Thank goodness the US is closed!

Thank goodness the US is closed!

Europe is down a whopping 3.5% (so far) this morning, opening in free fall after Asia opened down about 2% on the average (but finishing at the day’s lows). Gold flew up to $1,906 before calming down but oil is down to $84.82 at 6:45 am as the Dollar tests it’s highs of 75.15 on the Euro’s fall to $1.41 and the Pound testing $1.61. Any thoughts that the BOJ was done manipulating the Yen are now officially out the window as the Dollar/Yen is STILL 76.80 (around 128.50 on FXY), the same place it’s been since August 8th!

When the World’s 3rd largest economy is manipulating it’s currency on a daily basis, of course the Global markets are going to be thrown into chaos. Every day the BOJ tries to debase their currency they must buy other currencies or foreign stocks or gold or silver or oil – ANYTHING BUT YEN to make the Yen less valuable as compared to another relative basis.

Even so, it’s not working and Japan’s new finance minister said this morning that he will try to forge a consensus among the Group of Seven leading industrialized countries that "excessive yen rises" won’t benefit the world economy when finance officials meet in France later this week. "I am hoping to see us develop a common view that excessive yen rises, as shown by facts and processes in the past, do not necessarily have a positive impact on the global economy," Mr. Azumi told reporters, referring to Friday’s planned meeting of G-7 finance ministers and central bank chiefs in Marseille, France. "At this exchange rate, it is becoming impossible for crucial parts of Japan’s export industry to make profits," he said.

Asian shares were already following US financials downhill on overblown fears of the FHFA lawsuit (see FHFA Friday). I say overblown because the first bank sued, ING, already settled for .20 on the Dollar so banks are reacting as if they already lost $30Bn when it’s much more likely this will all get washed away for $6Bn, or about 2 day’s worth of profits (4%). We’ve already seen the banking community write down over $1Tn in losses and survive to screw us over another day – do we really think this little wrist-slap will end them or is this just another example of retail suckers being stampeded out of the sector that is likely to benefit most from QE3?

Asian shares were already following US financials downhill on overblown fears of the FHFA lawsuit (see FHFA Friday). I say overblown because the first bank sued, ING, already settled for .20 on the Dollar so banks are reacting as if they already lost $30Bn when it’s much more likely this will all get washed away for $6Bn, or about 2 day’s worth of profits (4%). We’ve already seen the banking community write down over $1Tn in losses and survive to screw us over another day – do we really think this little wrist-slap will end them or is this just another example of retail suckers being stampeded out of the sector that is likely to benefit most from QE3?

Let’s take BCS, for example (see David Fry’s chart): With a market cap of $34Bn, Barclays is one of the World’s largest and best-known banks, employing 146,00 workers around the World. Their diversified portfolio prevented them from losing money in 2008 – in fact they made 7.6Bn that year but they recovered nicely in 2009 and made $16.6Bn – which is 25% of their currrent market cap – in profits – in one year. Last year was rough and they only DECLARED $7Bn in profits (1/9th of market cap) but they still dropped $26.7Bn to the bottom line in cash flow (56% of the market cap in 12 months).

BCS INCREASED their Tier 1 Capital Ratio to 11% in the first half of the year and set aside $1.6Bn for Payment Protection Insurance. Their return on equity INCREASED from 6.9% in 2010 back to 9.1% in the first half of 2011 with UK Retail banking returning15% and Barclaycard (European Visa) turning in 15% – THESE ARE FANTASTIC NUMBERS! Profits in the first half were $6Bn. This was reported on August 2nd along with the $1.6Bn that was set aside and other adjustments that took Q2 down from $4Bn to $2.4Bn, which was 40% lower than last year’s $4Bn so the stock plunged from $14.50 all the way down to $10 over the next few weeks. This is ridiculous!

To some extent, this is the problem with modern market investing. Barclays was founded in 1896 and survived 2 depressions (there was one in 1906 as well), 2 World Wars and multiple recessions yet, after one bad quarter which wasn’t actually bad anyway – investors flee out of the stock as if it were radioactive (in fact, TEPCO’s stock actually IS radioactive and has held up better). This is going on throughout the banking sector, of course, as it is in the insurance sector and that is knocking XLF all the way down to $12.50 despite the trailing .184 dividend (1.5%) and despite the fact that the Financial Sector (which we are long on through FAS) made 1/3 of all corporate profits in 2010 (close to $2Tn).

