{kind=link}

Up 19.7% in 7 months.

Up 19.7% in 7 months.

That's not bad. Our goal in our most Conservative virtual portfolio was to make $4,000 a month so a person with $500,000 in a retirement account can generate $48,000 a year to live on without touching (and, hopefully, growing) the principal. As we're now up $95,175 on $500,000 in our 7th month (and only about 50% invested), we are comfortably on track as all those little trees we planted begin to take root.

The current positions are actually up $130,845 but we pulled some bad positions that lost us $35,670, which is normal as we begin this process - you can't pick all winners - the key is to have the discipline to cut your losses and nurture those winners because, hopefully, those are the ones that will be with you a long, long time and keep producing that income. So, in theory, this type of portfolio gets stronger and stronger each year and it's amazing how fast it can grow - especially when we're at a 35% annual pace.

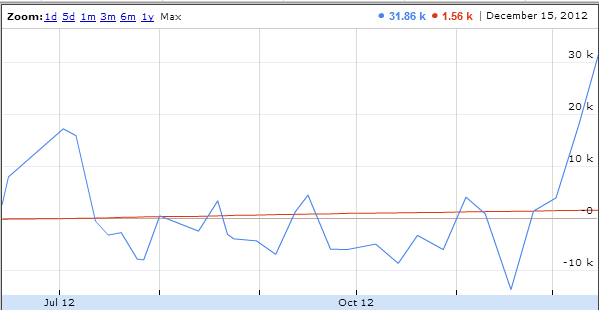

We might have done even better but we picked a terrible time to start this one, initiating a lot of initial positions in August and September, as the S&P topped out at 1,474. The markets began a relentless downturn all the way into QInfinity in November and bottomed out at 1,343 (down 9.5%) around the election and only last week made it back to where we were. Fortunately, our investing plan includes scaling into positions so we were able to adjust and add along the way - taking advantage of the dip and giving us a great return - even though the market is essentially flat to where we entered.

We might have done even better but we picked a terrible time to start this one, initiating a lot of initial positions in August and September, as the S&P topped out at 1,474. The markets began a relentless downturn all the way into QInfinity in November and bottomed out at 1,343 (down 9.5%) around the election and only last week made it back to where we were. Fortunately, our investing plan includes scaling into positions so we were able to adjust and add along the way - taking advantage of the dip and giving us a great return - even though the market is essentially flat to where we entered.

The chart on the right shows the portfolio's performance over time - down over $13,000 in November before turning around with the markets.