{kind=link}

Courtesy of The Automatic Earth.

Acme News Photo Moon River 1935

Last week we saw that China exports were down 18% in February and 6.6% in March, and that US mortgage originations are at their lowest level in 14 years. This week, the scary numbers just keep rolling in. Still, markets are up because Beijing has claimed a 7.4% GDP growth rate for 2014, and initial jobless claims in the US are falling somewhat, and most of all because everyone wants to believe in the recovery because they’re to scared of the alternative. If and when countries like Greece and Italy still have sky-high unemployment numbers and can nevertheless sell sovereign debt at puny yields, something’s definitely out of balance.

There’s a giant casino out there that poses as a solid investment vehicle that allows you to put your money in well-run and well-running enterprises that are working hard to produce what the public wants and needs, but in reality stock prices no longer reflect what companies do, but what their stocks do. It’s a hot air snake oil gold rush pyramid , and as long as the music plays you got to keep on dancing. There was a time when P/E ratios mattered, but it’s so yesterday to talk about those. It only takes a rumor of a gold seam some place out west for all of them to saddle up their wagons and chase the trail. It may go too far, at this point, to kill it mass hysteria, but it’s getting there. And the scary numbers just continue to flow in.

BusinessWeek says this (I adapt headlines at times to catch relevant details):

China Home Values Drop 7.7%, New Construction Down 25.2%

Most worrisome, however, is the clear cooling of China’s property market. The value of homes sold, 1.1 trillion yuan, dropped 7.7%. Broader property sales including commercial buildings reached 1.33 trillion yuan, down 5.2%. New property construction amounted to 291 million square meters, dropping 25.2% – that’s the worst first-quarter performance since 2009 and a signal that property developers are worried about sales over the rest of the year. [..] Urban real estate investment amounts to more than 10% of China’s economy.

New property construction in China fell 25.2%! In an economy that depends on real estate investment for 1 in every 10 dollars (and for far more on exports which also plunge), What was that number again, 90,000 property developers in China but only 30,000 viable concerns? And Beijing intends to let them go in a soft landing? Obviously, most people are not selling when values of homes that change hands fall by 7.7%, but as always some will have to.

And with each domino sold, another domino tumbles. China has been overbuilding in a wild craze and it’s hard to see what it can do next to stop prices from falling further. It could intentionally halt additional building activity, and create less supply while hoping for enough demand, but that would hammer both developers and builders, and push many Chinese out of relatively well paying jobs. It will probably try and find a golden middle road, but it’s all too easy to get those wrong. And then you get more of this:

Chinese Police Confront Trust Investors Demanding Repayment

Chinese investors demanding their money back from a troubled 973 million-yuan ($156 million) high-yield product in Shanxi province were confronted by police in front of a China Construction Bank branch. People wearing white masks with the words “despicable bank” and “pay back our money” were among at least 30 investors facing special-forces officers in dark uniforms in Taiyuan city, about 521 kilometers (324 miles) southwest of Beijing.

The nation’s second-largest bank is the custodian of the Songhuajiang River No. 77 trust, which missed six payments as of last month, according to the Economic Observer. “We have been cheated by CCB,” said Wang Fengying, 60, a Shanxi resident who said her husband had invested 1 million yuan in the product. “Our parents are very old. We need the money for their medical bills and to buy a home for my child. We are so miserable and they won’t even let us demand our money back.” The unrest underscores the stress in China’s $1.75 trillion trust industry [..]

Using special forces on your own people, certainly when they have legitimate complaints, is something every government should be cautious about. But it’s clear that if it concerns your 2nd biggest state(!) bank, there’s a risk any which way you choose to go. Still, what’s going to happen when there are protesters like this in a 100 cities, and in larger numbers? Sure, these people may have sought unrealistic returns on their investment, but to what extent can you hold that against them when it concerns a bank that belongs to the state?

John Rubino reports that Japan has major troubles in selling its sovereign bonds, with trade volume down by 70%, and a day and a half of no trade at all. If only the central bank buys government bonds, other investors move away. Until they get better yields. But in the case of Japan, with its behemoth state debt, higher yields very quickly turn into behemoth problems. It’s no accident that this happens just as Abenomics runs into its very predictable roadblock, precipitated though not caused by the April 1 sales tax rise, but it may well signify the beginning of the end of Tokyo being able to run the nation bond sales alone.