On top of making all the money, the Financial sector (thanks mainly to the Fed’s massive cash giveaway program) is sitting on over $1Tn of excess reserves yet they are being priced as if they were $1Tn short! There was a great study by the IILS titled "Did the Financial Sector Profit at the Expense of the Rest of the Economy" (short answer – yes!), which makes my point, saying:

On top of making all the money, the Financial sector (thanks mainly to the Fed’s massive cash giveaway program) is sitting on over $1Tn of excess reserves yet they are being priced as if they were $1Tn short! There was a great study by the IILS titled "Did the Financial Sector Profit at the Expense of the Rest of the Economy" (short answer – yes!), which makes my point, saying:

As profits accruing to the financial sector grew, the wage gap between financial and non-financial firms widened. And not only has the financial sector absorbed a disproportionate and growing share of valuable resources, but its practices and values have penetrated the non-financial economy. It seems that firms have increasingly been managed according to the reporting rules and short-term goals of capital markets. All this has had a negative impact on the real economy, namely business investment: real private business investment as a percent of its value added declined by roughly 2 percentage points in the last 30 years.

So the Financial Sector makes investing in anything else a bad idea yet investing in the Financial Sector is treated like it’s a bad idea too! A logical person might conclude that the Financial Sector, on the whole, does MUCH more harm than good to our economy and must be taken down – obviously it just doesn’t work on any level.

A less logical person (like us) might conclude that investors are idiots and that BCS or XLF are fantastic buys at this price for the PATIENT investor, who is willing to scale into a position over time and would be happy to double down should the Financials fall another 50%, rather than bail out with a 50% loss. On that basis – I like the following trade ideas (note this is pre- market and we may be able to do better once trading begins):

- XLF at $12.50, selling the 2013 $9 calls for $4.10 for net $8.40. This is a good play for those who can’t sell naked puts as it knocks the basis down to $8.40 with a boring .60 profit if called away at $9 but that’s still 7%, which beats T-Bills and, of course, it makes the .184 dividend a whopping 2.2% for a total return of around 9% annualized.

- Adding the short 2013 $11 puts at $1.45 to the above trade drops your basis to $6.95 but, if assigned to you at $11 (if XLF is below $11), you end up with 2x at an average of $8.97, which is not much more than if you just do a call cover, really. The nice thing here, aside from increasing your dividend return to net 11%, even if you are called away at $9, you still make $2.05 or 29% (assuming it’s over $11, of course).

Think or Swim tells me that the margin on the short puts is just $1 so JUST selling the $11 puts for $1.45 gives you a net $9.55 entry on 1x and, if the short puts expire worthless, that’s a 145% return on margin in 15 months so a nice stand-alone play as well! Keep in mind, XLF fell all the way to $5.66 in March of 2009 so you need to plan on not just buying in at net $9.55 but on doubling down at $6 for an average entry of $7.75ish. So if you don’t REALLY want to own 2x XLF at an average of $7.75 and ride that out for however many years the Depression lasts – DON’T risk getting assigned 1x at $9.55!

Think or Swim tells me that the margin on the short puts is just $1 so JUST selling the $11 puts for $1.45 gives you a net $9.55 entry on 1x and, if the short puts expire worthless, that’s a 145% return on margin in 15 months so a nice stand-alone play as well! Keep in mind, XLF fell all the way to $5.66 in March of 2009 so you need to plan on not just buying in at net $9.55 but on doubling down at $6 for an average entry of $7.75ish. So if you don’t REALLY want to own 2x XLF at an average of $7.75 and ride that out for however many years the Depression lasts – DON’T risk getting assigned 1x at $9.55!

BUT, if you think committing, for example, $15,500 to 2,000 shares of XLF ($7.75) would be a good long-term investment, then collecting $1,450 for selling 10 2013 $11 puts at $1.45 makes a lot of sense because, either you are making progress towards your goal of owning 2,000 shares of XLF very cheaply or, as a consolation prize, you will get paid $1,450 to compensate you for NOT being able to own 1,000 shares at net $9.55. $1,450 is 9.4% of your potential allocation and is 15.2% of your cash outlay and, as I mentioned, 145% of your margin outlay – Do you see why this is our favorite way to enter a long-term position?

- BCS is priced like they won’t exist in 2013! The $10 puts can be sold for $2.75, which is a net $7.25 entry (32% off the current $10.60 price). TOS says that would set us back net $1.50 in margin for a return on margin of 183% if BCS hits Jan 2013 expiration above $10.

- Much as I like BCS, they are just one bank and you never know what can go wrong – especially in Europe! So, I prefer not to over-allocate on a solo bank vs. the ETF, which I feel more confident will ultimately bounce back – even if some individual components fail. To be more aggressive and augment the short puts, I would add the 2013 $10/15 bull call spread at $1.50 so the overall trade is a net $1.25 credit with the worst case being you own 1x of BCS at net $8.75 (still 17% off the current price) and you make $1.25 + every penny up to $6.25 for any close over $10 on Jan 18th, 2013. It’s the same $1.50 in net margin plus the $1.50 in cash so return on cash and margin maxes out at 208% – that’s not bad for 15 months!

