{kind=link}

Good golly what a mess!

Good golly what a mess!

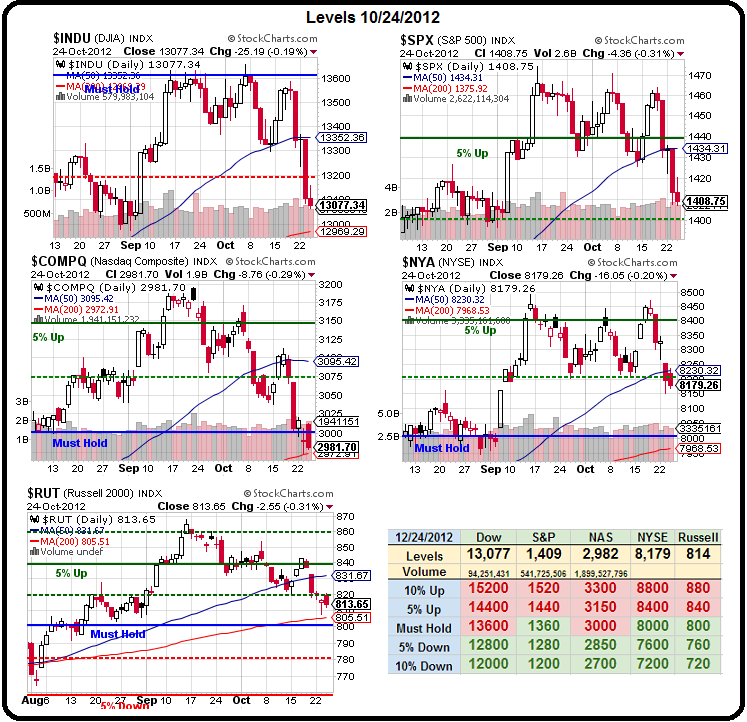

As you can see from the big chart, it's been 4 days of Hell for the markets, which is why, this weekend we had our "5 Plays that Make 500% if the Market Falls", which followed Friday and Wednesday's TZA hedge (now 100% in the money) and followed-up with Monday's DIA $135-131 bear put spread which is also 100% in the money and up 47% in 3 days already.

If you want to get fancy, the DIA $135 puts are $5.20, which is more than their max pay-off so it can be turned bullish on a bounce by pulling some or all of the long puts and leaving some of the short puts naked (tight stops, of course). The same goes for the TZA Jan $12 calls, which are $4.10 and the spread was only $3 max at close and we paid $1.90 so up over 100% if the short puts expire worthless.

Again, don't think of these as all or nothing moves, you can exercise a lot of control by buying back a few and selling a few more as the market gyrates – just as we work our AAPL position in the $25KPs. We gave up on AAPL short-term (too risky with earnings) but remain long-term bullish and will buy more if they fall this evening (and BBY and CROX should be good entries as well when they're done falling from poor reports today). I mentioned our bottom fishing expeditions in yesterday's post and, in yesterday's Member Chat – we drew a bit of a line in the sand as the Transports tested 5,000, which is nicely coinciding with the 200 dmas on the Nasdaq (2,972) and the Russell (805) although we might see Dow 13,000 before we're done – we would hate to see S&P 1,375 and NYSE 7,968, which is still far away.

As you can see from Dave Fry's SPY Chart, The S&P had a rotten day yesterday as it plowed towards our 2.5% line at 1,400 but look at that MACD line at the bottom – if that's not oversold, I don't know what is. While we've had some very poor earnings reports this week and we continue to get a lot of negative guidance, the fact is that 69% of the S&P companies that have reported so far have BEATEN earnings estimates (albeit low-bars).

As you can see from Dave Fry's SPY Chart, The S&P had a rotten day yesterday as it plowed towards our 2.5% line at 1,400 but look at that MACD line at the bottom – if that's not oversold, I don't know what is. While we've had some very poor earnings reports this week and we continue to get a lot of negative guidance, the fact is that 69% of the S&P companies that have reported so far have BEATEN earnings estimates (albeit low-bars).

What's been TERRIBLE is the revenues – 59% of the S&P companies that have reported so far (about 300/500) have missed revenue expectations. That's why AAPL's number tonight is critical, AAPL is now about 5% of the S&P by size but their earnings are more like 10% of the total so tonight's report by AAPL can make or break the quarter for the group.

