programme.

Italy Orders Short Sellers to Reveal Positions After Market Dip

by Lorenzo Totaro – Bloomberg

Italy’s financial-market regulator moved to curb short selling after the country’s benchmark stock index fell the most in almost five months and bonds tumbled on investor concern Italy would be the next victim of the region’s debt crisis.

The regulator known as Consob ordered last night that short sellers must reveal their positions when they reach 0.2 percent or more of a company’s capital and then make additional filings for each additional 0.1 percent. The measure takes effect today and lasts until Sept. 9.

‘EU taxpayers to rescue bank test failures’

by Reuters

European countries will support banks that fail stress tests if those lenders cannot raise capital from investors within six months, according to a draft EU document seen by Reuters. The paper, being prepared for EU finance ministers to approve on Tuesday, is an about-face from promises by G20 policymakers in the wake of the financial crisis that taxpayers would never have to bail out banks again.

The European Banking Authority is due to announce next week the results of its latest stress tests of the region’s top lenders – 91 in all – in another attempt to reassure investors that European banks have been rebuilt against future shocks. This latest round of tests has been touted as being more rigorous than previous attempts in which few banks failed, and finance ministers’ officials are drawing up plans for how to deal with the fallout.

Fears Italian banks may fail stress tests

by Jill Treanor – Guardian

Italian banks on Friday bore the brunt of concerns about the financial health of Europe’s banking sector before official results of stress tests due on 15 July. Britain’s big banks – including bailed-out Royal Bank of Scotland and Lloyds Banking Group – are among 91 in Europe to have been subjected to the crisis scenarios drawn up by the European Banking Authority. While Britain’s banks are expected to pass the health check, Italian bank shares slumped amid concern they might need new capital and that the country may be dragged into the eurozone crisis.

Ratings agency Moody’s has already predicted that almost a third of the banks being tested might need some form of external support to bolster their capital. The focus turned to Italy on Friday when shares in the country’s biggest bank, UniCredit, were temporarily suspended amid anxiety it might need to raise fresh capital. It is the only major Italian bank that has yet to do so.

Merkel Urges Italy to Stick to Austerity Measures

by Spiegel

German Chancellor Angela Merkel on Monday responded to mounting investor concern over Italy by urging the country to pass its planned budget cuts to help restore confidence. Merkel said "Germany and all euro partners are steadfastly determined to defend the stability of the euro."

German Chancellor Angela Merkel urged Italy on Monday to pass an austerity budget to demonstrate that it is undertaking the reforms needed to restore confidence in the euro zone, as the currency slid against the dollar on concerns that Italy could be the next nation to fall victim to the debt crisis.

"Italy must itself send an important signal by agreeing on a budget that meets the need for frugality and consolidation," she told a joint news conference with Icelandic Prime Minister Johana Sigurdardottir in Berlin. "I have full confidence that the Italian government will pass exactly this kind of budget, I discussed this yesterday with the Italian premier," said Merkel.

The global economy faces a unique double threat. The eurozone, of course, remains on the brink of a major, perhaps terminal, crisis. Then there’s the small matter of the US Congress possibly "closing down" the government of the largest economy on Earth.

Although separate, these dangers are intimately related. Both have their roots in grotesque and utterly unsustainable levels of government debt. For it’s the massive sovereign liabilities not just of the eurozone "periphery", but some of the "core" nations too, that could yet cause the single currency to break up – an end-game "cranks" like me have been predicting for almost 20 years, but which now even the most slavish Europhiles must accept is possible. A "euroquake", were it to happen, would send financial shockwaves across the world.

Don’t blame Moody’s for a messy euro crisis

by Wolfgang Münchau – Financial Times

You can always gauge the temperature of the eurozone crisis by the blame game. Last week, the cacophony briefly subsided when everybody who mattered accused the rating agencies of engaging in an anti-European conspiracy. This was the day after Moody’s downgraded Portugal to junk. The fury of the reaction tells me that the process is in real trouble, once again.

The most interesting aspect of Moody’s rating was not the downgrade itself, but the reasoning. Moody’s expects that Portugal, like Greece, will need another loan. Moody’s also expects that the politics will be just as messy. Will not the Germans again seek private-sector participation as a condition? Of course they will. Moody’s concluded, rightly in my view, that the messy European Union politics constitutes a reason for concern. Having observed this crisis from the start, I agree. This is as much a crisis of policy co-ordination as it is a debt crisis.

EU calls emergency meeting as crisis stalks Italy

by Luke Baker – Reuters

European Council President Herman Van Rompuy has called an emergency meeting of top officials dealing with the euro zone debt crisis for Monday morning, reflecting concern that the crisis could spread to Italy, the region’s third largest economy.

European Central Bank President Jean-Claude Trichet will attend the meeting along with Jean-Claude Juncker, chairman of the region’s finance ministers, European Commission President Jose Manuel Barroso and Olli Rehn, the economic and monetary affairs commissioner, three official sources told Reuters.

Italy and Spain must pray for a miracle

by Ambrose Evans-Pritchard – Telegraph

Once again Europe’s debt crisis has metastasized, and once again the financial authorities face systemic contagion unless they take immediate and dramatic action.