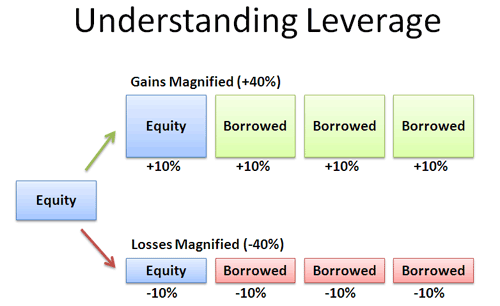

Again, looking at a practical example – we don’t use leverage to INCREASE our risks, we use it to DECREASE them. If you were considering allocating $7,250 for 1,000 shares of BCS, which is, judging from market action, a dangerous proposition. then how LITTLE can we risk to make a nice return? Obviously, selling 10 2013 $10 puts for $2.75 puts $2,750 in our pocket and risks having 1,000 shares assigned to us at $10 ($10,000) for net $7,250 but, realistically, did we expect to earn $2,750 (37%) in 15 months? If we bought $7,250 worth of the stock at $10.60, we would own 685 shares and BCS would have to climb to $13.35 for us to make $2,750.

Again, looking at a practical example – we don’t use leverage to INCREASE our risks, we use it to DECREASE them. If you were considering allocating $7,250 for 1,000 shares of BCS, which is, judging from market action, a dangerous proposition. then how LITTLE can we risk to make a nice return? Obviously, selling 10 2013 $10 puts for $2.75 puts $2,750 in our pocket and risks having 1,000 shares assigned to us at $10 ($10,000) for net $7,250 but, realistically, did we expect to earn $2,750 (37%) in 15 months? If we bought $7,250 worth of the stock at $10.60, we would own 685 shares and BCS would have to climb to $13.35 for us to make $2,750.

- If we REALLY believe BCS will get to $13.35, then how about buying 20 2013 $10/12.50 bull call spreads at .80 ($1,600). If BCS finishes at $13.35, we end up with $5,000, up $3,400! In fact, if BCS finishes at $12.50, we make $3,400 and we don’t lose money unless they can’t stay over $10.80. Getting back to our hoped-for gains of $2,750, we can work that backwards to see we only need to buy 16 bull call spreads for $1,280 to get our $2,750 return on a move over $12.50. Doesn’t tying up $1,280 on a speculative bank play make a lot more sense than tying up (and risking) $7,250 to make the same money? You are risking, on the whole, less than a 20% loss on the total commitment to make a possible 37% return on the whole INTENDED (but not necessary) commitment.

THAT is how you use leverage! You use it do DE-RISK, not to lever your risk… When you see a play that can make you 10 times your money – your reaction should be "Great – now I only have to risk 1/10th as much to make a nice potential return!" not "Great – I will bet it all and become fabulously wealthy!" If we are being paid 3:1 odds betting BCS will be over $12.50 in January of 2013, then the odds are certainly around 3:1 against us. While I am pointing our my logic for betting on this particular underdog – millions of other people – many of them certainly smarter than I am – obviously disagree!

THAT is how you use leverage! You use it do DE-RISK, not to lever your risk… When you see a play that can make you 10 times your money – your reaction should be "Great – now I only have to risk 1/10th as much to make a nice potential return!" not "Great – I will bet it all and become fabulously wealthy!" If we are being paid 3:1 odds betting BCS will be over $12.50 in January of 2013, then the odds are certainly around 3:1 against us. While I am pointing our my logic for betting on this particular underdog – millions of other people – many of them certainly smarter than I am – obviously disagree!

Using our combination play, you can sell 3 2013 BCS $10 puts for $2.75 ($825) and buy 12 of the 2013 $10/12.50 bull call spreads for .80 ($960) and you have spent net $145 cash and committed yourself to owning 300 shares of BCS at net $10.48 (about the current price – $3,144). At $12.50 or higher on Jan 18th, 2013, the short puts expire worthless and the 12 bull call spreads return $2.50 each for a total of $3,000, a $2,855 profit on your $145 cash (1,968%).

Even in an IRA account where you have to allocate 100% margin on a short put, it’s $3,000 in margin plus $960 in cash to make up to $2,855, which is 72% against cash and margin in 15 months and the worst thing that can happen on this trade is you end up owning 300 shares of BCS for net $3,145). Instead of thinking about HOW MUCH you can risk on a trade – try thinking about HOW LITTLE you can risk instead!

That’s where scaling into a position comes in. If our allocation on BCS was to be $7,250, then we’ve committed just $3,145 of it to the first 15 months. During that time, if BCS falls back to its 2009 lows of $2.66 (it was back to $20 in less than 6 months) we can buy 1,543 more shares and end up owning 1,843 shares for $7,250 or net $3.93 a share. Would that make you happy or sad? Obviously, the likely outcome isn’t that extreme but that’s what happened in the last panic and I’ll bet those investors were quite pleased with themselves when BCS went back to $20. Meanwhile, if you DON’T get the opportunity to buy BCS cheaper and they head back to $20, then you collect $2,855 in profits against the $3,960 you did commit – certainly not terrible.