In Q4 last year, for example, the S&P showed 0.5% growth in profit margins but, without AAPL's very impressive 30%, overall margins were down 0.22%. AAPL is, of course 20% of the Nasdaq, which is ridiculous and why we call it the AAPLdaq – and tonight, they will make or break the index at that 200 dma.

We had a nice little rally going this morning but, as usual, the Euro began falling again and fell right through the $1.30 line as the BOJ pushed the Yen back over 80 (now 80.2) buy buying Dollars and that Yentervention is sending the Dollar back over 80 (up 0.3%), which is putting a damper on the indexes despite a pretty good Durable Goods Report (up 9.9% headline, up 2% ex-transports).

As you can see from the chart – this is a very strong reversal and may indicate that it was last month's 13.2% drop that was the anomaly and we are, in fact, bottoming out in manufacturing.

This flies in the face of the MSM Doom Squad, who have been saying that fears of the Fiscal Cliff have frozen businesses and consumers in their place. It's a nice story, but where's the evidence. All it really is is a bunch of Conservatives with microphones, who are essentially saying "Vote for Romney or we'll shoot this economy."

Speaking of Conservative idiocy – the US is now producing 10.9Mb of oil per day – that's 28.5% more than was produced under GWB just 4 years ago (8.5Mbd) and, even more significant, just 700,000 barrels a day less than Saudi Arabia. Gosh, that's not what they tell us on Fox, is it? In fact, one of the reasons record amounts of oil money are pouring into the Romney campaign – as well as GOP candidates around the country ($200M for Romney alone!), aside from the Republican war against renewable energy, is Obama's 5-point plan to crack down on price manipulation in the energy markets, in which he proposes to:

- Request Immediate Funding to Put More "Cops on the Beat" Overseeing Oil Markets: The President is calling on Congress to pass an immediate increase in funding to support at least a six-fold increase in the surveillance and enforcement staff for oil futures market trading at the Commodity Futures Trading Commission (CFTC).

- Fund Critical Technology Upgrades in the Oversight and Surveillance of Energy Market Activity: The President is also requesting that Congress provide the CFTC funding for critical IT upgrades to strengthen monitoring of energy market activity.

- Substantially Increase Civil and Criminal Penalties for Manipulation in Key Energy Markets: The President's proposal includes a ten-fold increase in maximum civil and criminal penalties for manipulative activity in oil futures markets. These heightened penalties will make sure that penalties reflect the seriousness of misconduct.

- Empower the CFTC to Raise Margin Requirements in Oil Futures Markets: The President is also calling on Congress to act immediately to give the CFTC authority to direct exchanges to raise margin requirements to address increased price volatility or prevent excessive speculation or manipulation. This authority will help limit disruptions and reduce volatility in oil markets.

- Take Immediate Steps to Expand Access to CFTC Data to Better Understand Trading Trends in Oil Markets: These executive actions will allow additional analysis of CFTC's data to look for patterns and better understand trading activity in energy markets.

As you can see from this Bespoke chart on oil inventories, we are continuing to build record surpluses in US petroleum inventories, with an additional 6.7Mb added in this week's Inventory Report alone. And that's WITH the US EXPORTING a record 1Mbd of petroleum products to other countries. We simply have much more oil than we need yet the US oil cartel keeps prices artificially high as they desperately try to get their guy elected before the President can take action to reign in this madness.

As you can see from this Bespoke chart on oil inventories, we are continuing to build record surpluses in US petroleum inventories, with an additional 6.7Mb added in this week's Inventory Report alone. And that's WITH the US EXPORTING a record 1Mbd of petroleum products to other countries. We simply have much more oil than we need yet the US oil cartel keeps prices artificially high as they desperately try to get their guy elected before the President can take action to reign in this madness.

The UK surprised this morning with a 1% growth in GDP, but that probably had more to do with the August Olympics than any real turn-around in the economy. Still, it's making the European indexes happy and, if we can keep the momentum going – we could be on the way to taking out those strong bounce lines (see yesterday's post) after failing at the weak ones yesterday.

After that, it's all up to AAPL to make or break this market.