Courtesy of Mish.

On May 13, the BCA came out with this recommendation U.S. High-Yield: Maximum Overweight.

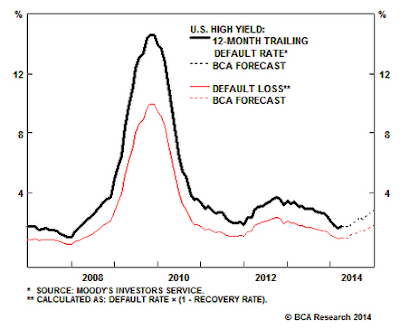

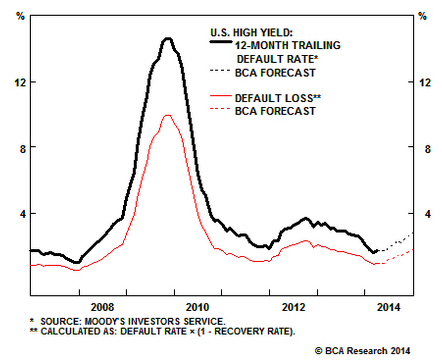

Our model predicts that the default rate for speculative grade bonds will average near 3.0% during the next year. Moody’s latest estimate for the 12-month trailing default rate is much lower at 1.7%. Our view is that the U.S. and global economies will continue to expand (and recession will be avoided) over at least a one-year investment horizon. In this case, default losses could remain less than that projected by our model which is calibrated to pre-crisis macro factors. The current cycle could see the default rate move lower still given the scope of deleveraging that followed the financial crisis and Great Recession. Corporate balance sheets are in excellent shape, and there is still an ample cash cushion available to fund operations in the event of a growth setback.

We continue to monitor three key factors for evidence of a turn in default risk: our Corporate Health monitor, bank lending standards, and Fed policy. None of these yet signal cause for concern.

{kind=link}

No Cause For Concern – Yet

I doubt we see default rates spike as high as they did in 2009, not because corporations are really flush with cash, but rather because corporations are holding cash-substitutes (backed by debt). Those cash-substitutes can be used as cash in a credit crunch emergency.

Nonetheless, there are numerous problems with the “Don’t Worry Yet” philosophy. What follows is a discussion from a risk-reward standpoint, starting with reward.

Potential Reward

Using the SPDR Barclays High Yield Bond (JNK) as a general proxy for high yield bonds, the reward prior to writeoffs is approximately 5.85%.

To calculate actual net return, start with 5.85%, subtract BCA’s expected default rate of 3.0%, then subtract another 2.0% or so for inflation. Assume a recovery rate of 40-60% on defaults and you are overweight “junk” for a final net return 2%+-.

Potential Risks

What about the risks? Could BCA’s model be wrong? Might default rates be much higher? Might the market start pricing in an expectation of higher defaults even if defaults themselves do not soar? What about rising rates? What about liquidity risks if the market turns on junk bonds?

What about the fact that complacency is at an extreme (see Big Appetite for Risk) and risky assets are typically the first to suffer in a downturn?…