If you are using leverage properly to scale into positions, then you will usually be "disappointed" with 72% returns like this as you would much rather have had the opportunity to double down at a lower price first. Since you are able to use your smaller entries to diversify your portfolio, stick much more in cash and ride out market fluctuations more easily – you will be MUCH more flexible and have a MUCH better time managing your investments over the long haul and the long haul is where we need to make our money!

If you are using leverage properly to scale into positions, then you will usually be "disappointed" with 72% returns like this as you would much rather have had the opportunity to double down at a lower price first. Since you are able to use your smaller entries to diversify your portfolio, stick much more in cash and ride out market fluctuations more easily – you will be MUCH more flexible and have a MUCH better time managing your investments over the long haul and the long haul is where we need to make our money!

Last weekend I published my September’s Dozen list of trade ideas and, when the market took off on Monday, I told Members to be patient as we were likely to get another chance to make cheap entries. Well, it looks like we’ll get it this week! This weekend, I began a review of how we traded off the August 19th lows in "Range Trading 101 – The Balancing Act (Part 1)" and I hope to finish part two today. As I said – the idea is to review what worked and what didn’t so that this time (if we hold the bottom of our range again) we can better allocate our capital on the way back up.

As we head past the usual US open at 9:30, the EU is heading into their close with the DAX down 4.6%, the CAC down 4.6% and the FTSE down 3.4% – all around their lows of the day. Italian bond yields are surging as the ECB may be backing off purchases while Berlusconi’s government backpeddles away from promised austerity measures. The Italian 10 year +20 bps to 5.48% and the 2 year +38 bps to 3.9% – not so terrible – yet.

Angela Merkel’s CDU party got its worst result ever in an election in her home state of Mecklenburg-Western Pomerania. Merkel’s handling of the EU debt crisis was a major issue, but her spiral downward doesn’t mean an end to the bailout mentality. The emergent SPD and Green parties take a softer line towards their EU brethren than does the CDU and this misreading of Germany’s troubles by Conservative investors, who are being brainwashed by Murdoch/Fox and the US MSM to believe this is some sort of referendum on Government spending are foolishly bailing out of their investments and piling into gold on the very eve of the next round of bailouts.

Angela Merkel’s CDU party got its worst result ever in an election in her home state of Mecklenburg-Western Pomerania. Merkel’s handling of the EU debt crisis was a major issue, but her spiral downward doesn’t mean an end to the bailout mentality. The emergent SPD and Green parties take a softer line towards their EU brethren than does the CDU and this misreading of Germany’s troubles by Conservative investors, who are being brainwashed by Murdoch/Fox and the US MSM to believe this is some sort of referendum on Government spending are foolishly bailing out of their investments and piling into gold on the very eve of the next round of bailouts.

Eurozone PMI fell to 50.7 in August (from 51.1) while the Service PMI held fairly steady at 51.5. UK PMI was 51.1 and all of this indicates a slowing but not yet a contraction. The UK’s Serious Fraud Office is examining several asset-backed securities for potential fraud, including deals put together by Deutsche Bank (DB) and Goldman Sachs (GS), according to the Financial Times and Banks are leading stocks lower in Europe, with RBS (RBS) -8%after being named in the FHFA’s lawsuit, along with Barclays (BCS -7.3%), Deutsche Bank (DB -5.5%), Societe Generale (SCGLY.PK -4.85%), and HSBC (HBC -1.2%).

See – I told you we could get an even better entry after the open!

US futures are right back to testing their August lows, which came just as the EU was returning from a holiday weekend at the beginning of the month. Today the US is on holiday and, once again, the global indexes are plunging with the Dollar back up at 75.38, a level we haven’t hit since August 5th. TLT (20 year notes) are even higher than they were in early August ($109.37) and are, in fact, now higher than they were in the panic of 2009 but not as high as the record 122.28 we hit in December of 2008 – now THAT’S panic!

Are things now as bad or worse than they were in 2008 or is this just market idiocy? While I lean towards idiocy – we will all do well to keep in mind the words of the great John Maynard Keynes who warned us:

Markets can remain irrational a lot longer than you or I can remain solvent.

More importantly, it was Keynes who also warned us:

Too large a proportion of recent "mathematical" economics are mere concoctions, as imprecise as the initial assumptions they rest on, which allow the author to lose sight of the complexities and interdependencies of the real world in a maze of pretentious and unhelpful symbols.

That’s what we have now, a lot of people who believe they are very clever but have lost sight of reality and God help us all because they are running the show!

Be careful out there….

Top charts by Dave Fry of ETF Digest.