If the ECB’s Jean-Claude Trichet is right in claiming that Europe was on the brink of a 1930s financial cataclysm a year ago – and I think he is – it is hard see how the threat is any less serious right now.

Worries Grow Over US Jobs

by Justin Lahart and Joe Light – Wall Street Journal

The U.S. economy added painfully few jobs for the second month in a row, undermining hopes that the sluggish recovery was getting back on track, depressing financial markets and putting new pressure on policy makers to come to the rescue.

The government’s broadest snapshot of employment showed the nation added just 18,000 jobs in June. Private-sector hiring slipped to its slowest pace in over a year, and government continued shedding workers. May’s equally disappointing job-creation number was cut in half. The unemployment rate ticked up to 9.2%, from 9.1% in May. The report also showed that even more workers dropped out of the job market.

US Economy Faces a Jolt as Benefit Checks Run Out

by Motoko Rich – New York Times

An extraordinary amount of personal income is coming directly from the government.

Close to $2 of every $10 that went into Americans’ wallets last year were payments like jobless benefits, food stamps, Social Security and disability, according to an analysis by Moody’s Analytics. In states hit hard by the downturn, like Arizona, Florida, Michigan and Ohio, residents derived even more of their income from the government.

The Housing Horror Show Is Worse Than You Think

by Roben Farzad – Businessweek

Despite some upbeat news, key housing market statistics point to years of stagnation

You might be tempted to believe that after four years of brutal declines in home prices, the worst of the crisis is over. The Standard & Poor’s/Case-Shiller 20-city index of prices has fallen back to where it was in 2003. Housing prices in Phoenix are at 2000 levels, and Las Vegas is revisiting 1999.

Lower prices have made homes more affordable than they’ve been in a generation, and sales have gone up in six of the past nine months. "It’s very unlikely that we will see a significant further decline" in prices, Housing and Urban Development Secretary Shaun Donovan said in a July 3 appearance on CNN. "The real question is, when will we start to see sustainable increases? Some think it will be as early as the end of this summer or this fall."

Lawmakers Mulling Fate of Fannie and Freddie Split on U.S. Role

by Lorraine Woellert – Bloomberg

The U.S. housing industry is finding political traction in Congress as it objects to plans that would wind down Fannie Mae and Freddie Mac and eliminate any government role in mortgage finance.

Two members of the House Financial Services Committee, Gary Miller, a California Republican, and Carolyn McCarthy, a New York Democrat, today introduced legislation to create a government-run replacement for the two mortgage finance companies, which originally were chartered by Congress.

The measure directly challenges House Republican leaders, who have backed bills that would do away with the two companies and aim to minimize the risk that taxpayers will have to bail out future mortgage failures.

US public pensions face accounting overhaul

by Dan McCrum and Nicole Bullock- Financial Times

Proposals to improve the way US state and local governments report pension liabilities were published on Friday in response to mounting concerns about shortfalls.

Public pensions have become a topic of debate, pitting lawmakers against public worker unions in tough negotiations over how to close gaps that are forecast to top $2,000bn by observers using more conservative accounting standards than are now recommended. The Governmental Accounting Standards Board has proposed that pension funds should use much more conservative assumptions under certain circumstances.

Defaulting rescued Argentina. It could work for Athens too

by Heather Stewart – Observer

Struggling under an impossible burden after its IMF bailouts, Buenos Aires knew its one hope was to stop paying its debts and become a pariah – and so it proved

Protesters on the streets of Athens this summer have been brandishing banners depicting a panicky helicopter airlift. Not Saigon at the height of the Vietnam war, but Buenos Aires in 2001, when Fernando de la Rúa fled from the roof of his presidential palace to escape riots in the streets.

Argentina, stuck in a painful recession since 1998, had done everything the International Monetary Fund had told it to do. After several bailouts, the government imposed wave after wave of eye-watering austerity measures, as prescribed by the "Washington consensus", and sought a voluntary restructuring with its private sector creditors, all of which will sound familiar to the Greeks.

UK chain retailers ‘closing 20 stores a day’

by Zoe Wood – Guardian

The gravity of the high street downturn is spelled out in new research published on Friday which shows UK retail chains have been closing stores this year at a rate of about 20 a day. The alarming statistic comes as closing down sales at TJ Hughes’s 57 department stores get under way. The Liverpool-based chain went into administration last week, putting more than 4,000 jobs at risk.

The administrators, Ernst & Young, said they were holding talks with more than 30 prospective buyers, but analysts suggested the chain, nearly a century old, would be broken up and shops auctioned. Tom Jack of Ernst & Young said they were encouraged by the level of interest in TJ Hughes, but needed to sell the mountain of unsold stock sitting in its storerooms in case a buyer failed to materialise.

Southern Cross wind-up bid sees shares’ value wiped out

by Thisislondon.co.uk

Some of the City’s biggest institutions today saw the last part of what was a £1.1 billion investment disappear after struggling care homes group Southern Cross suspended its shares and set out plans to wind itself up.

Restructuring plans drawn up last month by Southern Cross and its 80 landlords aimed to see homes transferred to new operators by September. But today’s shock announcement sees the firm closing its entire operations.