Courtesy of The Automatic Earth

"Max Wiehle, son of the founder of the long-defunct Fairfax County, Va., hamlet of Wiehle Station, was a Washington, D.C., businessman who owned Potomac Sales, a car dealership”

Ilargi: The August 15 trading day closed to headlines such as this:

"[US] stocks jumped, posting the third consecutive gain and the best 3-day rally since March 2009…".

Sounds good, doesn’t it? But perhaps a wee bit of perspective is in order. Financials were up yesterday (Monday), but here’s what they look like over the medium term:

- Bank of America:

+7.93% Aug 15, but -22.4% in past month, -34.95% in past 3 months - Citigroup:

+4.76% Aug 15, but -18.53% in past month, -24.71% in past 3 months - Morgan Stanley:

+6.10% Aug 15, but -15.03% in past month, -25.74% in past 3 months - Goldman Sachs:

+2.28% Aug 15, but -8.28% in past month, -15.79% in past 3 months - Société Générale:

+2.06% Aug 15, but -28.53% in past month, -41.23% in past 3 months

Reality is not quite the same, in other words, as the headlines. The "best 3-day rally since March 2009" leaves a lot to be desired. In fact, the chances that these stocks will ever recover are very slim, and even if they do, it won’t be for long.

The financial institutions are being slowly overwhelmed by their debts, despite all the bailouts thrown at them, both in the past 3 years and going forward.

Today may be a crucial day in the markets, though chances are that you’ll have a hard time noticing as much when all’s said and done. The language of politics and diplomacy will take care of that. Still, no matter how carefully it’ll all be put into words, something’s on the verge of breaking.

There will be a meeting between German Chancellor Angela Merkel and French President Nicolas Sarkozy. The issue at hand is, as it always is these days, how to save the euro, the eurozone, and the economies of the peripheral countries, a list that keeps growing slowly but surely.

The one item that spokesmen trip over themselves to declare will not be on the agenda is the only one that counts. Therefore, it will be on the agenda. Eurobonds.

In order to save Italy and Spain from being downgraded by the ratings agencies and attacked by the bond markets, Europe needs to come up with a huge pile of money. It’s really as simple as that. But Europe either doesn’t have that kind of money or is not willing to spend it, depending on your point of view. The difference between financial capital and political capital; the chasm may not be that wide.

The "official tools" such as the European Financial Stability Facility, and the European Stability Mechanism it is set to give birth to, are woefully inadequate.

The total size of Italy and Spain’s bond markets is €2.1 trillion ($3 trillion), while PIIGS bonds due in the next 2 years add up to €795 billion ($1.145 trillion).

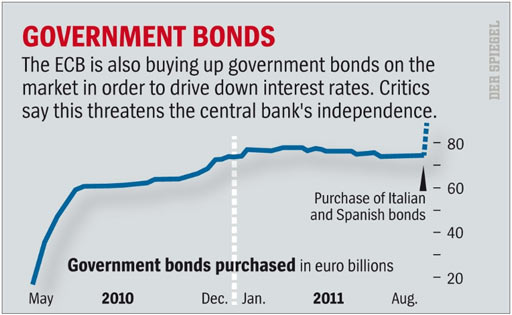

The EFSF and ESM can’t prop up all of this. Not even close. The European Central Bank has started buying some of the bonds, but long before it could swallow them in sufficient numbers, it would be in need of a bailout itself. And that’s how we inevitably get to Eurobonds.

If the Eurozone would start issuing bonds guaranteed by all its members, the hope is that they would be rated as high as German bonds (Bunds) today, AAA, and carry similar interest rates. Italy and Spain (as well as Ireland, Portugal, Greece etc.) could then borrow on international markets much cheaper than they can presently.

But this will never happen, as I’ve argued many times before, for instance in Europe throws in the towel. The premise of that article, that the ECB had irrevocably signaled its fatal lack of firing power, was doubted by many, and perhaps still is. Today’s developments will show why it is correct nevertheless. Perhaps not instantly, but since there is just one possible outcome, this is an easy call.

First, there is fast growing opposition in Germany against the Eurobonds plan, not in the least because it is widely deemed unconstitutional (in both German and EU constitutions). Opposition is equally fierce in Holland. A poll yesterday by YouGov and Bloomberg showed 75% of Germans disapprove of their government’s actions during the eurozone debt crisis, with 59% saying no further bailouts should be given, even if they were essential to keep the eurozone intact.

Second, reports came out just this morning that indicate that the German and Dutch economies have stopped growing almost entirely. Both show a Q2 2011 growth rate of 0.1% (statistical error territory). If anything, this is bound to increase opposition to the Eurobonds issue. Not that more opposition was needed or would make a difference anymore. No EU treaty ever provided for Germany saving Italy, or the other way around, for that matter. No such thing was ever a realistic option.

Merkel and Sarkozy may come out of their meeting later today with some sort of plan, veiled in carefully crafted language, that aims at raising the ceiling(s) for one or more of the financial instruments that are presently available in the Eurozone. And the ECB may keep buying PIIGS bonds for a while longer. But none of it will change the real problem in any way or shape that matters.

What I said on August 5 in Europe throws in the towel will become accepted reality in a manner of weeks. Europe will -have to- admit that it can’t save a country the size of Italy, at least not one with debts the size of Italy’s.

What happens after that is, for now, anybody’s guess. We can be sure that there are contingency plans being set up, and likely even discussed at today’s meeting, but it doesn’t look at all like Berlin and Paris have any more grip on the issues than anyone else has.

Germany and Holland may decide to leave the EU, but that would leave France in a type of isolation that Sarkozy deems unacceptable. Greece, Ireland and Portugal could be thrown out, but that wouldn’t solve the Italian and Spanish problems. They could aim for a two-tier Euro system, with "northern" euros more highly valued than "southern" ones, but that would still leave France very unhappily hanging by its fingernails.

Perhaps it’s reasonable, then, to expect the financial markets to have the final word. They can start, or rather resume, doing so today. If and when it becomes clear that Europe’s support of Italy and Spain is hollow at best and non-existent at the core, their borrowing rates can rise once again, along with those of the rest of the PIIGS and perhaps soon France. What is to save the likes of Société Générale (huge Italy exposure, world’s no. 1 equity derivatives book) when that happens is also anybody’s guess.