Courtesy of Mish.

The HSBC Flash China Manufacturing PMI™ report shows Operating conditions continue to improve in December.

Key points

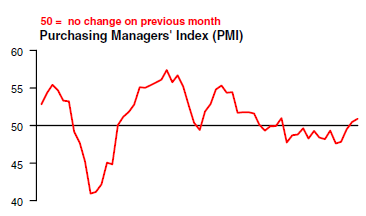

- Flash China Manufacturing PMI™ at 50.9 (50.5 in November). Fourteen-month high.

- Flash China Manufacturing Output Index at 50.5 (51.3 in November). Two-month low.

Data collected 5–12 December 2012.

Commenting on the Flash China Manufacturing PMI survey, Hongbin Qu, Chief Economist, China & Co-Head of Asian Economic Research at HSBC said:

“As December flash manufacturing PMI picked up further to a 14 month high, it confirmed that China’s ongoing growth recovery is gaining momentum mainly driven by domestic demand conditions. However, the drop of new export orders and the downside surprise of November exports growth suggest the persisting external headwinds. This calls for Beijing to keep an accommodative policy stance to counter-balance the external weakness, provided inflation stays benign.”

{kind=link}

Has China Turned the Corner?

Before anyone gets excited by this 14 month high (barely above contraction), please consider a few comments by Michael Pettis at China Financial Markets. The comments via email are from December 6, following the last full PMI report but prior to this flash report.

Following many months of gloom – and seven consecutive quarters of declining growth – the Chinese stock markets are permitting themselves a frisson of excitement after China’s official manufacturing PMI rose to a seven-month high of 50.6 in November, from 50.2 in October. The higher PMI was propelled (unfortunately, I think) by a surge in construction activities. Infrastructure investment was also strong.

The HSBC China manufacturing PMI, which is more heavily weighted towards smaller companies, also rose, to 50.5 up from 49.5 in October, but not without dire warnings from smaller companies that the outlook continues to be, for them, very poor. Orders are generally up, but not enough to reduce inventory, and it is the big companies, not the small ones, who seem to account for all the improvement in the two PMIs.

Still, the overall numbers were stronger than they have been for most of this year. “We believe that China’s near-term outlook remains positive as the political uncertainties have dissipated after a smooth leadership transition,” ANZ said in their subsequent research piece. “The much-feared ‘hard landing’ has been averted,” IHS wrote in their own research piece. “Economic activity is back, and growth has bottomed out.”

I don’t think, however, that we should get overly excited. The economic slowdown in China has not bottomed out except in the very short term, and pretty much as I (and many of my fellow skeptics) had expected. It was obvious all year that the political transition was going to be tough and that there would be strong opposition to reforms that the leadership is pretty serious about wanting to implement (about which more later). In that case, and as I have been writing since early this year, I expected that Beijing would once again step on the investment accelerator to create some good feeling within which the new leaders can more easily manage the process of consolidating power.

As I see it, the length of the upturn will give us a sense of how difficult the process of consolidation will have been. If we see investment start to flag in the late first quarter or early second quarter of 2013, and with it growth drop sharply, this would suggest to me that the leadership is in firm control and determined to begin the adjustment process as quickly and forcefully as possible. If investment and economic growth continue strong through the end of 2013, I would be a lot more pessimistic about the pace of the adjustment and more worried about the possibility of a debt problem). The better the numbers over the next year, in a sense, the worse the medium term outlook.

No one should doubt, in other words, that this “bottoming out” is very temporary and most certainly not a bottoming out in any meaningful sense (and in fairness both IHS and ANZ, who are quoted above on the subject of “bottoming out”, warn that this may be temporary). Growth in China in the short term can only occur with a surge in investment, and by now we should all be worrying about the longer-term consequences of more investment.

…