Bank of Japan Only Buyer Left for 10-Year Japanese Government Bonds

Here’s something you don’t see very often: For a day and a half this week, the Japanese government’s benchmark 10-year bonds attracted not a single successful private sector bid. At today’s artificially-depressed yields, no one wants this paper — except of course the Bank of Japan, which is buying up the bonds with newly-created yen. As the Gulf Times noted:

The Bank of Japan’s massive purchases of government debt hit a milestone this week, sucking liquidity out of the market to such an extent that the benchmark 10-year bond went untraded [..] for more than a day and a half. Trade volume in the benchmark cash bonds so far this month dropped to less than one trillion yen, down about 70% from the same period last year.

These are the most important fixed income instruments of the world’s third biggest economy, and the only entity willing to own them is the government that issues them. The rest of the world now refuses to lend money for ten years at 0.6% to a government whose debt is 200% of GDP and rising, which leaves Tokyo with only two choices: monetize virtually all its future borrowing or allow interest rates to rise and pay two or three times as much in interest going forward. The latter choice would hobble, if not cripple, an economy that can only function when borrowed money is nearly free.

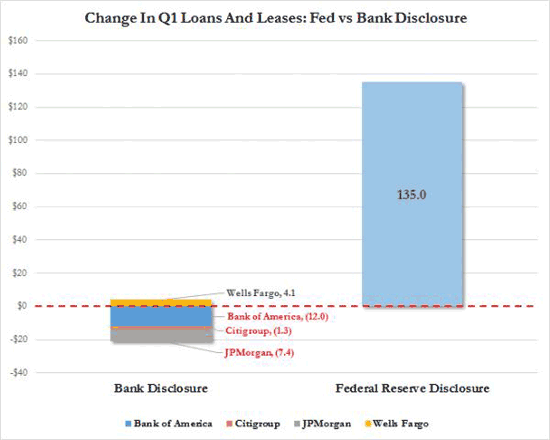

And if we turn stateside, Tyler Durden has found a “little” discrepancy that should raise a few BIG questions. The Fed has reported a hefty rise in loans and leases at US banks, but the banks’ own numbers show nothing of the kind. This is “only” the big 4 banks, which are good for 42% of all loans outstanding, so in theory the other, smaller banks, could be behind the rise the Fed talks about, but that would mean the shareholders of JPMorgan, Wells Fargo, BoA and Citi need to fire the asses of their executives for letting such a huge piece of their market slip away. It seems more likely that the Fed is not telling the truth here.

Is The Fed Fabricating Loan Creation Data? (Zero Hedge)

One of the more bullish “fundamental” theses discussed in recent weeks, perhaps as an offset to the documented record collapse in mortgage origination – because without debt creation by commercial banks one can kiss this, or any recovery, goodbye – has been the so-called surge in loans and leases as reported weekly by the Fed in its H.8 statement. This is indeed notable because as we have shown in the past, for nearly five years, total loans and leases within the US commercial system remained virtually unchanged from a level of about $7.3 trillion [..]

Of course, if the data represented by the Fed, which supposedly is a sample of call reports distributed to commercial banks, is accurate,[..] it would slowly allow the elimination of the Fed’s artificial conditions and removal of the central-planning umbrella.

And logically, since the Fed’s data is sourced by the banks themselves, what the Fed is representing and what the banks report quarterly should be in rough alignment. Unfortunately it isn’t. [..] … the Top 4 banks held some $3.14 trillion in loans and leases at March 31. So far so good. But what is not so good is that the change of this number in the first quarter is not an increase even remotely comparable to what the Fed makes those who read its H.8 statement believe it is. Quite the opposite. As the chart below shows, in the first quarter, of the Big 4 banks, only Wells Fargo reported an increase – a tiny $4 billion to be exact – in its loans and leases portfolio. All the other banks… saw a decline in their loans and leases holdings. We show this on the chart below.

We are of course bombarded on a daily basis with twisted, made up and simply untrue stories and interpretations through the media and government officials. But that will necessarily backfire, because once it’s revealed that you make it all up as you go along, at some point trust and confidence will disappear from the markets. It would be much preferable for everyone, except of course for those who profit most from the fantasy “news”, if markets returned to honesty. Thing is, how would we get there? The big media are not going to do any truthfinding, those days are long gone, their present role is much more profitable. It’s going to take either a major crash or a country saying we’ve had enough of this. Meanwhile, has there ever been a time when the entire globe refused to restructure their debts and return to a financial system people could trust?