{kind=link}

Rejected!

Rejected!

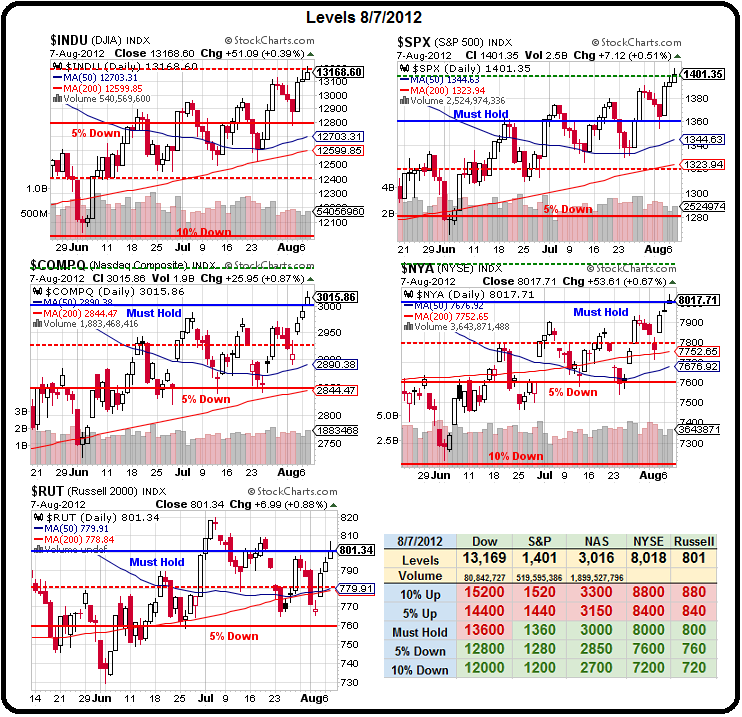

After hitting our lines ON THE BUTTON across the board (see yesterday's perfect predictions), we're taking a little pre-market tumble this morning led lower by our favorite short – PCLN, which has negotiated their way to a 15% drop on an earnings miss that didn't surprise any of our Members as it's been a focus short of ours for ages and is in both of our $25,000 Portfolios as well as our Long Put List with the Oct $540 puts, which we rolled into from the $510 puts for a net of $7.

With PCLN dropping to $575 pre-market, we won't do as well as we did on CMG last month (another focus put of ours) but we should get about $25, which will add, at 5 contracts, $9,000 to our $25KPs! When asked why we were shorting PCLN in yesterday's Member Chat, my response was:

Because the exchange rate sucks for one thing (PCLN is very big in Europe), because a great Q is priced in as PCLN has zoomed up with EXPE from last Q but are now outpacing EXPE (who are a much better company) by 20% over the past year. Also, PCLN has been diversifying into regular travel and cannibalizing their own business and, of course, because PCLN has a p/e of 30, which is a good 50% above the rest of the sector.

That pretty much sums up PCLN's earnings report. They are not a terrible company, they were simply over-priced into earnings and we took advantage of it. Now that we've had our little correction, we're moving on. We pressed our bearish bets yesterday as we expected a rejection at our Must Hold levels and my comment to Members on the way up was: "If you are going to be bearish – days like this are when you dig in your heels and shore up your positions – not the day you capitulate!"

That pretty much sums up PCLN's earnings report. They are not a terrible company, they were simply over-priced into earnings and we took advantage of it. Now that we've had our little correction, we're moving on. We pressed our bearish bets yesterday as we expected a rejection at our Must Hold levels and my comment to Members on the way up was: "If you are going to be bearish – days like this are when you dig in your heels and shore up your positions – not the day you capitulate!"

As you can see from Dave Fry's SPY chart, the "rally" looks a lit less impressive if you notice the volume, which is lower now than it was before we went off the cliff in May or August or July of last year. Traders never seem to learn that these resistance lines are very hard to cross when there is a lack of participation but it's not because of any TA mumbo-jumbo – it's just math.

The S&P represents about 1/3 of the $60Tn Global Market Cap (AAPL and XOM alone are over $1Tn) and, when Global Markets move up in synch, a 7.5% move in the S&P is a pretty good indicator that the Global Market popped $4.5Tn since early June. Now, I know I didn't take $4.5Tn off the sidelines and I'm pretty sure you didn't either so what's going to sustain the markets trading at a $4.5Tn higher level over time?

The Global Economy (also $60Tn) didn't grow 7.5% since June either and, even if you want to argue that perhaps the market was under-valued at the time – over the longer haul you can see that 1,300 on the S&P is probably a more realistic indicator of our "recovery" than 1,400 is. That's why we have our little formula that tells us that we need $10Bn in G20 stimulus/QE to get 1 S&P point (at roughly $42Bn per point) with an effect that lasts about 6 months. $10Bn is 1/4 of what an S&P point represents so, of course we get a reasonable pop – but it still isn't sustainable – even if the money went directly into stocks – which it doesn't.

You can't reprice a $60Tn market based on the excitement of a day or a week. As I often explain to Members, if I had 100 identical VW Beatles to sell and I sell one at $25,000 but then I have my mom buy one for $26,000 and make a big deal of it in the papers and then my brother buys one for $27,000 and then some guy off the street rushes in to buy one for $28,000 before the price goes up and then I sell 3 to my cousins for $29,000, $30,000 and $31,000 and that causes a frenzy that drives the next 4 sales to $35,000 from regular suckers off the street – how much are my other 90 cars worth?

You can't reprice a $60Tn market based on the excitement of a day or a week. As I often explain to Members, if I had 100 identical VW Beatles to sell and I sell one at $25,000 but then I have my mom buy one for $26,000 and make a big deal of it in the papers and then my brother buys one for $27,000 and then some guy off the street rushes in to buy one for $28,000 before the price goes up and then I sell 3 to my cousins for $29,000, $30,000 and $31,000 and that causes a frenzy that drives the next 4 sales to $35,000 from regular suckers off the street – how much are my other 90 cars worth?

On the chart – they'd look just like the S&P, wouldn't they? But I still have 90 unsold cars on my lot and, if we've finally run out of idiots and someone in town realizes that a VW Beatle is only worth $25,000 – do I still get to book a $900,000 profit on my 90 remaining cars just because the last idiot paid $35,000 or will that chart turn very ugly very fast?

Stocks like PCLN and CMG are very much like the Emperor parading around naked in their "invisible suit" – no one wants to say anything because everyone else seems to be admiring the threads and you've been told by Cramer that only an idiot can't see the value on display. That all works fine as long as everyone buys the MSM BS but then, all it takes is one little boy (or an earnings report) to shout out "but he's just naked" and suddenly it is obvious to everyone what that suit is actually worth.

Value investing isn't dead – no matter how many times Cramer et al try to bury it.